Here we dive into the famous “Excellent Adventure” from Hedgefundie and how to implement it.

Interested in more Lazy Portfolios? See the full list here.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality, ad-free content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I get if you decide to purchase through my links. Read more here.

In a hurry? Here are the highlights:

- Hedgefundie

iswas a member of the Bogleheads forum. - Hedgefundie created a thread in February 2019 proposing a 3x leveraged ETF investing strategy based on risk parity using the S&P 500 index (UPRO) and long-term treasury bonds (TMF) held in a 40/60 allocation. The thread later expanded into a Part 2.

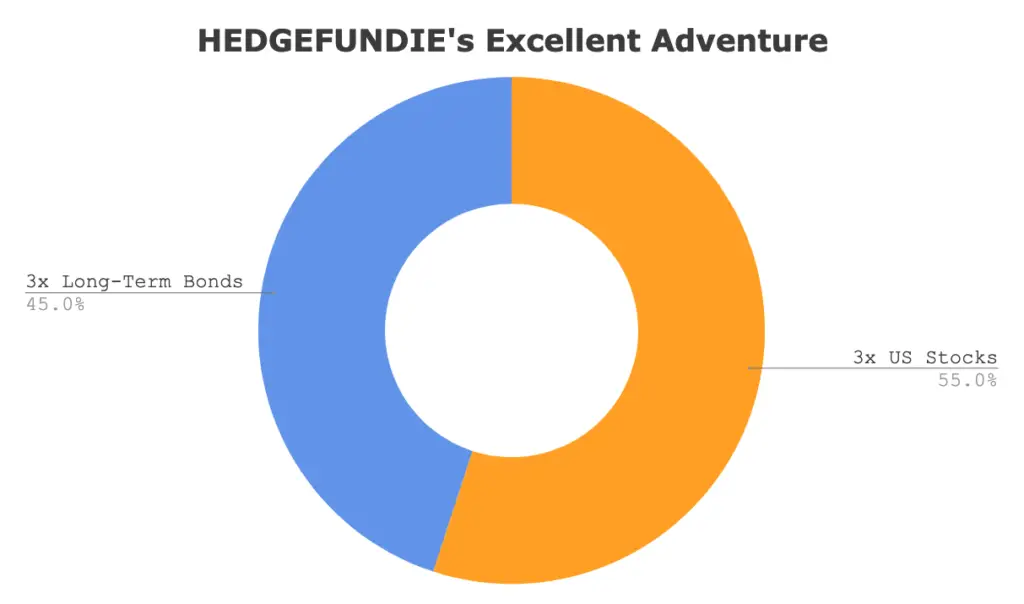

- Hedgefundie later updated the strategy's asset allocation in August 2019 to 55/45 UPRO/TMF.

- Extensive backtesting, discussion, and analysis within the thread by members of the Bogleheads forum supports the validity and potential market outperformance of the strategy.

- The proposed strategy calls for quarterly rebalancing.

- Several different protocols/variations of the strategy emerged in the Excellent Adventure thread, including monthly rebalancing, rebalancing bands, and volatility targeting with various lookback periods.

- Some users have added a dash of TQQQ (3x the NASDAQ 100 index) for a minor tech tilt, as Big Tech has had a stellar run recently.

- It is recommended to implement the strategy within a Roth IRA on M1 Finance, to avoid tax implications and to make regular rebalancing seamless and easy.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. All examples above are hypothetical, do not reflect any specific investments, are for informational purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Contents

Video

Prefer video? Watch it here:

Who Is Hedgefundie?

Hedgefundie is was a member of the Bogleheads forum who created a now-famous thread on the forum proposing a 3x leveraged ETF strategy.

What Is the Hedgefundie Strategy?

The Hedgefundie strategy – the wild ride of which is known as “Hedgefundie's Excellent Adventure” – is based on a risk parity allocation of leveraged stocks (3x the S&P 500 index via UPRO) and leveraged long-term treasury bonds (3x the ICE U.S. Treasury 20+ Year Bond Index via TMF). Note that “HFEA” is the shorthand initialism for the name of the strategy, not the ticker for a fund.

Risk parity is a portfolio allocation strategy in which, consistent with Modern Portfolio Theory (MPT), risk is spread evenly among assets within the portfolio by looking at the volatility contributed by each asset, thereby attempting to optimize returns per unit of risk (Sharpe). I explained it more here. Parity between stocks and long treasuries is roughly achieved at 40/60.

The Hedgefundie strategy relies heavily on the negative correlation (or at least, uncorrelation) between stocks and long-term treasury bonds, wherein the bonds provide a buffer during stock drawdowns. Long-term treasuries are chosen precisely because they are more volatile than shorter-duration bonds and because of their degree of negative correlation to stocks, in order to sufficiently counteract the downward movement of a 3x leveraged stocks position in a crash. I delved into these specific benefits of treasury bonds here. This concept is based on the simple historical principle of improving risk-adjusted return (Sharpe) over long periods by holding uncorrelated assets, such as a traditional 60/40 stocks/bonds portfolio, as opposed to 100% stocks. In a nutshell, this is a way to hold UPRO long term in a much more sensible way.

Consistent with the idea of Lifecycle Investing, this heavily-leveraged strategy is better suited for young investors with a long time horizon who can afford to be risky early in their investment horizon. Hedgefundie advocates for treating this strategy like a “lottery ticket” and not using it with a significant portion of your total portfolio value.

Critics and naysayers reflexively exclaim the oft-cited, overblown, platitudinous “Leveraged ETF's aren't meant to be held long-term because of volatility decay,” but, in short, that doesn't concern me. Moreover, that same volatility decay can actually help when upward movement with positive momentum is occurring. I would also argue that as long as you can stomach the volatility, a major drop should [eventually] be followed by a major rebound; 3x hurts on the way down but helps on the way up. UPRO from ProShares and TMF from Direxion were chosen due to their low tracking error and high volume; again, we're getting 300% exposure to the S&P 500 and long-term treasury bonds, respectively.

The proposed strategy calls for quarterly rebalancing. Several different protocols/variations of the strategy emerged as the Excellent Adventure thread progressed, including monthly rebalancing, rebalancing using bands, and volatility targeting with various lookback periods. I'd keep it simple and avoid checking it often; I can see it being very easy to get emotional with this strategy and abandon your plan. It is recommended to implement the strategy within a Roth IRA on M1 Finance, to avoid tax implications and to make regular rebalancing seamless and easy.

I know this sounds saIes pitchy, but if you're wanting to use this strategy in a taxable account, I would argue it makes even more sense to use M1 Finance because if you're choosing to put in new deposits, the system will automatically rebalance the portfolio for you by directing new deposits to buy the underweight asset, thereby allowing you to avoid capital gains taxes that would otherwise be incurred with a manual rebalance. This is more impactful than it might sound at first. These are 3x leveraged ETFs; they can very quickly get out of balance. For example, let's say you start out at the prescribed 55/45 and stocks take off and bonds suffer, which causes it to stray to 75/25 after only a month. Not good. At this point you'd have to incur short term capital gains taxes (ouch!) just to get things back in balance. Granted, at a certain point, your new deposits may not be sufficiently large enough to provide the full rebalancing effect on their own, but that would be a great problem to have.

Utilizing a traditional, unleveraged 40/60 stocks/bonds portfolio, compared to an all-equities portfolio, has relatively low volatility and should produce higher risk-adjusted return (Sharpe) over long time periods, but would also likely underperform an all-equities portfolio in terms of total return. The solution, Hedgefundie maintains, is applying leverage. We're attempting to accept a risk profile similar to that of the S&P 500, but with much higher expected returns.

Hedgefundie updated the approach 6 months after posting the original strategy, opting to move to a 55/45 UPRO/TMF allocation from the previous 40/60 risk parity allocation. Hedgefundie's reasons are laid out here, based primarily on the premise that the stocks portion of the strategy is the primary driver of the strategy's returns and that the main purpose of holding the treasury bonds is essentially as “insurance” in case of a stock market crash.

Intrinsically, we're relying on US stocks and long-term treasuries not crashing in tandem. At the time of writing, these assets have a seemingly reliably negative correlation close to -0.5 on average. A key fundamental assumption of this strategy that Hedgefundie proposes is that the US will not return to pre-Volcker (pre-1982) monetary policy. That is, we'll be able to significantly mitigate or altogether avoid runaway inflation periods like the late 1970's, during which time bonds suffered greatly.

Stocks and long-term treasury bonds do not have a perfect -1 correlation. Sometimes they move in the same direction. This is actually a good thing. Historically, when these assets moved in the same direction, it was usually up. On days when stocks dropped, long-term treasuries fairly reliably rose significantly to mitigate the total loss.

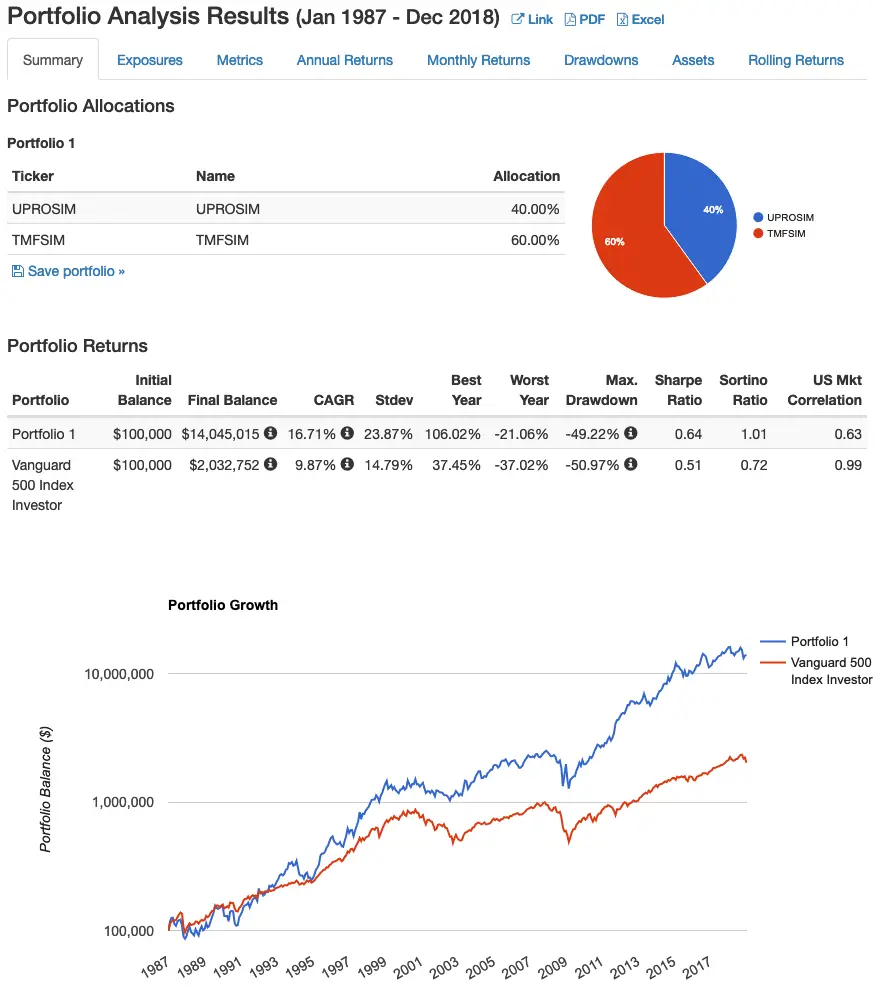

Simulated returns going back to 1987 look like this:

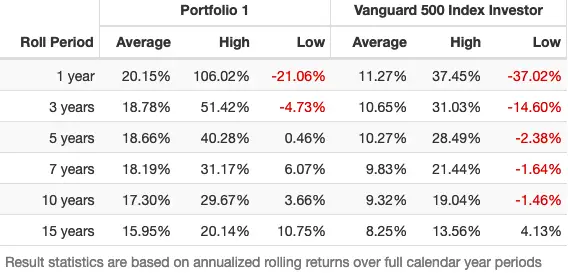

Here are the rolling returns:

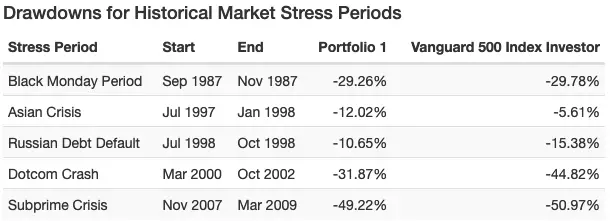

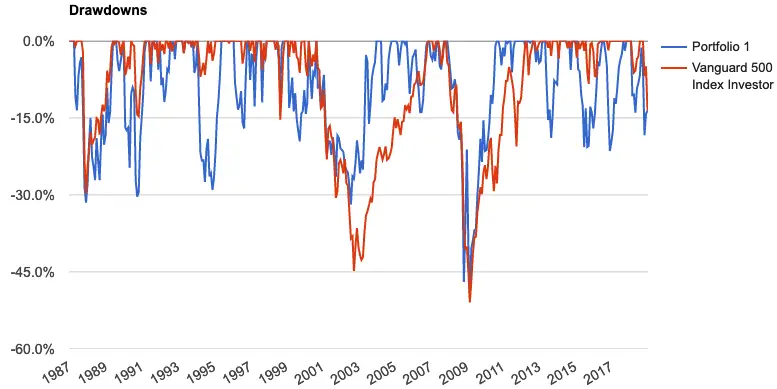

Below are the drawdowns. Notice the smaller drawdowns in most cases compared to the S&P 500:

I agree with Hedgefundie's assertion that extremely volatile assets like gold, commodities, small caps, etc. would suffer worse from volatility decay and would not improve the strategy's diversification and return. International developed markets may be a viable option to include, but Boglehead member siamond found issues with the DZK ETF, which ended up closing in October, 2020 anyway.

If you wanted to for some reason, you could also use the slightly more expensive SPXL instead of UPRO. Their liquidity and performance should be nearly identical.

Make no mistake that this is a risky strategy by its very nature. Read up on leverage and the nature of leveraged ETF's before employing this strategy. Do not put your entire portfolio in this strategy.

Read more details and nuances of the strategy on the original thread here. If you've got the time, there's a lot of learning to be had throughout the entire thread. The thread has expanded into a Part 2 here.

UPRO vs. TQQQ

Some users have added a dash of TQQQ (3x the NASDAQ 100 index) for a minor tech tilt, as Big Tech has had a stellar run recently. Others still are using TQQQ as the entire equities position for the HFEA strategy. I personally think this is unnecessary and is purely performance chasing as a product of recency bias.

Imagine for a second that this is January, 2010. After the previous decade, the S&P 500 is down by about 10% for that time period versus the Nasdaq 100 being down about 50%. Would you still be as enthused about TQQQ? Logically, we should be more willing to buy when prices are low, but I’d be willing to bet the honest answer to this question for most folks would be “no.” A rational investor should want to avoid expensive stocks and buy cheap stocks, but this unfortunately isn’t how investors’ highly-emotional brains work.

TQQQ has beaten UPRO historically in terms of sheer performance. But don’t succumb to recency bias. Past performance does not indicate future performance. More importantly, large cap growth stocks are now looking extremely expensive relative to history and are at the valuations we saw in 2000 at the height of the tech bubble, meaning they now have lower future expected returns. To make things worse, fundamentals of these companies do not explain these valuations. The current situation is simply the result of an expansion of price multiples.

Value stocks, on the other hands, are looking extremely cheap, meaning they now have greater expected returns. Of course, we expect Value to outperform every day when we wake up anyway due to what we think is a risk factor premium. If you buy TQQQ, you won’t own any Value stocks. TQQQ is purely large cap growth stocks, the segment with lower expected returns. You also won’t own any small- or mid-cap stocks, which have outperformed large stocks historically.

The valuation spread between Value and Growth was recently as large as it’s ever been. Historically, wide value spreads have also reliably preceded massive outperformance by Value. At the end of the day, we’re still paying for a discounted sum of all future cash flows; Growth cannot get more expensive forever. Unfortunately, there's no leveraged Value ETF.

People like to claim “tech is the future!” That may be true, but that doesn’t have much to do with stock market returns, which are not correlated with GDP. The economy is not the stock market, and the stock market is not the economy. Remember that extremely high expectations for these tech firms are already priced in, and they will have to exceed those expectations in order to beat the market. Moreover, good companies tend to make bad stocks and bad companies tend to make good stocks.

Also remember that you don’t need a “tech tilt” anyway; the market is already over 30% tech at this point. The NASDAQ 100 is basically a tech index at this point; it's realistically about 70% tech, posing a sector concentration risk, which is uncompensated risk.

While I don't employ or condone market timing, we also must acknowledge the fact that we may see rising interest rates sometime in the near future, and TQQQ inherently has more interest rate risk than UPRO. Moreover, TQQQ by definition excludes Financials, which tend to do well when interest rates rise.

Now may be the worst time to overweight large cap growth, but my time machine is broken. Only time will tell which index outperforms. We can’t know the future, but I would argue that’s the reason for broad diversification in the first place.

Why Not 100% UPRO?

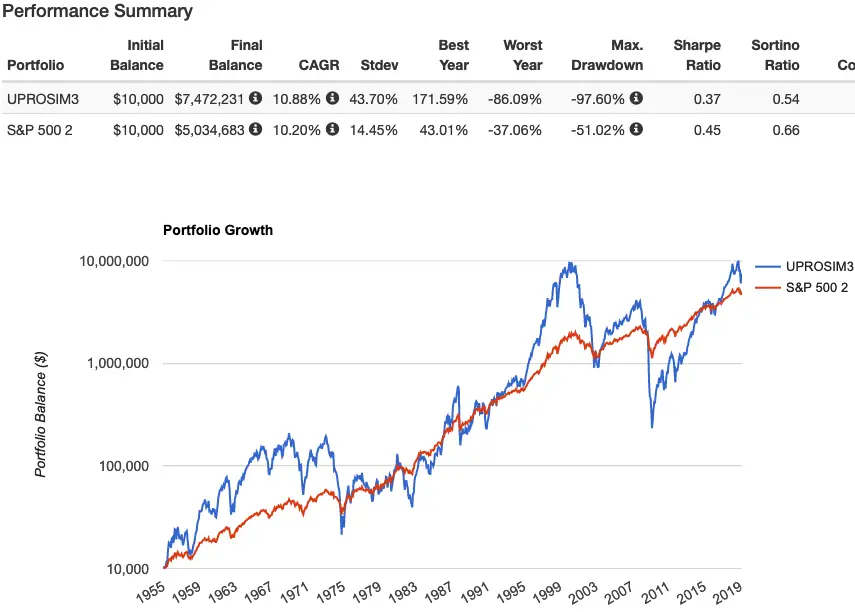

If we're expecting UPRO to be the driver of the strategy's returns, why not go 100% UPRO? Hedgefundie addressed this in the original Bogleheads thread by pointing out that in doing so, we'd probably expect super deep drawdowns from which it may take decades to recover. Here's a backtest showing 40/60 UPRO/TMF (Portfolio 1) vs. 100% UPRO (Portfolio 2) to illustrate:

Here's UPRO vs. the S&P 500 going back to 1955:

My Hedgefundie Adventure Performance

Tracking the quarterly change in performance (relative to the initial value; no new deposits) of my Hedgefundie Adventure in my own portfolio starting October 1, 2019:

01/01/2020: +7%

04/01/2020: -2%

07/01/2020: +35%

10/01/2020: +54%

01/01/2021: +79%

04/01/2021: +67%

07/01/2021: +105%

10/01/2021: +105%

01/01/2022: +150%

04/01/2022: +98%

07/01/2022: +14%

10/01/2022: -14%

01/01/2023: -10%

04/01/2023: +5%

07/01/2023: +11%

10/01/2023: -14%

01/01/2024: +16%

Alternative Options To the Hedgefundie Portfolio

If you want to utilize a leveraged strategy similar to that proposed by Hedgefundie but be completely hands off, PIMCO has been doing something similar for years with their StocksPLUS Long Duration Fund (PSLDX) since 2007. I reviewed the fund here. Note that you can only access this fund through certain brokers, and it may have a minimum investment requirement and transaction fees. Those details are beyond the scope of this post; ask your broker if it's available to you.

Similarly, if you're doing this with a small portion of your portfolio or if you want to employ a leveraged strategy in a taxable account, WisdomTree's NTSX may be a suitable option, effectively providing 1.5x leverage on a traditional 60/40 stocks/bonds portfolio. It holds 90% straight S&P 500 stocks and 10% treasury futures to achieve effective notional exposure of 90/60 stocks/bonds. I reviewed the fund here.

Bogleheads user MotoTrojan proposed a variant by which you can match the volatility of Hedgefundie's 55/45 UPRO/TMF, tone down the leverage a bit, and save some on the expense ratio of TMF by utilizing Vanguard's Extended Duration Treasury ETF (EDV) in a ratio of 43/57 UPRO/EDV. Here's an M1 pie for that. This variant would also be more tax-efficient than the original strategy that uses TMF if you're doing this in taxable.

Rapidly rising interest rates and/or runaway inflation are the primary risks for this strategy. If those concerns are material to you and make you hesitant about this strategy, or if you simply want more diversification across asset types, then a leveraged All Weather Portfolio may appeal to you. There are also some diversifiers listed below.

Addressing Concerns Over Long-Term Treasury Bonds

I've gotten a lot of questions about – and a lot of the discussion in the original Bogleheads thread has been about – the use, utility, and viability of long-term treasury bonds as a significant chunk of this strategy. I'll briefly address and hopefully quell these concerns below.

Again, by diversifying across uncorrelated assets, we mean holding different assets that will perform well at different times. For example, when stocks zig, bonds tend to zag. Those 2 assets are uncorrelated. Holding both provides a smoother ride, reducing portfolio volatility (variability of return) and risk.

Common comments nowadays about bonds include:

- “Bonds are useless at low yields!”

- “Bonds are for old people!”

- “Long bonds are too volatile and too susceptible to interest rate risk!”

- “Corporate bonds pay more!”

- “Interest rates can only go up from here! Bonds will be toast!”

- “Bonds return less than stocks!”

So why long term treasuries?

- It is fundamentally incorrect to say that bonds must necessarily lose money in a rising rate environment. Bonds only suffer from rising interest rates when those rates are rising faster than expected. Bonds handle low and slow rate increases just fine; look at the period of rising interest rates between 1940 and about 1975, where bonds kept rolling at their par and paid that sweet, steady coupon. Rates also rose steadily from 2016 to mid-2019, during which time TMF delivered a positive return.

- Bond pricing does not happen in a vacuum. Here are some more examples of periods of rising interest rates where long bonds delivered a positive return:

- From 1992-2000, interest rates rose by about 3% and long treasury bonds returned about 9% annualized for the period.

- From 2003-2007, interest rates rose by about 4% and long treasury bonds returned about 5% annualized for the period.

- From 2015-2019, interest rates rose by about 2% and long treasury bonds returned about 5% annualized for the period.

- New bonds bought by a bond index fund in a rising rate environment will be bought at the higher rate, while old ones at the previous lower rate are sold off. You're not stuck with the same yield for your entire investing horizon.

- We know that treasury bonds are an objectively superior diversifier alongside stocks compared to corporate bonds. This is also why I don't use the popular total bond market fund BND. It has been noted that this greater degree of uncorrelation between treasury bonds and stocks is conveniently amplified during periods of market turmoil, which researchers referred to as crisis alpha.

- Again, remember we need and want the greater volatility of long-term bonds so that they can more effectively counteract the downward movement of stocks, which are riskier and more volatile than bonds. We're using them to reduce the portfolio's volatility and risk. More volatile assets make better diversifiers. Most of the portfolio's risk is still being contributed by stocks. Let's use a simplistic risk parity example to illustrate. Risk parity for UPRO and TMF is about 40/60. If we want to slide down the duration scale, we must necessarily decrease UPRO's allocation, as we only have 100% of space to work with. Risk parity for UPRO and TYD (or EDV) is about 25/75. Parity for UPRO and TLT is about 20/80. etc. Simply keeping the same 55/45 allocation (for HFEA, at least) and swapping out TMF for a shorter duration bond fund doesn't really solve anything for us. This is why I've said that while it's not perfect, TMF seems to be the “least bad” option we have, as we can't lever intermediates (TYD) past 3x without the use of futures.

- This one's probably the most important. We're not talking about bonds held in isolation, which would probably be a bad investment right now. We're talking about them in the context of a diversified portfolio alongside stocks, for which they are still the usual flight-to-safety asset during stock downturns. Specifically, for this strategy, the purpose of the bonds side is purely as an insurance parachute in the event of a stock crash. Though they provided a major boost to this strategy's returns over the last 40 years while interest rates were dropping, we're not really expecting any real returns from the bonds side going forward, and we're intrinsically assuming that the stocks side is the primary driver of the strategy's returns. Even if rising rates mean bonds are a comparatively worse diversifier (for stocks) in terms of future expected returns during that period does not mean they are not still the best diversifier to use.

- Similarly, short-term decreases in bond prices do not mean the bonds are not still doing their job of buffering stock downturns.

- Historically, when treasury bonds moved in the same direction as stocks, it was usually up.

- Interest rates are likely to stay low for a while. Also, there’s no reason to expect interest rates to rise just because they are low. People have been claiming “rates can only go up” for the past 20 years or so and they haven't. They have gradually declined for the last 700 years without reversion to the mean. Negative rates aren't out of the question, and we're seeing them used in some foreign countries.

- Bond convexity means their asymmetric risk/return profile favors the upside.

- Again, I acknowledge that post-Volcker monetary policy, resulting in falling interest rates, has driven the particularly stellar returns of the raging bond bull market since 1982, but I also think the Fed and U.S. monetary policy are fundamentally different since the Volcker era, likely allowing us to altogether avoid runaway inflation environments like the late 1970’s going forward. Bond prices already have expected inflation baked in.

David Swensen summed it up nicely in his book Unconventional Success:

“The purity of noncallable, long-term, default-free treasury bonds provides the most powerful diversification to investor portfolios.”

Ok, bonds rant over. If you still feel some dissonance, the next section may offer some solutions.

Reducing Volatility and Drawdowns and Hedging Against Inflation and Rising Rates

It's unlikely that any of the following will improve the total return of the portfolio, and whether or not they'll improve risk-adjusted return is up for debate, but those concerned about inflation, rising rates, volatility, drawdowns, etc., and/or TMF's future ability to adequately serve as an insurance parachute, may want to diversify a bit with some of the following options:

- LTPZ – long term TIPS – inflation-linked bonds.

- FAS – 3x financials – banks tend to do well when interest rates rise.

- EDC – 3x emerging markets – diversify outside the U.S.

- UTSL – 3x utilities – lowest correlation to the market of any sector; tend to fare well during recessions and crashes.

- YINN – 3x China – lowly correlated to the U.S.

- UGL – 2x gold – usually lowly correlated to both stocks and bonds, but a long-term expected real return of zero; no 3x gold funds available.

- DRN – 3x REITs – arguable diversification benefit from “real assets.”

- EDV – U.S. Treasury STRIPS.

- TYD – 3x intermediate treasuries – less interest rate risk.

- UDOW – 3x the Dow – greater loading on Value and Profitability factors than UPRO.

- TNA – 3x Russell 2000 – small caps for the Size factor.

- TAIL – OTM put options ladder to hedge tail risk. Mostly intermediate treasury bonds and TIPS.

- PFIX – OTC payer swaptions on interest rate changes; effectively shorting long bonds.

The Hedgefundie Portfolio ETF Pie for M1 Finance (UPRO/TMF)

Again, most users are utilizing M1 Finance to deploy the Hedgefundie strategy due to its dynamic rebalancing with new deposits, zero transaction fees, and its simple, 1-click rebalance that you can do quarterly. It takes no more than 30 seconds every 3 months. I wrote a comprehensive review of M1 Finance here.

The risk parity 40/60 portfolio would be this pie which looks like this:

- 40% UPRO

- 60% TMF

To add this pie to your portfolio on M1 Finance, just click this link and then click “Save to my account.”

The updated 55/45 portfolio would be this pie which looks like this:

- 55% UPRO

- 45% TMF

To add this pie to your portfolio on M1 Finance, just click this link and then click “Save to my account.”

Canadians can find the above ETFs on Questrade or Interactive Brokers. Investors outside North America can use eToro or possibly Interactive Brokers.

M1 currently has a promotion for up to $500 when initially funding an investment account:

Disclosures: I am long PSLDX, NTSX, UPRO, and TMF in my own portfolio.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. All examples above are hypothetical, do not reflect any specific investments, are for informational purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Don't want to do all this investing stuff yourself or feel overwhelmed? Check out my flat-fee-only fiduciary friends over at Advisor.com.

As an Australian investor, there is possibly another interesting layer of downside protection when implementing this strategy.

There is a positive correlation between the AUD/USD and S&P 500 (negative in the USD/AUD pair). The AUD has tended to crash significantly along with the S&P 500, which can at time completely eliminate the drawdown when dominated back into AUD. e.g. the 50% and 35% drawdowns in the S&P 500 during the GFC and COVID-19 was offset by the 50% and 15% decline in the AUD. Over the long run currencies average out and shouldn’t affect long term returns, but in the short run can provide interesting diversification properties.

What are your thoughts?

You said in your Ginger Ale Portfolio (My Own Portfolio) that you bucketed this strategy

Why not fix it as a static allocation? i.e. 30% Hedgefundie 70% Ginger Ale? Would it not smooth out your returns/risks? Forcing you to take profits along the way when it’s working and putting it in when it’s not (and arguably where most of the returns will come from when rallying from market bottoms)

It would also achieve a constant leverage ratio of 2:1 as advocated by Lifecycle Investing at the optimum leverage ratio for young investors. You could have a glide path for the Hedgefundie allocation as well to reduce the overall portfolio leverage down as you approach older age

No right answers and a matter of preference, just curious why the bucketed approach over a static or glide path approach

Because I still recognize it’s a high risk strategy with the possibility of going to zero. Including it in the portfolio and continuing to contribute to it would probably have me feeling uneasy.

That’s very honest. I love how you included the backtest with rolling returns, few do this, it’s much more helpful than using selective time periods

Have you considered doing or seen a monte carlo or other out of sample simulation to see how this performs?

Also, 30% 3x and 70% 1x would be 1.6, not 2:1. 2:1 would require 50% 3x and 50% 1x.

I take it you’re not a market timing person and prefer a all weather / set and forget strategy, but…

What do you think of doing this with a volatility overlay? i.e. exit the strategy or switch out UPRO/TMF during periods of high volatility? All the returns are from a levered bet during a uptrend typically associated with low volatility periods and vice versa. Could you not capture a lot of the returns and reduce a lot of downside with a volatility overlay?

This type of approach was discussed in the original thread.

Just now discovering this website. Kudos on a great job!!

I’ve never been a fan of bonds, but can understand your justification for them. I worry too much that rising interest rates will negate the hedging effect in the years ahead. Curious of your thoughts on a simple 50:50 mix of 2X ETFs (QLD and SSO) along with a Golden Cross/Death Cross signal using 20/50/100 EMAs for entering and exiting positions? These 2X ETFs are less volatile than 3X and have enough liquidity to get out of if needed fairly quickly. The biggest risk to being in the markets seems to be long, drawn out declines over several months to years (2000, 2008, 2018, etc). Why not just avoid them all together as much as possible while utilizing leverage???

The thread is huge. This was really nice!

I’ve heard of a few using this strategy by shorting inverse leveraged ETFs. On the surface that sounds like the kind of crazy internet thing you should never do. -60% SPXU and -40% TMV, monthly rebalance looks to significantly outperform the UPRO/TMF strategy, and interestingly it had mostly flat returns in Feb ’20 and gained 20% in March ’20, when the S&P lost 7.9% and 12.4% respectively.

Would the explanation for this be that in shorting the inverse leveraged ETFs one gains the fees, tracking error, and volatility drag as alpha? At the very least it doesn’t seem at a glance that inverse leveraged ETFs make the promised gains when the market crashes.

Is there any legitimacy to this theory or are these advantages just random noise?

This idea was discussed in the thread and I don’t remember the details of why it was a no-go. I’d imagine liquidity would be more of a concern with the inverse funds.

Wondering if comments are closed…

They’re not.

Had a comment that never showed about jumping in and out based on the 200/235 MA. It was brought up on Reddit/Bogleheads and I’d love to hear your take on it.

I might have missed that discussion on BH. Admittedly I have no experience with and no real interest in MA strategies, other than my charting days over a decade ago.

It seems like it would pay off in that you would miss some of the very down days. Personally, it seems like it would be very tough to have the discipline to jump in and jump out. I have a hard time just jumping in so,without discipline and controlled emotions it might just be a better strategy to buy and hold.

So in this environment of inflationary fears, obviously the market is taking a tumble. Would this make it a good entry point into this strategy as prices are somewhat lower? Maybe a percentage of the Roth portfolio in UPRO and leaving TMF out of it until we get a better picture of rates? Wouldn’t the lower rates make the bonds perform terribly?

Trying to time the market is usually more harmful than helpful.

I ended up allocating 25% of my Roth’s now with this strategy, UPRO/TMF. I’ve seen in the past week the difference in holding TMF, it’s been holding when UPRO’s been down. Are you doing this with a portion of your portfolio as well? I notice you state you are long VTI as well. How are you bonds allocates is it just TMF? Or is that only reserved for the HF strat. Thanks.

Yea I’ve got a lottery ticket in my version of the HFEA. I have bond exposure through NTSX and PSLDX as well.

I am wondering how would it impact the results if we replaced UPRO with TECL?

TECL is a single sector. Not sure why you’d want to do that.

Out of curiosity, did you deploy your adventure in the UPRO/TMF or UPRO/EDV portfolio?

I know Bogleheads preaches the lowest expense ratio (assume all equal), so wonder if you think that there is any downside to saving a few bucks with EDV.

Thanks in advance.

UPRO/TMF

I’ve really tried to find ways to hedge this portfolio against inflation. The best I can think of are natural resource etfs like COPX, GDXJ, and XOP. Natural resource stocks actually do ok in high inflation environments, so you shouldn’t get completely destroyed.

https://www.vaneck.com/us/en/blogs/natural-resources/all-things-reconsidered-in-the-inflation-debate/

The pure play natural resource etfs also have crazy standard deviations, so they are around the same volatility as UPRO and TMF.

Another fantastic article John!

I have been hunting around for a factor tilted version of this, and i stumbled onto the offerings by UBS Etracs, have you had any experiences with them and are they a feasible inclusion ?

tickers: IWFL(growth factor), IWML(size factor), IWDL(value Factor), MTUL(momentum),QULL(Quality factor)

That said they are 2x leverage, so it might fit better with a SSO/UBT portfolio.

Thanks !

Matthew

Thanks!

I actually hadn’t seen these. Unfortunately, I doubt these will gain much traction, and they’re structured as ETNs which is disappointing.

Interesting, nonetheless; thanks for pointing me to them.

Have you heard of the TAIL Risk ETF by Cambria? The details are here: https://www.cambriafunds.com/assets/docs/Cambria_Tail_FAQ.pdf

I am curious to know what you think about pairing TAIL with UPRO and how to go about calculating the best allocation?

Yep. Expensive insurance that doesn’t even seem to work.

I had looked into it myself a while back, it didn’t move up enough during the 2020 virus crash enough to be worth it.

I studied your leveraged porfolios AWP and HFEA. They are all impressive. Somehow I saw this article that against leveraged porfolios. To be honest the inforamtion in the article is a bit beyond me so I would like to know what is your opinion about this? Thanks.

https://www.mindfullyinvesting.com/why-not-use-leverage-another-tug-on-the-lever/

Hey Josh, thanks for the kind words.

As the article notes, most of the points brought up have been discussed ad nauseam in the original thread on the Bogleheads forum. It basically comes down to one’s view of U.S. monetary policy. The article is more agnostic toward interest rate environments. If you believe interest rates will – or even have the ability to – rise rapidly for an extended period, then long term treasuries – and subsequently this strategy – may not be the best idea. If, however, you believe that the Fed now knows which levers to pull to avoid what we saw in the late 1970’s before Volcker, then I think the situation is not as dire as that article makes it out to be. In any case, obviously we don’t know the future, and past results are not necessarily indicative of future results. Moreover, Hedgefundie always reminded people not to put one’s entire portfolio in this strategy, but rather treat a small piece as a “lottery ticket.”

Thanks John. The explanation is clear to understand. But then I come up with another question.

If we look into 3x AWP its 55% LTT and 30% UPRO. I know we have another 15% for as a cusion compared to HFEA.

We know we shouldnt all-in to HFEA (As you mentioned he suggests only 10%-15% of capital). Base on the similarity of HFEA and 3x AWP. Is it ok to all-in or monthly invest to 3x awp?

Thanks alot.

As with all things, it largely comes down to personal time horizon and risk tolerance. I personally wouldn’t go all in on any of these leveraged strategies. Also depends on what overall leverage ratio you’re aiming for in your portfolio; 50% “normal” unleveraged and 50% 3x results in a total leverage ratio of 2. All things being equal, greater leverage is more suitable for young investors with a long time horizon and high tolerance for risk, whereas an investor at retirement probably shouldn’t be levered up at all.

Hi John:

Great job summarizing the strategy. Could you comment on how the bond portion of the portfolio can help offset the stock portion when long bond prices at at record lows. I just can’t seem to wrap my head around a situation where the bond portion will rise any time in the near term. I guess interest rates could go down slightly but there just doesn’t seem to be any room in this environment. Thank you!

Bond convexity. Moreover, remember that just because interest rates are low does not mean they will rise. They have gradually declined for the last 700 years. Bonds remain the best diversifier alongside stocks because they are currently still the asset with the lowest correlation to stocks. Lastly, the bond portion of this strategy is essentially insurance; we don’t really care as much about its performance in isolation.

I think the likelihood of rates rising in the near (year or two from now) term is bothering me too, although I am planning to try out this portfolio. Its interesting that rates have declined over 700 years. However, now that we are at zero, there is nowhere else to go, it seems. I guess they could go negative… What were previous time periods when rates rising and how did this portfolio perform during that time?

Thanks.

Thank you John for the info and your great site. I have a question regarding holding a leveraged ETF position inside a taxable account. Are there any different tax consequences of these leveraged ETFs compared to unleveraged ETFs that I should pay attention to?

Thanks for the kind words, Justyn! To answer your question, yes, definitely. The daily resetting of these funds makes them unsuitable for a taxable environment if you can avoid it. We would hope the enhanced returns would make up for the tax consequences over the long term, but the taxes will definitely eat into your returns. Utilizing NTSX and/or margin would be a much more tax-efficient approach (compared to leveraged ETFs) if you want to use leverage in a taxable account.

Thanks for the answer. So with that said, how do you feel jumping into these leveraged ETFs in this current bull market with pricing in mind? Would you wait for a dip then buy in a lump sum? I’m already maxed out for 2021, so would need to sell some positions to make room for such a portfolio.

I neither employ nor suggest market timing, so I wouldn’t wait around for a dip that may not come for a long time.

Forgot to mention that MotoTrojan’s EDV variant would also be comparatively more tax-efficient than the Adventure with TMF.

Great website and youtube videos. Thank you for sharing your information. Could you explain this I do not understand “The daily resetting of these funds makes them unsuitable for a taxable environment” or is there a link where I can find more information on this? I understand in a taxable account with regular stocks and ETFs but its not very clear in the Leveraged ETFs.

Thanks, Martin! Basically, LETFs have much higher turnover, transaction costs, and subsequent tax implications than “normal” ETFs, so they should usually be avoided in a taxable environment if you can help it. You’d also need to rebalance the portfolio, which would incur further taxes.

Great write up

Hedgefundie is no longer participating in the boglehead forums.

Thanks!

Sadly, I’m aware. ☹️

Thank you for summarizing the excellent adventure. I started this trip with TQQQ in place of URPO about a year ago. I have been adding $100-500 every week instead of rebalancing. So far its worked well. Late feb 2020 was certainly gut wrenching.

No prob, Rick! Thanks for your comment. I’ve seen many people doing that tech tilt using a combination of TQQQ and UPRO for the equities side. Glad it’s working well for you.

How is TQQQ working out? It took a huge beating , down to $30 from $140, back to $180 now. I am selling puts and selling covered calls, sort of a wheel strategy.

I don’t own TQQQ.

Thanks for a interesting post and site. One quick question why not trade this 55/45 strategy in Traditional IRA for somebody having 15 years horizon ?

Hey RK,

Thanks for the kind words. You could still do that. Would come down to your personal risk tolerance. I wouldn’t be levered up 3x with the bulk of my portfolio with only a 15-year time horizon though.

Thanks for sharing this and it is a very helpful strategy!

I posted my questions here but did not see it showed. If you see it, please just ignore the other one then.

I love this strategy. However, I am just wondering what are the scenarios that UPRO and TMF get delisted or return to zero? ( I know if S&P500 drops more than 33% in a day, UPRO might be zero; however, what about it drops more than 33% in a 2-3 day period and no single day drop more than 33%?)

Also, what will happen to UPRO and TMF this type of market link ETFs, if the parent company goes bankrupt? I am just thinking about different scenarios that can happen which stopped our long term investment in this leveraged portfolio.

Thanks a lot!

Grace

Hey again, Grace. I don’t see any other comments from you that came through on this post.

Delisting or deleveraging would be up to the ETF houses, in this case ProShares and Direxion. These are 2 of the most highly traded (high volume) ETF’s, so I doubt that would happen unless any new regulations interfere. There are some proposed regulations to tighten up the accessibility of leveraged products by average investors, but that’s another conversation. Some 3x sector ETF’s have also recently been downgraded to 2x due to their extreme volatility during the recent market turmoil.

Currently circuit breakers on the S&P 500 kick in at 7%, 13%, and 20%. This happened a couple times during the recent crashes. These leveraged ETF’s reset daily, so drops over several days wouldn’t matter. Because of these facts, technically it is impossible for them to actually go to zero.

The providers going bankrupt would mean the shares would be liquidated at their market value and you’d get that amount in cash. The prospectus for each fund should detail that process.

Scenarios that would be bad news for this strategy, albeit likely only temporarily in my opinion, include rising interest rates, hyperinflation, and bonds no longer being a flight-to-safety asset.

If you have the time and desire, I’d encourage you to read through the Bogleheads threads on the strategy. There are some great nuggets and discussions in there.

Hi John,

Loving this blog.

Quick question: How were you able to enter UPROSIM and TMFSIM as tickers?

Are you on portfoliovisualizer.com?

Thanks!

Hey Randy, glad you’re liking it!

If you read through the Bogleheads thread, one of the users created the SIM data that goes back pretty far. For a quick and easy way, you can use mutual funds and a negative cash position like this.

Awesome, thank you!

What sort of external factors could cause the treasury bonds to fall at roughly the same time as stocks falling? Is there any way to see what this portfolio would have looked like during the 2008 economic crash?

Rising interest rates, hyperinflation, bonds no longer being a flight-to-safety asset, a number of things. Keep in mind though that the bonds are really just for crash insurance in this context. The backtests above include the 2008 crash.

How do you feel about adding an inflation hedge for this? I guess it becomes more like the golden butterfly or all weather but adding some $FXF(Swiss Francs) or $CPI

The Hedgefundie strategy largely intrinsically assumes that post-Volcker (1982), the Fed will be able to altogether avoid a hyperinflationary environment, as well as the fact that any reliable inflation hedge would likely just drag down returns.

I just came up with the identical strategy independently (I initially went with SSO but then found UPRO in the last couple of days) and Googled it to see if anyone had already tried it and your blog came up! Great minds think alike, I suppose, lol.

Just curious, I have yet to put real money against this strategy, but I noticed in my backtest spreadsheet that in the 3/6/20-3/18/20 period the equity crashed 44.20% (based on your 55/45 weighting). It rebounds to new highs by 6/2/20, but talk about a wild ride! Did you experience this wild swing, and if so did you hold on for dear life or did you partially exit? I’m still trying to figure out why on 3/11/20 and 3/18/20 in particular both UPRO and TMF tanked together and what could be done to mitigate such occurrences (the VIXY performed well during that period, but it’s otherwise a drag on performance). Thanks for any insight, and keep up the good work!

Catmango,

Thanks for your comment. I can’t really take any credit. Hedgefundie on the Bogleheads forum came up with the specific approach and reasoning behind it.

Yes, you must be comfortable with the wild swings that leverage brings. These are to be expected during crashes. The time period you noted was the COVID crash. Stocks and bonds do move together sometimes, but usually offer an uncorrelation. TMF is basically acts as insurance in this strategy. On days when stocks crash, treasury bonds usually go up. If you look at the individual days, this is precisely what happened, as expected. UPRO alone dropped more than 60% during the time period you noted.

Selling during crashes is one of the worst things you can do. This usually causes people to sell low and buy high. I hold through dips and usually try to buy more. If your risk tolerance dictates that you’d be tempted to sell, this strategy isn’t for you. This strategy is also only a relatively small part of my total portfolio.

I’d encourage you to read through the threads on the Bogleheads forum, titled Hedgefundie’s Excellent Adventure. Members are actually currently suggesting the proposition of using a small amount of VIX as more insurance. I’m personally not a fan of that idea.

> This strategy is also only a relatively small part of my total portfolio

Is there any real meaning to “partitioning” strategies in this way, or do you just end up with a more garbled global portfolio, and do you do backtesting on that global one?

Great question, Zon. Probably depends on how much of one’s portfolio is going into a strategy like this and how the investor is viewing it. Like I noted, if you’re only putting a tiny bit in, you may be better off just using NTSX. There was a good amount of discussion around this concept in the Bogleheads thread. I think in this instance, at least for me, I’m viewing it as a separate partition because I set aside a specific amount of cash aside as a “lottery ticket” like Hedgefundie proposed and I’m not adding new deposits. Others chose to keep adding new deposits to it and view it as part of the global portfolio.

If you’re only going into this as a tiny lottery ticket, why not just buy UPRO and let your “serious” portfolio be the hedge against volatility? Not sure how much benefit there is to adding such a tiny bond portion.

I guess the main point would be the educational factor of seeing how the bucket turns out over the long run.

Depends on one’s risk tolerance and value of the lottery ticket bucket relative to their “normal” portfolio, I suppose. I personally don’t have any unleveraged bonds in my “serious” portfolio to act as a hedge anyway. That is, my “serious” portfolio is already very volatile and risky at this time in my investing horizon.

If I use EDV instead of TLT

Is it 1.5 TLT ? Or more? Thank you

Hi Eric, yes EDV is 1.5x TLT. But note that TLT is not part of the Hedgefundie portfolio.

Great Job! I started a slightly different variation of the portfolio yesterday! 35% stocks, 20 % 10 year treasuries and 45 % long term treasuries.

I follow the Boglehead thread quite closely but this is a really nice and easy to read summary of the whole situation.

Thanks! That was the goal.