NTSX from WisdomTree is a relatively new ETF designed to provide access to asset class diversification without sacrificing returns in order to free up space in diversified portfolios. I think the fund is pretty clever, simple, elegant, and useful. Here's my summary and review.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

NTSX ETF Review Video

Prefer video? Watch it here:

NTSX – The What, Why, and How

NTSX is a relatively new ETF from WisdomTree that launched in late 2018. Its name is the WisdomTree U.S. Efficient Core Fund (formerly WisdomTree 90/60 U.S. Balanced Fund). It holds entirely U.S. securities, investing in 90% straight S&P 500 stocks (think 90% VOO or SPY, for example) and 10% 6x treasury bond futures using a bond ladder of different durations, providing effective exposure of 90/60 stocks/bonds, which is essentially 1.5x leverage on a traditional 60/40 portfolio, considered to be a near-perfect balance of risk and expected return.

Hopefully you didn't exit out of the page after you read the word “leverage.” Leverage per se gets a bad rap from survivorship bias and confirmation bias, because you only hear about the extreme cases, which are usually disastrous. In the right circumstances, I think it can be particularly useful and can even decrease risk, such as with the idea of Lifecycle Investing, applying leverage while young and deleveraging as you get older in order to diversify across time.

I'm always talking about how young investors with a long time horizon can reasonably expect to boost returns and possibly beat the market by using a “modest” amount of leverage applied to a broad index (or preferably, multiple indexes), and that this is statistically a far better bet than stock picking. “Modest” is admittedly subjective, but I'd say it's anything between 1 and 1.5.

I think NTSX perfectly embodies that idea. It's effectively applying 1.5x leverage but doing so with a diversified allocation of stocks and bonds (technically, bond futures), which are uncorrelated to each other, meaning when stocks zig, bonds tend to zag. This reduces the portfolio's volatility and risk. The traditional belief is that bonds – and more specifically, treasury bonds – are inherently less risky that stocks and provide downside protection during stock market crashes. Historically, this has been true. Diversifiers like bonds become more important as we increase portfolio leverage, as drawdowns become more damaging.

The idea is that levering up a balanced 60/40 exposure to 90/60 should provide roughly stock market returns with lower volatility and risk, and indeed this has been the case historically, which I'll illustrate below. Think similar returns to the S&P 500 with smaller drawdowns. We can say that over the long term, on average, compared to 100% stocks, we would expect NTSX to outperform during bear markets unless interest rates are rising faster than expected. I think this makes it a perfect investment for the moderate-risk-tolerance investor who wants returns similar to that of 100% stocks but who can’t stomach the volatility and drawdowns.

This enhanced exposure also makes something like NTSX a particularly attractive investment in the face of lower expected returns for both stocks and bonds in the near future. Rodrigo Gordillo of ReSolve Asset Management coined the term “return stacking,” suggesting that leverage in this context can be an “ally” for those with a long term view. I delved into the concept of return stacking here.

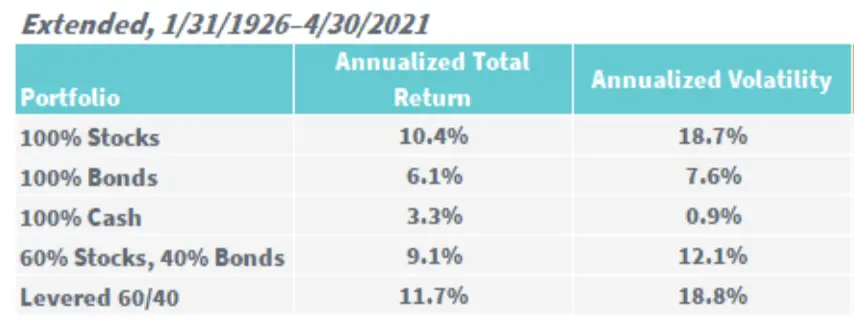

Of course, this idea isn't really new. We know from Markowitz's Modern Portfolio Theory from the 50s that we can allocate assets based on their relative “risk” – not dollar amount – to construct a more efficient portfolio than one of a single asset, and then we can lever up to increase exposure and subsequent expected returns. Cliff Asness showed that a 60/40 portfolio levered up to match the volatility of 100% equities has delivered higher returns historically. This is exactly what NTSX does. Here's how that would have worked out historically, from 1926 to 2021:

NTSX is an “Efficient Core” indeed. The fund only uses leverage on the bonds side in the form of futures contracts on treasury bonds, so no credit risk. The stocks side is unleveraged – just roughly 500 U.S. large cap stocks similar to the S&P 500. This is a simple yet elegant way in which NTSX was specifically built with tax-efficiency in mind, making it one of the few (if not the only) leveraged funds appropriate for a taxable account. Futures are taxed as 60% long term capital gains and 40% short term capital gains, as opposed to traditional bond interest being taxed as ordinary income. In fact, NTSX even has a lower tax cost than VTI!

It’s also cheaper to lever up bonds than stocks, and by using futures on a bond ladder, they’re not using daily-reset leverage usually seen with leveraged ETFs, so no volatility decay to worry about, and we're also largely avoiding counterparty risk, as bond futures markets are highly liquid. Even Bogleheads seem to like it for all these reasons.

All this comes at what I think is a low cost of only 0.20% for a packaged solution that novice investors would likely not be able to implement on their own. It's also been speculated that this is precisely the reason why the fund hasn't soared in popularity among portfolio managers. The theory is that ETFs that combine asset classes for you aren’t popular among advisors because they’re doing the work of the advisor. The aforementioned negative perception of the word “leverage” may also have something to do with it.

Those wanting a DIY version of this fund with ETFs can achieve roughly the same exposure with 90% VOO (S&P 500) and 10% TMF (3x long treasuries), rebalanced monthly, but it would be pretty tax-inefficient. You’d also still have an overall fee of roughly 0.13%, not to mention all the unwanted things like volatility decay, counterparty risk, greater borrowing costs, etc. A DIY version just doesn’t seem worth it in my opinion when NTSX itself is already sufficiently liquid, simple, elegant, relatively low-cost, and incredibly tax-efficient. You could also just buy treasury futures yourself, but that doesn't really seem worth the hassle either.

NTSX can be thought of as essentially a milder, cheaper version of the famous Hedgefundie Adventure.

NTSX vs. SWAN

NTSX is not unlike SWAN, though SWAN is designed more specifically for downside protection to hedge against black swan events, as the name suggests, aiming for 70/90 stocks/bonds exposure through options contracts on the stocks side. SWAN also commands a much larger fee and would be comparatively less tax-efficient than NTSX. Also keep in mind that WisdomTree's stated use case for NTSX is to use it to make room for other assets.

That said, these funds are pretty similar. In terms of exposure, NTSX is 1.5x 60/40 for effective 90/60, and SWAN is roughly 1.6x 44/56 for effective 70/90. Note that NTSX's treasury bond futures ladder has an effective average duration of about 7 years, while SWAN's treasury bond ladder aims to match the duration of the U.S. 10-Year Treasury Note.

NTSX Performance vs. the S&P 500 (SPY, VOO, etc.)

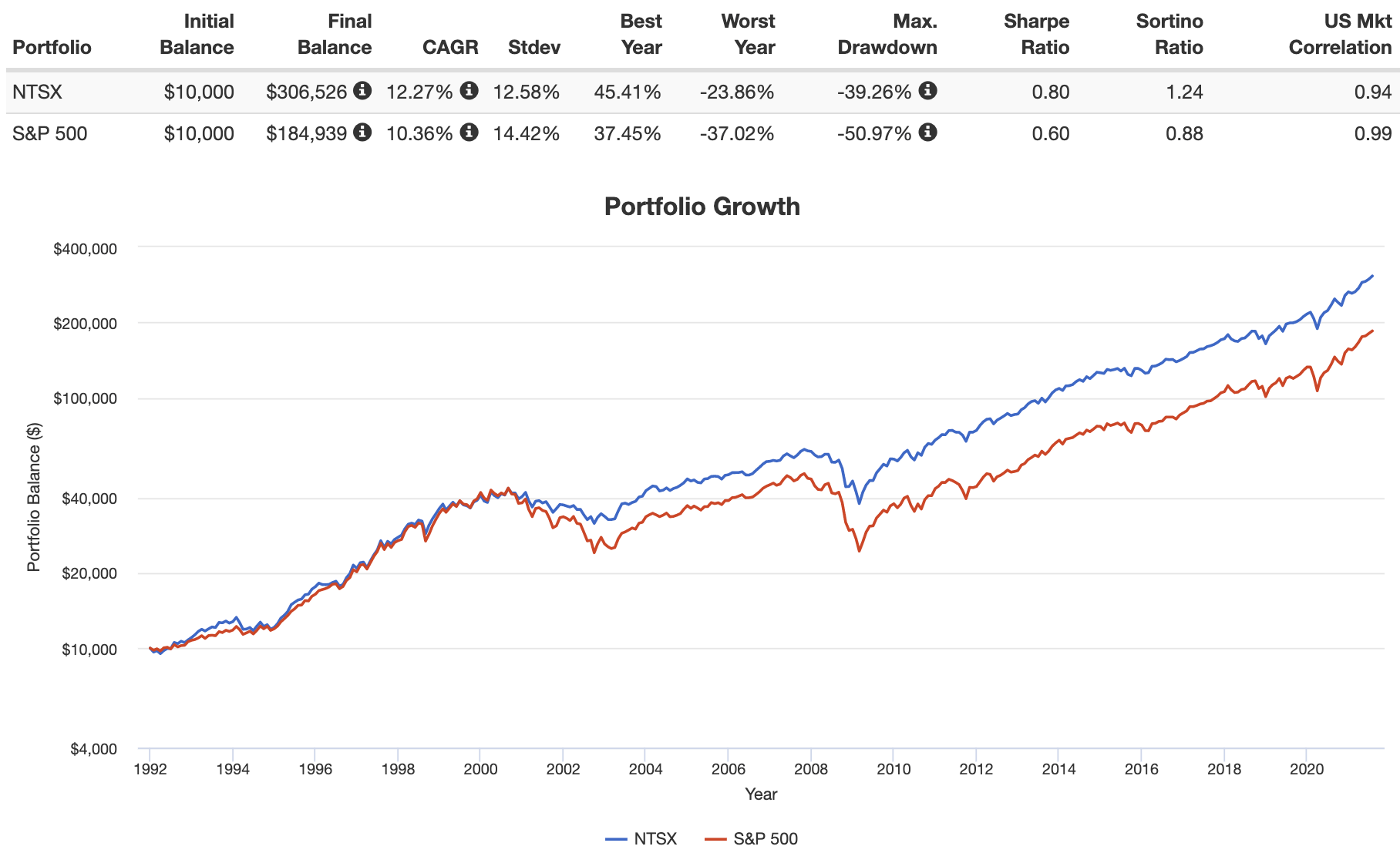

Remember, NTSX was designed to roughly deliver stock market returns but with lower risk. Conveniently, the bond bull market over the last 40 years or so has allowed a 90/60 portfolio to deliver above-market returns with lower risk. Here's a simulated approximation of NTSX vs. the S&P 500 from 1991 through July, 2021:

Use Cases for NTSX

Interestingly, NTSX is suitable for different investors with different goals depending on how it's used. For a young investor in the accumulation phase, 100% NTSX wouldn’t be a bad idea. You’d basically be treating it like a less volatile S&P 500 fund. This use case is illustrated in the backtest above. This would again simply be a 90/60 portfolio in a single fund, though note that your equities exposure would be entirely U.S. large caps.

The primary use case suggested by WisdomTree themselves, on the other hand, suitable for older investors, even retirees, or anyone wanting more diversification, would be to use this fund at around 67% and diversify with that other 33% across other assets to further reduce the volatility and risk of the portfolio. The possibilities here are endless: international stocks, TIPS, factor tilts, gold, etc. Ideally, this would mean adding assets that aim to address a risk that both stocks and bonds suffer, such as TIPS for inflation risk. This could also mean simply adding assets that tend to be lowly correlated to both stocks and bonds, such as gold.

In this sense, NTSX basically provides a way to hold a traditional 60/40 portfolio – considered a near-perfect balance of risk and return – and still have room to diversify further. WisdomTree themselves state they aim to “boost the capital efficiency in the core to allow investors more flexibility” with these products.

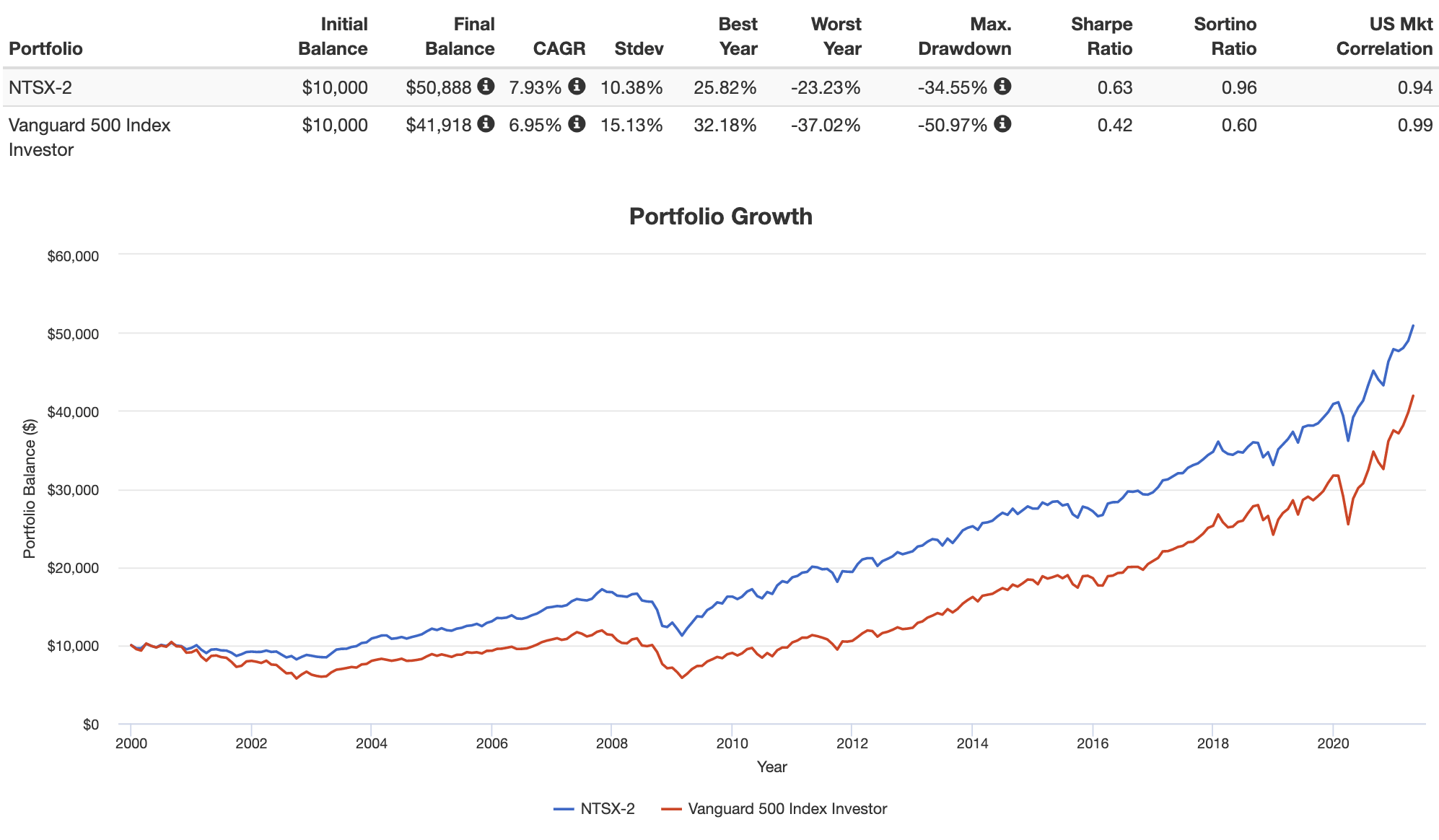

A reasonable portfolio for this diversification use case in my mind, if one’s desire is to reduce volatility and risk, would be something like this:

- 60% NTSX

- 10% Small Cap Value

- 10% Emerging Markets

- 5% Developed Markets

- 10% TIPS

- 5% Gold

Here's a backtest of this use case vs. the S&P 500 from 2000 through April, 2021:

This portfolio would provide effective exposure of 79/46/5 stocks/bonds/gold.

Here's a link for that pie for M1 Finance if you're interested. I wrote a comprehensive review of the M1 platform here if you're interested.

Canadians can find the above ETFs on Questrade or Interactive Brokers. Investors outside North America can use Interactive Brokers.

Risks for NTSX

Originally, fundamental risks of liquidity and fund closure were concerns. I got into NTSX when its AUM was a little under $100M, with the cautious expectation that it may close within the year. Thankfully, AUM has now grown to around 6X that, approaching $600M. Again, it seems that it hasn't taken off with retail investors perhaps because it seems like a sophisticated product (with no marketing behind it), and it hasn't taken off with advisors/managers because it potentially puts them out of a job.

An obvious shortcoming of this fund – solved somewhat by the above proposed use case – is the lack of geographical diversification in equities. WisdomTree may have heard that complaint from investors; they recently filed for 2 new products like NTSX using Developed Markets and Emerging Markets. Whether or not those will materialize into viable ETFs is another story yet to be seen.

Update – May 20, 2021: Today, those two ETFs – NTSI and NTSE – launched for Developed Markets and Emerging Markets, respectively. I'm curious to see if they attract assets.

Update – August 9, 2021: A little less than 3 months later, NTSI and NTSE still have concerningly-low AUM of about $16 million and $2 million respectively. I'm hopeful they'll grow and stick around, but only time will tell. I still don't own them.

Update – January 3, 2022: NTSI and NTSE have attracted more assets and now have about $86M and $36M respectively. Industry rule of thumb says a “safe” minimum is $50M, after which fund closure becomes much less likely. So these two newer funds are now more attractive and viable in my opinion. I'm hoping the trend continues upward. I still don't own them at this time. Volume and spread still appear to be worse for NTSE, as we'd expect.

Update – February 18, 2022: Time flies. A year later, NTSI and NTSE have now attracted assets of about $217M and $50M respectively.

Update – June 2024: Time flies. NTSX, NTSI, and NTSE now have assets of $1B, $330M, and $27M respectively. NTSX and NTSI are now far away from the chopping block, though weirdly NTSE went in the opposite direction and pales in comparison to its older sister funds. I'd like to think that the success of NTSX and NTSI would help ensure the continued viability of NTSE.

The downfall of NTSX would be what I would argue is a rare simultaneous combination of economic factors: rapidly rising interest rates, runaway inflation, and slow economic growth. But this scenario would also wreak havoc on virtually any diversified portfolio that holds mostly stocks and bonds. This concern can also be mitigated with an allocation to things like TIPS, international stocks, managed futures, and gold, as I suggested above.

I actually think that’s why it’s also important to note that the effective duration of the bond allocation is intermediate (about 7 years), not long-term, posing less interest rate risk. This is why NTSX still outperformed the S&P 500 during periods where interest rates rose slowly. There also tends to be more roll yield to be captured in the middle of the yield curve.

Is NTSX a Good Investment?

So is NTSX a good investment? Maybe.

I think NTSX is an extremely interesting, useful, and clever product that can be inserted into different strategies, risk tolerances, and time horizons. The fund is incredibly tax-efficient, and it provides a packaged solution for retail investors who want the long-term returns of 100% stocks without the associated volatility and risk, all at what I consider to be a pretty low fee. The fund's risks are easily mitigated by diversifying across other assets and geographies, and its intermediate effective bond duration should bode well for future performance even in a rising rate environment.

What do you think of NTSX? Let me know in the comments.

Disclosures: I am long NTSX in my own portfolio. It comprises most of my taxable account. I know it sounds like I'm selling this fund pretty hard, but note that I am not affiliated with WisdomTree at all and I get no sort of kickback or compensation from them if you decide to buy NTSX (or any of the other funds listed here). I've also received no form of compensation from WisdomTree for the words I've written on this page. My discussion and appreciation of NTSX are simply the result of my own independent research and analysis.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Thoughts on GDE?

Breaking news, there is now a World version of this with NTSG 🙂

Yes, it’s an EU UCITS ETF though.

In the long run, Is the 50% additional bond expected to outperform cost of 50% leverage?