Here we're discussing the Rick Ferri Core 4 Portfolio, looking at its components, historical performance, and the best ETF’s to use for it.

Interested in more Lazy Portfolios? See the full list here.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

Video

Prefer video? Watch it here:

What Is the Rick Ferri Core 4 Portfolio?

As the name suggests, the Core 4 Portfolio was created by financial adviser and author Rick Ferri in 2007. To be clear, he has created several “Core-4” portfolios. Here we're talking about the “Classic” one. Even within the “Classic” Core 4 Portfolio, Ferri proposes 4 different risk tolerances: low-risk, conservative, moderate, and aggressive, each with a different asset allocation. For the sake of simplicity in this post, I'll be using the “Moderate” risk tolerance allocation which is 60/40 stocks/bonds.

Rick Ferri is a retired US Marine Corps officer and fighter pilot and former stockbroker. He is now an investing consultant and author. Ferri believes in “decoupling” advice from portfolio management, and supports low-fee index investing. Read more about him here. You can get the second edition of his most popular book All About Asset Allocation here on Amazon.

The “Moderate” allocation of the Classic Core 4 Portfolio looks like this:

- 36% Total US Stock Market

- 6% US REITs

- 18% Total International Stock Market

- 40% Total US Bond Market

Rick Ferri Core 4 Portfolio – Performance Backtest

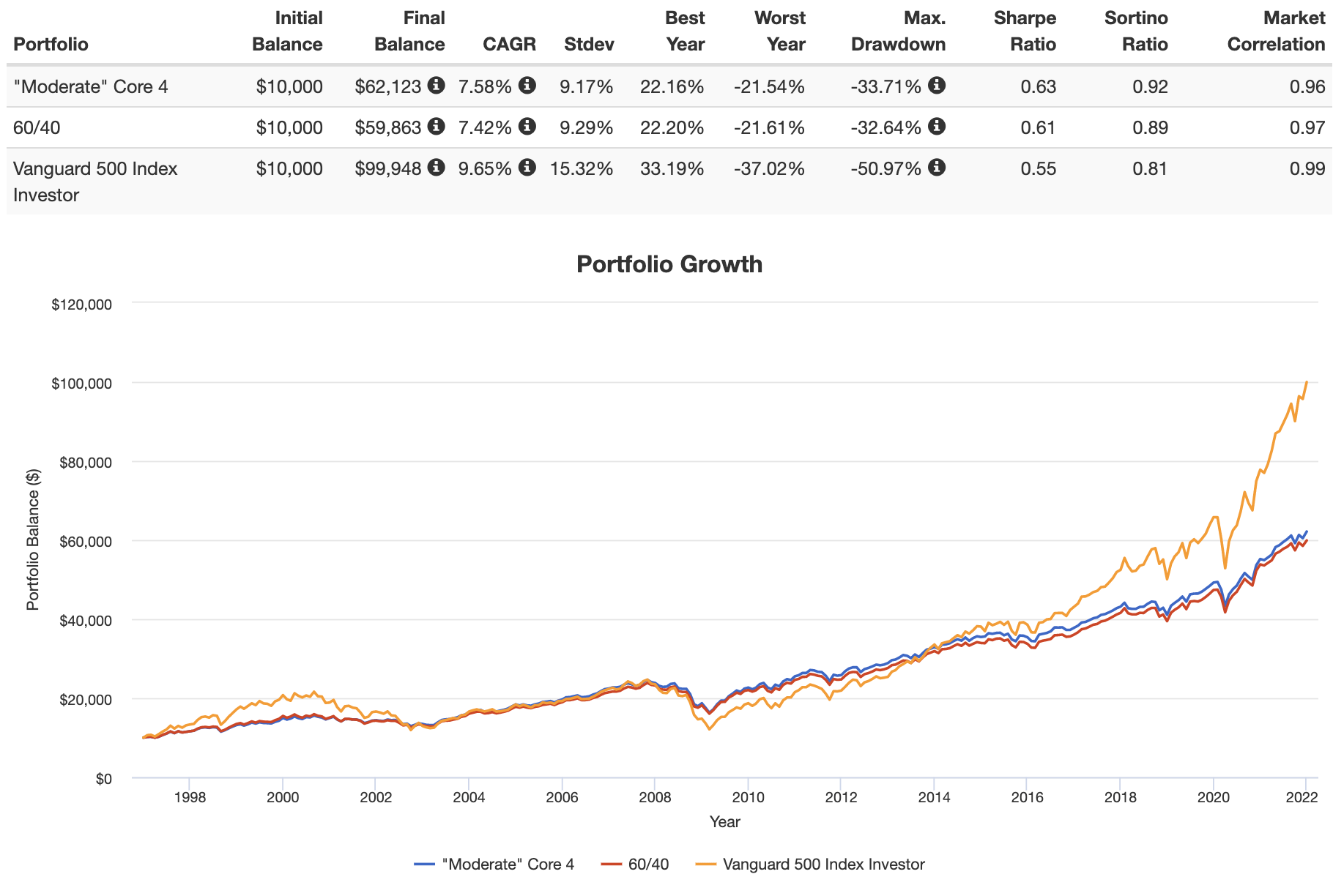

Going back to 1996, here's a comparison of the Core 4, a traditional 60/40, and the S&P 500 through 2021:

Notice how the addition of REITs increased the return of the Core 4 compared to its 60/40 benchmark, thereby allowing it to have higher general and risk-adjusted returns, with slightly lower volatility but also a slightly larger max drawdown. This drawdown was larger because it was from the 2008 Global Financial Crisis.

Also notice how the volatility and drawdowns of the Core 4 and 60/40 are lower than the S&P 500 by about 1/3.

Rick Ferri Core 4 Portfolio ETF Pie for M1 Finance

M1 Finance is a great choice of broker to implement the Rick Ferri Core 4 Portfolio because it makes regular rebalancing seamless and easy with one click, has zero transaction fees, and incorporates dynamic rebalancing for new deposits. I wrote a comprehensive review of M1 Finance here.

Using entirely low-cost Vanguard funds, we can construct the Core 4 Portfolio pie with the following ETF’s:

- VTI – 36%

- VNQ – 6%

- VXUS – 18%

- BND – 40%

You can add the Core 4 Portfolio pie to your portfolio on M1 Finance by clicking this link and then clicking “Add to Portfolio.”

Canadians can find the above ETFs on Questrade or Interactive Brokers. Investors outside North America can use Interactive Brokers.

Disclosures: I am long VTI and VXUS in my own portfolio.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

What are your thoughts about investing in the covid-19 age? I am age 76 and my wife age 66…both retired.

We were thinking of letting Vanguard manage our portfolio. Am now out of the equity market…just in bond ETF’s and some GLD.

Hey Ed,

If I were in your situation and attempting to minimize volatility and risk, I’d probably go with the All Weather Portfolio.