NTSX from WisdomTree is a relatively new ETF designed to provide access to asset class diversification without sacrificing returns in order to free up space in diversified portfolios. I think the fund is pretty clever, simple, elegant, and useful. Here's my summary and review.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality, ad-free content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I get if you decide to purchase through my links. Read more here.

Contents

NTSX ETF Review Video

Prefer video? Watch it here:

NTSX – The What, Why, and How

NTSX is a relatively new ETF from WisdomTree that launched in late 2018. Its name is the WisdomTree U.S. Efficient Core Fund (formerly WisdomTree 90/60 U.S. Balanced Fund). It holds entirely U.S. securities, investing in 90% straight S&P 500 stocks (think 90% VOO or SPY, for example) and 10% 6x treasury bond futures using a bond ladder of different durations, providing effective exposure of 90/60 stocks/bonds, which is essentially 1.5x leverage on a traditional 60/40 portfolio, considered to be a near-perfect balance of risk and expected return.

Hopefully you didn't exit out of the page after you read the word “leverage.” Leverage per se gets a bad rap from survivorship bias and confirmation bias, because you only hear about the extreme cases, which are usually disastrous. In the right circumstances, I think it can be particularly useful and can even decrease risk, such as with the idea of Lifecycle Investing, applying leverage while young and deleveraging as you get older in order to diversify across time.

I'm always talking about how young investors with a long time horizon can reasonably expect to boost returns and possibly beat the market by using a “modest” amount of leverage applied to a broad index (or preferably, multiple indexes), and that this is statistically a far better bet than stock picking. “Modest” is admittedly subjective, but I'd say it's anything between 1 and 1.5.

I think NTSX perfectly embodies that idea. It's effectively applying 1.5x leverage but doing so with a diversified allocation of stocks and bonds (technically, bond futures), which are uncorrelated to each other, meaning when stocks zig, bonds tend to zag. This reduces the portfolio's volatility and risk. The traditional belief is that bonds – and more specifically, treasury bonds – are inherently less risky that stocks and provide downside protection during stock market crashes. Historically, this has been true. Diversifiers like bonds become more important as we increase portfolio leverage, as drawdowns become more damaging.

The idea is that levering up a balanced 60/40 exposure to 90/60 should provide roughly stock market returns with lower volatility and risk, and indeed this has been the case historically, which I'll illustrate below. Think similar returns to the S&P 500 with smaller drawdowns. We can say that over the long term, on average, compared to 100% stocks, we would expect NTSX to outperform during bear markets unless interest rates are rising faster than expected. I think this makes it a perfect investment for the moderate-risk-tolerance investor who wants returns similar to that of 100% stocks but who can’t stomach the volatility and drawdowns.

This enhanced exposure also makes something like NTSX a particularly attractive investment in the face of lower expected returns for both stocks and bonds in the near future. Rodrigo Gordillo of ReSolve Asset Management coined the term “return stacking,” suggesting that leverage in this context can be an “ally” for those with a long term view. I delved into the concept of return stacking here.

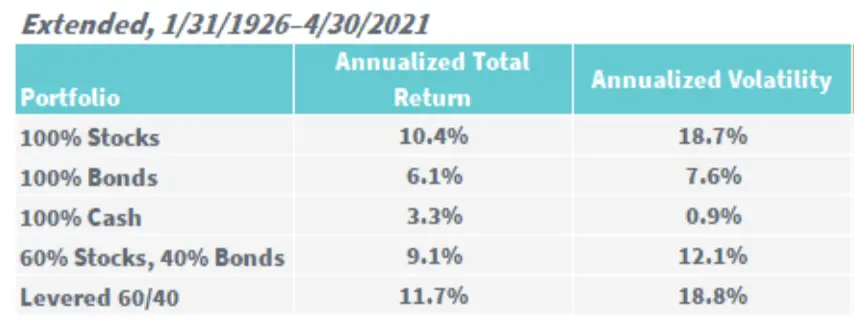

Of course, this idea isn't really new. We know from Markowitz's Modern Portfolio Theory from the 50s that we can allocate assets based on their relative “risk” – not dollar amount – to construct a more efficient portfolio than one of a single asset, and then we can lever up to increase exposure and subsequent expected returns. Cliff Asness showed that a 60/40 portfolio levered up to match the volatility of 100% equities has delivered higher returns historically. This is exactly what NTSX does. Here's how that would have worked out historically, from 1926 to 2021:

NTSX is an “Efficient Core” indeed. The fund only uses leverage on the bonds side in the form of futures contracts on treasury bonds, so no credit risk. The stocks side is unleveraged – just roughly 500 U.S. large cap stocks similar to the S&P 500. This is a simple yet elegant way in which NTSX was specifically built with tax-efficiency in mind, making it one of the few (if not the only) leveraged funds appropriate for a taxable account. Futures are taxed as 60% long term capital gains and 40% short term capital gains, as opposed to traditional bond interest being taxed as ordinary income. In fact, NTSX even has a lower tax cost than VTI!

It’s also cheaper to lever up bonds than stocks, and by using futures on a bond ladder, they’re not using daily-reset leverage usually seen with leveraged ETFs, so no volatility decay to worry about, and we're also largely avoiding counterparty risk, as bond futures markets are highly liquid. Even Bogleheads seem to like it for all these reasons.

All this comes at what I think is a low cost of only 0.20% for a packaged solution that novice investors would likely not be able to implement on their own. It's also been speculated that this is precisely the reason why the fund hasn't soared in popularity among portfolio managers. The theory is that ETFs that combine asset classes for you aren’t popular among advisors because they’re doing the work of the advisor. The aforementioned negative perception of the word “leverage” may also have something to do with it.

Those wanting a DIY version of this fund with ETFs can achieve roughly the same exposure with 90% VOO (S&P 500) and 10% TMF (3x long treasuries), rebalanced monthly, but it would be pretty tax-inefficient. You’d also still have an overall fee of roughly 0.13%, not to mention all the unwanted things like volatility decay, counterparty risk, greater borrowing costs, etc. A DIY version just doesn’t seem worth it in my opinion when NTSX itself is already sufficiently liquid, simple, elegant, relatively low-cost, and incredibly tax-efficient. You could also just buy treasury futures yourself, but that doesn't really seem worth the hassle either.

NTSX can be thought of as essentially a milder, cheaper version of the famous Hedgefundie Adventure.

NTSX vs. SWAN

NTSX is not unlike SWAN, though SWAN is designed more specifically for downside protection to hedge against black swan events, as the name suggests, aiming for 70/90 stocks/bonds exposure through options contracts on the stocks side. SWAN also commands a much larger fee and would be comparatively less tax-efficient than NTSX. Also keep in mind that WisdomTree's stated use case for NTSX is to use it to make room for other assets.

That said, these funds are pretty similar. In terms of exposure, NTSX is 1.5x 60/40 for effective 90/60, and SWAN is roughly 1.6x 44/56 for effective 70/90. Note that NTSX's treasury bond futures ladder has an effective average duration of about 7 years, while SWAN's treasury bond ladder aims to match the duration of the U.S. 10-Year Treasury Note.

NTSX Performance vs. the S&P 500 (SPY, VOO, etc.)

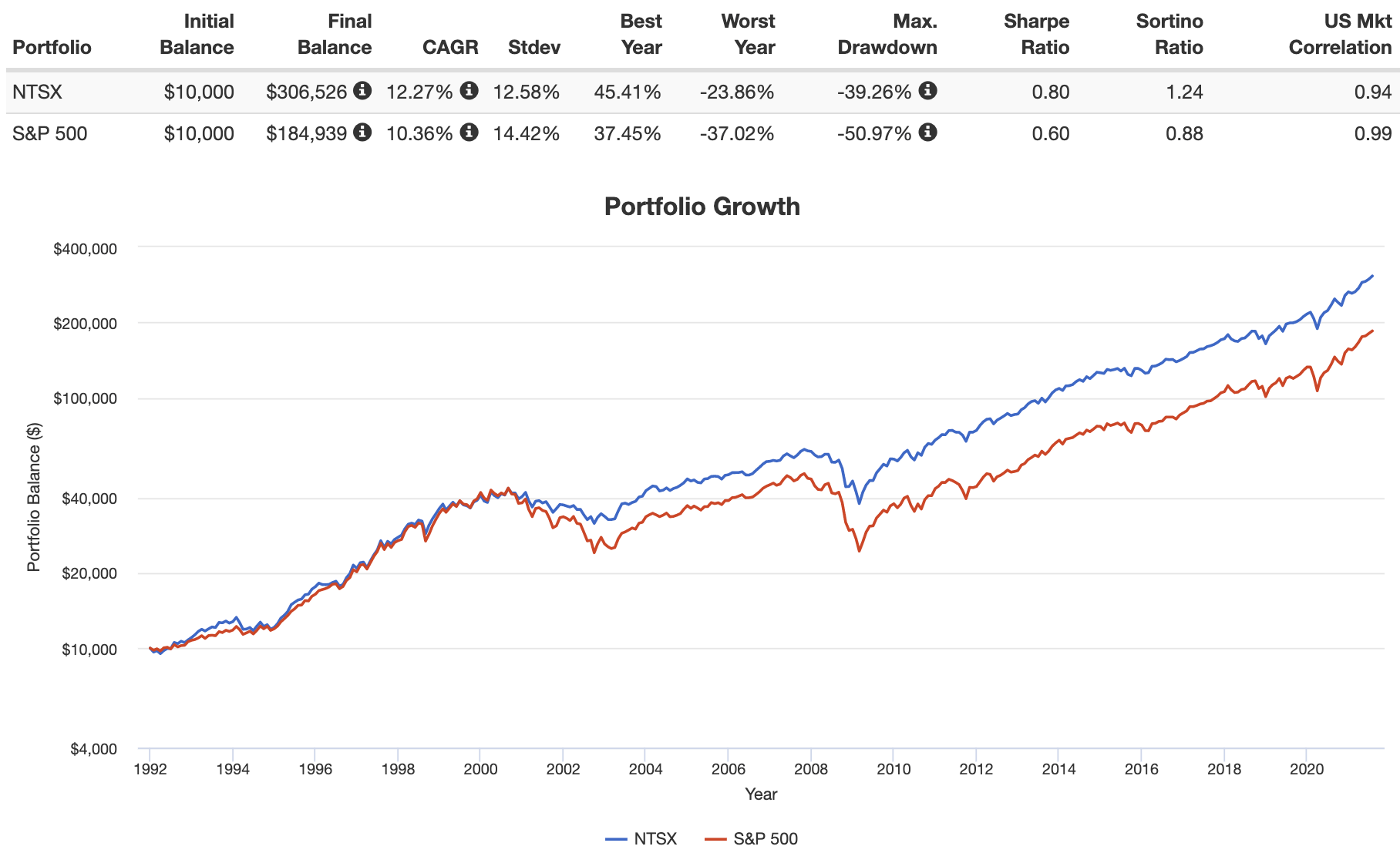

Remember, NTSX was designed to roughly deliver stock market returns but with lower risk. Conveniently, the bond bull market over the last 40 years or so has allowed a 90/60 portfolio to deliver above-market returns with lower risk. Here's an approximation of NTSX vs. the S&P 500 from 1991 through July, 2021:

Use Cases for NTSX

Interestingly, NTSX is suitable for different investors with different goals depending on how it's used. For a young investor in the accumulation phase, 100% NTSX wouldn’t be a bad idea. You’d basically be treating it like a less volatile S&P 500 fund. This use case is illustrated in the backtest above. This would again simply be a 90/60 portfolio in a single fund, though note that your equities exposure would be entirely U.S. large caps.

The primary use case suggested by WisdomTree themselves, on the other hand, suitable for older investors, even retirees, or anyone wanting more diversification, would be to use this fund at around 67% and diversify with that other 33% across other assets to further reduce the volatility and risk of the portfolio. The possibilities here are endless: international stocks, TIPS, factor tilts, gold, etc. Ideally, this would mean adding assets that aim to address a risk that both stocks and bonds suffer, such as TIPS for inflation risk. This could also mean simply adding assets that tend to be lowly correlated to both stocks and bonds, such as gold.

In this sense, NTSX basically provides a way to hold a traditional 60/40 portfolio – considered a near-perfect balance of risk and return – and still have room to diversify further. WisdomTree themselves state they aim to “boost the capital efficiency in the core to allow investors more flexibility” with these products.

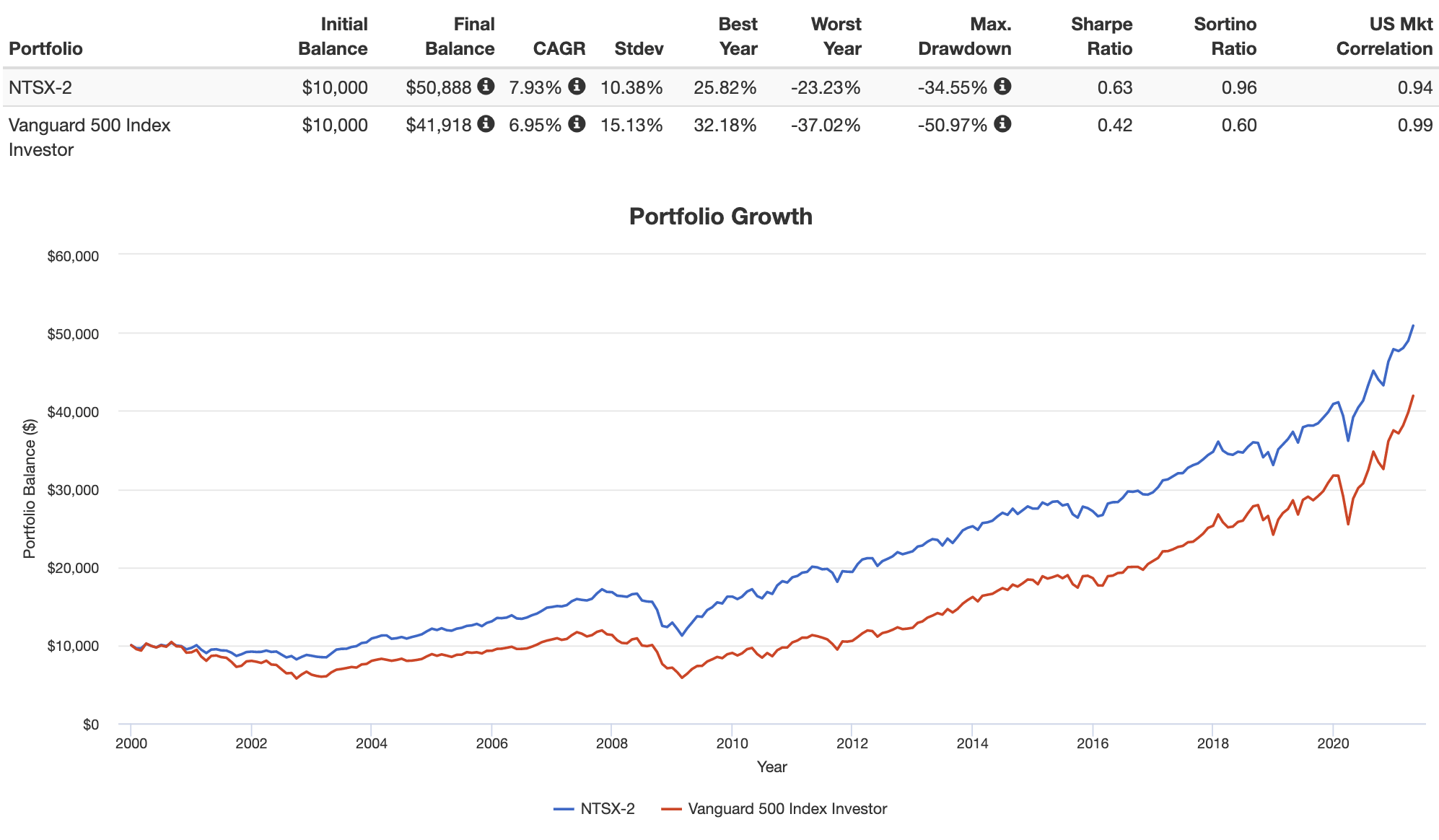

A reasonable portfolio for this diversification use case in my mind, if one’s desire is to reduce volatility and risk, would be something like this:

- 60% NTSX

- 10% Small Cap Value

- 10% Emerging Markets

- 5% Developed Markets

- 10% TIPS

- 5% Gold

Here's a backtest of this use case vs. the S&P 500 from 2000 through April, 2021:

This portfolio would provide effective exposure of 79/46/5 stocks/bonds/gold.

Here's a link for that pie for M1 Finance if you're interested. I wrote a comprehensive review of the M1 platform here if you're interested.

Canadians can find the above ETFs on Questrade or Interactive Brokers. Investors outside North America can use eToro or possibly Interactive Brokers.

Risks for NTSX

Originally, fundamental risks of liquidity and fund closure were concerns. I got into NTSX when its AUM was a little under $100M, with the cautious expectation that it may close within the year. Thankfully, AUM has now grown to around 6X that, approaching $600M. Again, it seems that it hasn't taken off with retail investors perhaps because it seems like a sophisticated product (with no marketing behind it), and it hasn't taken off with advisors/managers because it potentially puts them out of a job.

An obvious shortcoming of this fund – solved somewhat by the above proposed use case – is the lack of geographical diversification in equities. WisdomTree may have heard that complaint from investors; they recently filed for 2 new products like NTSX using Developed Markets and Emerging Markets. Whether or not those will materialize into viable ETFs is another story yet to be seen.

Update – May 20, 2021: Today, those two ETFs – NTSI and NTSE – launched for Developed Markets and Emerging Markets, respectively. I'm curious to see if they attract assets.

Update – August 9, 2021: A little less than 3 months later, NTSI and NTSE still have concerningly-low AUM of about $16 million and $2 million respectively. I'm hopeful they'll grow and stick around, but only time will tell. I still don't own them.

Update – January 3, 2022: NTSI and NTSE have attracted more assets and now have about $86M and $36M respectively. Industry rule of thumb says a “safe” minimum is $50M, after which fund closure becomes much less likely. So these two newer funds are now more attractive and viable in my opinion. I'm hoping the trend continues upward. I still don't own them at this time. Volume and spread still appear to be worse for NTSE, as we'd expect.

Update – February 18, 2022: Time flies. A year later, NTSI and NTSE have now attracted assets of about $217M and $50M respectively.

The downfall of NTSX would be what I would argue is a rare simultaneous combination of economic factors: rapidly rising interest rates, runaway inflation, and slow economic growth. But this scenario would also wreak havoc on virtually any diversified portfolio that holds mostly stocks and bonds. This concern can also be mitigated with an allocation to things like TIPS, international stocks, and gold, as I suggested above.

I actually think that’s why it’s also important to note that the effective duration of the bond allocation is intermediate (about 7 years), not long-term, posing less interest rate risk. This is why NTSX still outperformed the S&P 500 during periods where interest rates rose slowly. There also tends to be more roll yield to be captured in the middle of the yield curve.

Is NTSX a Good Investment?

So it NTSX a good investment? Maybe.

I think NTSX is an extremely interesting, useful, and clever product that can be inserted into different strategies, risk tolerances, and time horizons. The fund is incredibly tax-efficient, and it provides a packaged solution for retail investors who want the long-term returns of 100% stocks without the associated volatility and risk, all at what I consider to be a pretty low fee. The fund's risks are easily mitigated by diversifying across other assets and geographies, and its intermediate effective bond duration should bode well for future performance even in a rising rate environment.

What do you think of NTSX? Let me know in the comments.

Disclosures: I am long NTSX in my own portfolio. It comprises most of my taxable account. I know it sounds like I'm selling this fund pretty hard, but note that I am not affiliated with WisdomTree at all and I get no sort of kickback or compensation from them if you decide to buy NTSX (or any of the other funds listed here). I've also received no form of compensation from WisdomTree for the words I've written on this page. My discussion and appreciation of NTSX are simply the result of my own independent research and analysis.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. All examples above are hypothetical, do not reflect any specific investments, are for informational purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Don't want to do all this investing stuff yourself or feel overwhelmed? Check out my flat-fee-only fiduciary friends over at Advisor.com.

You mention youre long on NTSX with most of your taxable portfolio. Youve also got a guide on your ginger ale portfolio that isnt including any NTSX at all. Can you please explain what your strategy looks like?

Ive also been wondering if you could make a guide/review on combing NTSX/NTSI/NTSE in to a leveraged all world portfolio and if that makes any sense to try to stay diversified over all world while still having bonds and not compromising on returns.

Just replied to you on Reddit. Ginger Ale is my strategy. 90/10 VOO/EDV is close to NTSX. I’d love to own NTSI and NTSE but their AUM is currently too low for my tastes. I’m hoping they get more popular.

Can I get the link to the answer to the question for the Reddit post?

Here’s that exchange, Alex.

Re the idea to “stack” something on top of 60% NTSX, RPAR could fill that gap (tips, gold, global stocks, etc). 60/40 NTSX/RPAR looks alright. Or add some small cap as you suggest (IJR/IJS): 60/30/10 NTSX/RPAR/IJR

John, I tried to leave a comment on this page the other day but it hasn’t appeared, so I’m trying once again. (Apologies if you deliberately suppressed the comment b/c it was dumb or vexatious. If once again this comment doesn’t show, I’ll desist!) Basically, I’m wondering if you could elaborate — either here or in a separate blog post (yes, please!) — on how to think about overall asset allocation/diversification when one’s portfolio includes both leveraged and unleveraged assets. For instance, I understand as a logical matter how the summation of one’s asset allocation can exceed 100% (like if one were 100% in NTSX, making for a 90/60 portfolio), but I lack an intuition about what this means. Relatedly, I have trouble understanding how one might use NTSX in the context of overall portfolio construction. Suppose one wanted use NTSX in an 80/20 portfolio. If one acquired enough NTSX that its equity component accounted for 80% of the portfolio value and then plunked that in, the bond component would likely be overweight. Would one just not worry about that? Or would one acquire enough NTSX that its bond exposure accounted for 20% of the portfolio value, and then add in other equities to hit 80%? Is this the wrong way to think about it? Or if the answer is something like “it depends” — which seems likely — could you say a little about what it would depend on? Thanks for any thoughts on these matters!

Hey Ross, I replied to your other comment here last week.

Great article! Do you have any idea if it can be bought in EU especially in France? Some people told me that it is not possible…

Sorry Oliver, I’m not sure whether or not this would be available outside the U.S.

Hi

I am curious how you back tested ntsx when it started 3 years ago. How did you do that? I tried but could not.

Thank you

Rod

Hey Rod, I just used mutual funds and its target allocation of 90/60.

I enjoy your website. I have a decent size taxable account I found this strategy on YouTube. If I held a 90% position in NTSX vs SPY and used the other 10% to hedge via the strategy below, in your opinion good idea or bad idea? Alternatives? I through 5% UVXY and 95% in Portfolio Visualizer and the max dd looked pretty good vs NTSX alone. Thanks.

How to Hedge & Protect Your Investment Portfolio during Market Crash with One Simple ETF? – YouTube

Long Volatility Hedging Strategy

Step 1

When 15 < VIX < 20, add 5% VXX Position

When VIX < 15, add another 5% VXX Position

Step 2

Rebalance VXX position during the Bull Run. Make sure the VXX position stays 10% of the entire portfolio

Step 3

When the market has Corrections or Crashes, sell the VXX position and buy back the Equities:

When VIX breaks 40, sell 5% of the VXX position and buy your equity choice

When VIX breaks 60, sell 5% of the VXX position and buy your equity choice

I can’t provide personalized advice and I don’t try to time the market. VIX futures seem like an insurance policy that’s not worth the premium to me. I’m a long term buy-and-holder.

Thanks for the response. I have a second question. I would like to duplicate your results via Portfolio Visualizer.

I weighted 90% VFINX, 60% VBIIX and -50 CASHX. My worst year shows -31%. Yours shows 23%. Can you tell me the mutual funds you used to perform your test?

VBIIX is not solely treasury bonds. I believe I used VFITX or PRTIX. I may have used the actual allocations corresponding to NTSX’s treasury futures ladder for long, interm., and short. Honestly don’t remember at this point. Maybe I’ll revisit.

My concern is the 60/40 portfolio looks good historically when bonds have been cheap. I’m worried that now that bonds are outrageously expensive with low interest rate, you could see them actually be drag on the portfolio and what happens if there is inflation and the bond portion takes a dump.

Definitely a possibility, but keep in mind lower future expected returns for bonds does not mean they won’t still do their job of curbing stock downturns, as I explained here.

Great article! I’m considering using NTSX. However, I just watched Ben Felix’s video on the S&P 500, and it got me concerned about the fact NTSX is only exposed to large cap equities. You’ve mentioned that your taxable account is 100% NTSX – what percentage is that account of your total investment portfolio, and are you concerned about the lack of diversification across cap sizes / value / growth?

Considering to make a taxable account with 50% NTSX, 16% AVUV, 10% AVDE & AVEM, 8% AVDV & DGS. Thoughts?

Definitely good to throw in some small cap value in my opinion; I overweight that segment heavily, as I explained here.

Hi John,

Enjoyed the write up and this fund makes a lot of sense. Was wondering what would be a good tax loss harvesting partner to pair with NTSX?

Nothing that I know of. SWAN is probably the closest thing. Or just hold the international one NTSI for 30 days.

John, how do you suggest I account for NTSX when viewing my asset allocation as a whole? In other words, presumably in a tool like Morningstar X-Ray or Fidelity Full View, NTSX in a portfolio would be calculated as 60/40 stocks to bonds. But is that the appropriate way to consider its impact on your portfolio as a whole? I am interested in adding NTSX, but as a practical matter I have many other holdings that I prefer not to sell due to capital gains. So I’m looking for guidance as to how to decide how much NTSX to add while maintaining a desired effective asset allocation between stocks and fixed income. Thanks.

Hey David, I prefer to just include its 90/60 exposure in the normal calculation, e.g. if NTSX is 67% of the portfolio (for 60/40 exposure, which is WisdomTree’s suggested use case) and I buy stocks with the other 33%, my asset allocation is 93/40.

Others may prefer to view it more simply as just a less risky equities position, so in my example they’d just say they’re 100% stocks, but this way doesn’t make much sense to me unless the portfolio is 100% NTSX, as 60% exposure to intermediate treasuries is no slouch, and this may lead this investor to incidentally overweight bonds.

Hope this helps!

John, I hope I can reply to your answer here, even though I’m not David (the author of the August 16, 2021 comment). I’m doing this because I had a question similar to — probably simpler than — David’s, and I’m still a bit confused. Basically, can you give a quick mini-tutorial on how to think about asset allocation when the use of leverage means that the sum of the components can exceed 100%? I realize that may be a stunningly “n00b” question but I’m having trouble getting my head around it. For instance, say Bob has chosen an AA of 85 S&P500 and 15 bonds, and a $100K portfolio. And suppose he wants to use NTSX. It seems to me that to get his desired $85K equity exposure, he’d need to buy ($85K/0.9)=~$94,444 of NTSX (since each dollar of NTSX more-or-less exposes him to $0.90 of the S&P500). Is that right? And if he makes that purchase, then he has ~$56,667 in bond exposure (since each dollar of NTSX more-or-less exposes him to ($0.10*6) of bonds). Right? But then it seems he has ~3.8x ($56K/$15K) the bond exposure that his AA calls for. Is that right? If so, why isn’t that a problem? Finally, if he pursues this strategy, then he has ~5,555 left over. Suppose he plunks it into a gold ETF. Then his AA is 85% equity / 56% bond / 5.5% gold. I just have some mental block that prevents me from conceptualizing this AA when its components exceed 100%. Can you shed any light on this, or point me in the direction of something that will do so? Thanks very much and sorry for the length of this comment.

Not a dumb question at all, Ross. It can seem weird at first to add up allocations that equal greater than 100%.

Yes, your line of thinking is correct if I’m following it right. You might be overthinking it. In simple terms, NTSX is just a way to apply leverage to the portfolio – borrowing to increase exposure. Specifically, with 100% NTSX, we get 150% or 1.5x exposure to the classic 60/40 portfolio.

In your example, the investor just has leveraged exposure to bonds. This may end up being good or bad. So it’s hard to say whether or not it’s a “problem.” Suppose Rob is using plain 90/10 but Bob is using 90/60 via NTSX. If interest rates rise rapidly and unexpectedly, we’d expect that to hurt treasury bonds, so Bob’s portfolio will perform worse than Rob’s, as Bob has 60% bonds but Rob only has 10%, so this scenario hurts Bob’s portfolio more. Suppose the stock market crashes. We’d expect treasury bonds to rise. So Bob with 90/60 will see greater gains than Rob with 90/10, as Bob has more exposure to treasury bonds.

Here’s an even simpler example using one asset, stocks. SSO is a leveraged fund that is 2x or 200% the S&P 500. So if I have $10 in SSO, I have $20 of exposure. If the S&P 500 goes up by 10%, my position should go up by 20%. If it falls by 10%, my position should fall by 20%. So leverage can be a double edged sword; it magnifies both gains and losses. Obviously it gets a bit more nuanced with multiple assets like with NTSX.

You may find this post or this post useful in thinking about leverage.

Hope this helps.

Hi John, I highly appreciate your insight, it turned out immensely helpful for me.

I am trying to repark my kids college fund combined with Tier 2 emergency fund (tier 1 is sitting on a checking account) which is pretty much lump sum ( around 100k) in which connection I would love to hear your opinion.

The money now is sitting in 0.4% yield saving account, earning nothing and melting because of inflation which is unpleasantly bothering me.

I am considering to put them in NTSX for the next 3-4 years mostly for digging around 20k each year from that.

Would you think that would be a decent option for short term investment? I would love to have an option to beat inflation at least

Thanks for your reply

Hey Ellen, glad you’ve found my ramblings helpful! I can’t provide personalized advice, but if it were me, I’d go much more conservative than NTSX. I designed a portfolio here to replace an emergency fund that sounds like exactly what you’re looking for. If I were to go even more conservative, it would be something like 50/50 short treasuries and short TIPS (inflation-linked bonds).

Even simpler than that would be the 1% APY with M1 Finance’s checking account, but to get that it’s a $125 annual fee, so on $100k that would be $875 earned.

Hi John,

Love the site. I’ve been recommending to friends that are in to personal finance.

What do you think about leveraging up on NTSX through cheap margin in taxable? Adding 2x through margin would put it at 180/120 (3x a 60/40), a little more equity tilt than the 165/135 in HFEA. NTSX does quarterly rebalancing and on 5% deviation.

Thanks, Claire! Not a bad idea; I’d pick a leverage ratio you feel comfortable with and dial it in with the margin, rather than simply maxing it out. Also depends heavily on how cheap that margin is. In many cases you’d still come out ahead just using the LETFs.

Regarding a taxable account (because my Roth is already fully contributed):

NTSX currently shows 0.34% tax cost. What do you think about simulating HFEA using UBT instead of TMF to get better returns and lower taxes?

UBT is 0.00% tax cost. UPRO is already only 0.02%. Since it’s only 2x leveraged, do something around 35% UPRO / 65% UBT. Seems like this “taxable” HFEA is 105 / 130 while NTSX is 90 / 60.

Thank you as always; that’s my question of the day.

Tax implications of LETFs are definitely nowhere near zero, which is why they’re deemed inappropriate for a taxable environment. The need for rebalancing is just as much of a concern. Moreover, UBT’s low AUM is somewhat concerning.

Is there such a thing as leveraged TIPS? Would be interesting if it could be added to a 3X/2X AWP..

Nope, no leveraged TIPS. Long term via LTPZ is your best bet.

OK I get that you used 90% VFINX 60% VFITX and -50% CASH.

I have added that to one of your PV calculations and the link to the modified PV page is here.

https://tinyurl.com/yzazydvy

The MaxDD for that is the horrible 40%. Does not sound like a balanced fund.

I mean, yea, it’s 1.5x leverage on 60/40. What did you expect to see for the ’08 crisis? PV also uses the max DD for the entire stress period, not a single day.

Try 14.5% QLD 12.5% URE 23% UBT 14.5% QQQ 12.5% RFI 23% WHOSX

Has 50% leverage just like NTSX, similar volatility, but much lower drawdown (you will have to use synthetic QLD etc.) of about 31%.

You can lower the leverage to reduce the drawdown further. The CAGR will also be reduced but can still be better than the synthetic NTSX in the long run depending on the leverage. For example 25% leverage reduces the maxDD to 26%.

For 2019-2021 (the actual period for which the real NTSX data is available) 25% leverage gives 13.5% volatility, 7.6% maxDD and 27.2% CAGR, vs. 15.2% volatility, 14.6% maxDD and 27.13% CAGR. Not bad.

I determined these weights by averaging the weights for monthly rebalanced QQQ, RFI and WHOSX using risk parity for 2000-2021.

This is entirely different from NTSX.

Hi John,

This is a really interesting and engaging website, thanks for the great work! I’m a young investor with about 5 years of market gains mostly split between VOO and VT at this point, planning to adjust my tax-protected holdings to diversify across risk factors as you’ve mentioned in other posts. I’ve been digging into NTSX more and am thinking of switching my taxable holdings to NTSX. What are your thoughts on selling current holdings and having to incur capital gains to switch to NTSX, vs just contributing future investments to NTSX to avoid the current capital gains hit? I’d obviously have to deal with paying capital gains down the line if I don’t now, so maybe capital gains are a wash in the long run.

Thanks,

Steve

Thanks Steve! Depends on how big of a tax hit it would be and whether or not you want to incur it now or later. I’d probably just put new deposits toward the new fund, and if we experience a crash in the future, sell shares of the old holdings to harvest losses.

Would including Small cap value and Emerging markets be advisable for shorter and intermediate savings goals? I’d like to pair NTSX with something in the taxable environment but not sure what

Sure. Greater diversification and lower leverage.

Hi John,

Thanks for this great website and your continuous updates.

I would like to create a portfolio similar to “NTSX-2” and include NTSI and NTSE for international and EM stocks exposure. NTSI and NTSE have about 40% US exposure.

What allocation would be ideal and approximate NTSX-2?

Thanks,

Simon

Hey Simon, NTSI and NTSE only have U.S. exposure because they use U.S. treasury bond futures. The stocks aren’t exposed to the U.S.; they’re Developed Markets and Emerging Markets, respectively.

Hi John,

Thanks for the prompt reply. I looked at your Ginger Ale Portfolio and thought about modifying the 100% stocks version, i.e., by using the WisdomTree ETFs to include bonds:

– 50% NTSX

– 30% NTSI

– 15% NTSE

– 5% SCHP

What do you think?

Kind regards,

Simon

I can’t provide personalized advice, but just note that this is nothing like the Ginger Ale Portfolio.

Curious to hear what you think of the International (NTSI) and Emerging Markets (NTSE) funds that Wisdom Tree just launched today (along with renaming NTSX as the WisdomTree U.S. Efficient Core Fund). Seems like a good way to add some international exposure to the portfolio for those using NTSX.

Indeed. Will be curious to see if they attract assets. I have to assume they’d be less popular than NTSX.

Does tying NTSI and NTSE to US treasuries give you pause?

Or is it still a reasonable approach despite the funds not having US stocks?

Not at all.

Perfectly reasonable and desirable.

My taxable/brokerage is currently 100% vtsax. Wouldnt moving 100% to ntsx potentially be bad if you already have a sizable amount in the taxable/brokerage (1/3rd of retirement) due to capital gains tax incurred on the move?

Just comes down to whether or not you want to pay those taxes now by locking in gains.

Hi John,

I’m really interested in your proposed use case with 60% NTSX, 10% Small Cap Value, 10% Emerging Markets, 5% Developed Markets, 10% TIPS, 5% Gold (though I’d probably substitute the gold with something else) for my taxable account which I’m using to saving up for an intermediate-term goal. I’m curious if you back-tested that portfolio yet and if you saw improved results relative to risk. What about the more simple 90/10 split with AVUV as you suggested in the comments above?

As always I love your content and you have found a new dedicated reader in me! Keep up the good work!

— Davis

Thanks for the kind words, Davis!

Agreed, gold wouldn’t be ideal for taxable since it’s taxed as a collectible.

Here’s a backtest comparing those options.

Is the CASHX in negative %’s being added to the back test portfolios a leverage correction? Can you explain a little or express in terms of leverage?

Thanks for this (and other) informative write-ups! I’m getting much inspiration from it.

Question about NTSX in taxable: Traditional recommendation seems to be to hold bonds in tax advantaged. Do the same considerations apply to the bond portion of NTSX (yields taxes at income tax rates)? And how does leverage affect taxes? Thanks!

Thanks for the kind words, Johannes! Glad you’re finding them useful!

The futures NTSX uses for the bonds side are actually more tax-efficient than bonds or bond funds themselves. WisdomTree put some thought into building NTSX for tax-efficiency. You can read more about it here:

https://www.wisdomtree.com/blog/2018-08-02/introducing-the-wisdomtree-90-60-us-balanced-fund-ntsx

https://www.wisdomtree.com/-/media/us-media-files/documents/resource-library/wisdomtree_ntsx_faq.pdf

Thanks! Just summarizing my findings here – bond futures (which are held by this fund) are taxed at 60% short-term and 40% long-term capital gains; vs bond yields (from holding bonds directly) are taxed at full income tax rates (which are typically higher than long term capital gains). Per the WisdomTree prospectus, because of this the futures strategy tends to be more tax efficient than plain bonds in flat or rising bond yield rate environments, but actually less tax efficient in falling yield environments (because with the futures, one ends up paying 60% short-term + 40% long-term capital gains tax on the resulting bond appreciation right away, which dominates the returns and taxes from yield in this environment).

Also, given that 90% of the fund consist of presumably tax-efficient large-cap stocks, I can see why it’s a good tax-efficient strategy more often than not.

IYO, how well are the bonds in NTSX suited for the expected increases in the 10-year during the rest of 2021? The increases in early 2021 seem to have really taken it off course of the S&P.

As a long term investor, I’m unconcerned with a fund’s 1-year behavior, much less its behavior over a few months. NTSX is not supposed to track the S&P 500. I talked about how to view one’s bond holding here. Effective duration of NTSX’s treasury futures ladder is about 7 years.

Thanks. That was a lazy question on my part, so sorry about that. My taxable is generally short-term minded, which doesn’t line up the same as yours.

I am young investor and I just took your advice on M1 Finance on investing 100% NTSX into my taxable account. I noticed your language across comments you’ve left and articles you’ve written and it sounds like you aren’t 100% in NTSX in your taxable account. What else does your taxable portfolio include and why?

Thank you very much for your time – Zaija

My taxable account is 100% NTSX.

If I may ask John, why do you not diversify the US only NTSX with any international funds? I’d love to understand your thought process around this.

Thanks!

As I noted, NTSI and NTSE have very low AUM.

Hi John,

Is it possible to somewhat approximate this with 80% Voo, 10% TYD and 10% TMF, or will volatility decay affect the expected returns too much ? Or better yet, replace Voo with DFAU or AVUS?

Thanks,

Matthew

Closest approximation would be 90/10 VOO/TMF but I’m not sure why you’d want to. It would be much less tax-efficient than NTSX and yes, the volatility decay would likely wipe out the small savings on fees.

Instead of going that route and using DFAU or AVUS, I’d think something like 90/10 NTSX/AVUV would be superior, or 80/10/10 NTSX/AVUV/AVDV if you want to incorporate ex-US SCV.