SGOV is a relatively new ETF from iShares for 0-3 month U.S. Treasury bonds, called T-bills. But is it a good investment for 2026? I review it here.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

SGOV ETF Review Video

Prefer video? Watch it here:

SGOV ETF Quick Stats Table

Before we get into the details, here's a table of the quick stats for SGOV:

| Full Name | iShares 0-3 Month Treasury Bond ETF |

| Issuer | BlackRock / iShares |

| Ticker | SGOV |

| Inception Date | May 26, 2020 |

| Exchange | NYSE |

| Index Tracked | ICE 0-3 Month US Treasury Securities Index |

| Expense Ratio | 0.09% |

| AUM | $84 billion |

| SEC Yield (Apr 2026) | 3.55% |

| Effective Duration | 0.10 years |

| Distribution Frequency | Monthly |

SGOV ETF Methodology

SGOV is the iShares 0-3 Month Treasury Bond ETF. It launched in mid-2020 and has since quickly amassed nearly $85 billion in assets, making it one of the most popular ETFs for Treasury Bills. SGOV took in nearly $1 billion in its first 5 months.

SGOV is a pretty simple fund. It just tracks an index that holds ultra short term U.S. Treasury bonds – called T Bills – that mature in 3 months or less. That index is the ICE 0-3 Month US Treasury Securities Index, which is rebalanced monthly.

Because T-bills are the safest bonds out there, we call them a “cash equivalent” and the 3-month T-bill rate is used as what we call the “risk-free rate” when comparing other assets. As such, many investors use T-bill funds like SGOV for their emergency fund because it tends to pay more than a traditional savings account at a bank.

The phrase “cash equivalent,” may make you think negligible returns, but T-bills have returned 3.32% annualized historically going back to 1926 for the U.S.

Inflows into T-bill funds like SGOV have soared in recent months to capture their currently-very-attractive yield and to take up a safe haven in short-term U.S. government debt issues. At the time of writing in January 2023, the 3 month T Bill rate is 4.57%, and 5% is not out of the question by the end of the year. Even the past 30 days or so going into 2023 have seen record inflows – nearly $10 billion in the first trading week of the year – into short-term government bond funds after fearful investors are fleeing stocks en masse.

Update 7/21/23: SGOV now has an SEC yield of 5.21% as of July 21, 2023.

Update 7/19/24: SGOV's fee waiver expired this month so it now costs 0.09%. It has an SEC yield of 5.25%.

Update 10/20/25: Vanguard finally launched an ETF for T-bills, VBIL, which is slightly cheaper than SGOV now at 0.07%. I specifically compared it to SGOV here.

How Does SGOV Work?

So let's look specifically at how SGOV works.

The fund holds roughly 93% of its assets in direct U.S. Treasury bills spread across the 0-to-120-day maturity spectrum. The underlying ICE index covers every publicly issued T-bill with 3 months or less remaining and at least $1 billion outstanding, excludes Fed SOMA holdings, and rebalances on the last calendar day of each month. The index holds roughly 40 component bills.

As bills mature, the fund continuously rolls proceeds into newly issued or outstanding bills via “representative sampling.” Portfolio turnover is reported as effectively 0% (maturities don't count as sales under accounting rules), but in economic terms, the fund is in perpetual motion. This is why SGOV provides no rate lock; today's yield is a snapshot of wherever short-term T-bill rates happen to be right now. If the Fed cuts next month, your monthly distributions will drift lower as bills roll.

It's worth explicitly noting that T-bills themselves don't pay interest like most bonds. They are simply sold at a discount to their face value, and the difference is the effective “interest.” However, since SGOV as a fund is rolling these bills, the fund does pay out that effective “interest” in the form of a monthly dividend. So in short, T-bills don't pay dividends but SGOV does.

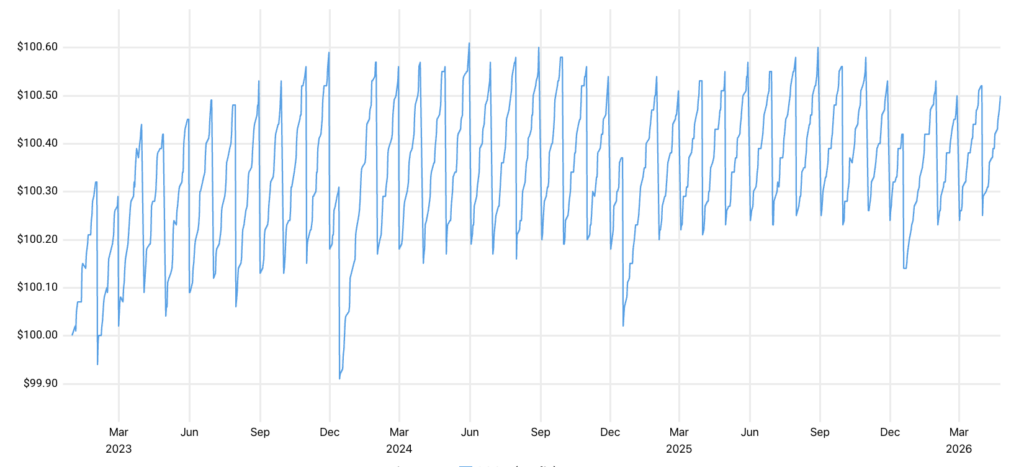

Sometimes investors are confused by the “sawtooth” motion of SGOV's price behavior, so the mechanics are worth understanding.

SGOV's share price doesn't hover at a fixed price. It climbs steadily over the course of a month as interest accrues into the NAV, and then drops on the ex-dividend date (typically the first business day of each month) when the accumulated distribution is paid out. This is completely normal and by design. This is different from a money market fund, which maintains a stable $1.00 NAV and accrues dividends as a separate calculation.

Another common misunderstanding resulting from that is that it's advantageous to buy the fund at a certain time during the month. This is not true, as you'll receive any interest for the remaining part of the month after you buy.

SGOV ETF Performance

Since inception in 2020 and looking through March 2026, SGOV has returned 2.93% annualized with volatility of 0.24%:

SGOV Dividend Yield and History

At the time of writing in April 2026, SGOV has a dividend yield of 3.55%. (This is quoted as a 30-day SEC yield, meaning the yield net of fees for the last 30 days, annualized. Think of this like the APY quoted for a savings account.)

But it hasn't always been that high. Let's briefly look at its history to better understand how SGOV's yield changes with the federal funds rate.

SGOV launched into a zero-interest-rate world in 2020 and spent its first 18 months paying essentially nothing. The Fed's rate hiking campaign in 2022 transformed the fund extremely quickly. Monthly distributions climbed from $0.0018 in February 2022 to $0.324 by December 2022, and the 30-day SEC yield breached 4%.

2023 and 2024 were even juicier for SGOV. SEC yields of 5.25% were seen around February 2024. Then the Fed cut 100 bps in late 2024 and made another cut a year later in 2025, arriving at roughly 3.5% for mid-2026.

SGOV's annual NAV returns tell the arc neatly:

| Year | SGOV Annual Return |

|---|---|

| 2021 | 0.02% |

| 2022 | 1.58% |

| 2023 | 5.13% |

| 2024 | 5.28% |

| 2025 | 4.24% |

To state the obvious, SGOV quickly reflects rate changes due to its inherently short-term nature, for better or worse.

SGOV Dividend History

Here's the specific dividend history of SGOV overlaid with the Federal Funds Rate since the fund's inception in mid-2020 through mid-2026:

SGOV Dividend History

Monthly distribution per share vs. Fed Funds Rate — Jul 2020 to present

December distributions reflect the sum of two monthly payments (SGOV typically pays twice in December). January distributions are $0 in most years as a result of this timing. 2021 monthly distributions were sub-penny and display as $0.00 on most data sources. Hover bars for details. Source: iShares / SlickCharts.

SGOV Expense Ratio History

Let's also talk about the history and changes with SGOV's expense ratio, because this seems to confuse people too.

At launch in May 2020, iShares set a gross management fee of 0.12% with a partial but hefty waiver, producing a net expense ratio of just 0.03%. This was aggressively priced to dominate the ultra-short Treasury ETF category during the COVID-era cash surge (and it did so swimmingly). The waiver was extended annually, eventually settling at 0.05% net through mid-2022 and 0.07% net through mid-2024.

Then in July 2024, the waiver expired and was not renewed. iShares simultaneously cut the gross fee from 0.13% to 0.09%, landing at the current 0.09% gross = 0.09% net. The practical result for shareholders is that SGOV is slightly more expensive than before, but still among the cheapest T-bill ETFs in existence.

From my interactions with people online, clearly many do not realize that this fee waiver expired or that SGOV's net expense ratio has crept up over the years since its inception.

In the interest of full disclosure, that expiration also conveniently opened a window for competitors like Vanguard, who launched VBIL at 0.07% in early 2025. Now there are a handful of T-bills ETFs that are cheaper than SGOV, including VBIL, XHLF, TBLL, and more.

SGOV Risks

We call SGOV “risk-free” colloquially, but that admittedly doesn't tell the full story with respect to specific risks, so I'll briefly cover those now in the interest of being comprehensive here.

Credit risk: effectively zero. Treasury Bills are direct U.S. Treasury obligations backed by the full faith and credit of the federal government. The ETF wrapper adds operational risks (trust structure, BlackRock sponsor, State Street custodian) that are theoretical but vanishingly small in practice. SGOV is not FDIC-insured, but in any scenario where Treasuries default, nearly every USD-denominated asset would be impaired simultaneously, so this is less a risk specific to SGOV than a risk specific to civilization as we know it.

Interest rate risk: trivial. With effective duration around 0.10 years, a 100-bp rate shock moves NAV roughly 8-11 cents on a $100 share. During the most aggressive hiking cycle in 40 years (2022), SGOV's NAV never deviated meaningfully from par plus accrued interest. Maximum historical drawdown since inception is under 0.10%. For practical purposes, you're not going to lose money in SGOV due to rates.

Reinvestment risk: the dominant concern right now. Remember, every few weeks, bills mature and reinvest at prevailing rates. If you want to lock in today's rates for a defined period more than 1 month, SGOV is not the tool.

Inflation risk: the quiet drag. We'd expect SGOV to roughly match CPI over the long term, but that's precisely why it's a short term investment vehicle – we want assets to appreciably exceed inflation to fund future consumption. SGOV is a cash management tool, not a wealth accumulation vehicle.

Liquidity risk: essentially none. Roughly 18 million shares trade daily (~$1.9B notional), bid-ask spreads of one penny. The underlying T-bill market is the deepest securities market in the world. The only “liquidity friction” is T+1 settlement plus however long your broker takes to ACH funds to your bank, typically 2-4 business days total.

Depending on your specific investment strategy, I'd guess these risks are likely immaterial, but I figured they're worth explaining for those who may not fully understand them.

SGOV Tax Treatment

Now let's briefly cover the tax treatment of SGOV.

Federal taxes – SGOV distributions appear in Box 1a of your Form 1099-DIV as ordinary dividends, taxed at your marginal income rate. There are no qualified dividends (Box 1b should be $0).

State taxes: where SGOV earns its edge. Interest on direct U.S. Treasury obligations is exempt from state and local income tax.

What this means in practice, for example, is a California investor in the 9.3% state bracket receiving 4% from SGOV effectively earns an extra 0.35% in after-tax yield versus a fully-taxable savings account or money market fund paying the same rate. In New York City, with combined state + city rates near 12.7%, the advantage is even larger. In Florida or Texas (no income tax), this doesn't help you at all – in which case a top-tier high-yield savings account may have the edge on pure pre-tax yield.

The comparison to a savings account hinges heavily on that tax dimension, so I made a calculator in the next section to easily compare.

SGOV vs. Savings Account – After-Tax Yield Calculator

For a small difference in yield, state taxes may be the deciding factor in considering SGOV versus a savings account. Here's a calculator to compare after-tax yield.

HYSA means “high yield savings account.” Input your tax rates and yields.

SGOV After-Tax Yield Calculator

See whether SGOV or your savings account actually pays more after taxes.

Assumes SGOV distributions are ~97.5% exempt from state income tax per iShares U.S. Government Source Income information. Federal, state, and NIIT rates applied to ordinary income only. Does not account for AMT, deduction phase-outs, or state-specific rules (e.g. CA requires >50% quarterly Treasury threshold, which SGOV meets). Not tax advice – consult a professional for your situation.

SGOV as an Emergency Fund

SGOV is a strong emergency fund vehicle for brokerage investors, especially in high-tax states: Treasury safety, low cost, liquid, state-tax-free, and often better yield than high yield savings accounts and money market funds after tax, and seamlessly integrated with the accounts where your other investments live.

Just remember settlement of funds is going to be a couple days, so envision 3 days or so before funds hit your checking account or wherever you're transferring to.

The practical Boglehead consensus seems to be a mix of a plain HYSA or checking account for genuine instant liquidity and then 2-5 months' expenses in SGOV for yield and tax efficiency. This captures the best of both worlds without sacrificing access speed.

Remember SGOV is also only accessible during market hours (9:30 AM – 4:00 PM ET) since it's a tradable security, not an account.

Is SGOV a Good Investment?

So is SGOV a good investment? Sure, if you want T-bills and don't want to bother with buying and rolling a ladder of individual bonds yourself.

SGOV is clearly a great low-cost index fund for T-bills, evidenced by its huge AUM and massive inflows, and it's one of the most affordable in its space. SGOV works great as a safe temporary parking garage for cash or an emergency fund that pays more than a traditional savings account.

SGOV does exactly what it advertises – it delivers T-bill rates with minimal fees and maximum convenience. It handily beats the FDIC national average savings interest rate (~0.40%). For someone who would otherwise leave cash sitting in a bank account earning nothing, SGOV is an obvious upgrade.

What SGOV is good for:

- Emergency funds in taxable accounts, particularly for investors in high-tax states.

- Parking cash awaiting deployment while you decide what to do with it.

- Short-term liabilities – tax payments, tuition, down payments within 12 months.

- Zero-duration ballast in a bond portfolio.

- Flight-to-safety trades during equity market volatility.

What SGOV is not good for:

- Long-term wealth compounding – inflation will slowly eat your real returns.

- Bond allocations in IRAs with 20+ year horizons, where longer durations have historically dominated over full cycles.

- Situations requiring instant liquidity – T+1 settlement plus ACH transfer means 2-4 business days to cash, not seconds.

- Rate-lock strategies – if you want today's yield guaranteed for 12 months, buy a bond instead.

Conveniently, SGOV should be available at any major broker, including M1 Finance, which is the one I'm usually suggesting around here.

What do you think of SGOV? How does it fit in your investment strategy? Do you own it? Let me know in the comments.

SGOV FAQ's

Is SGOV safe?

SGOV is nearly as safe as it gets in terms of investable securities. We're talking about treasury bills from the U.S. government maturing in 3 months or less. The fund has never experienced a meaningful NAV loss. It is not FDIC-insured, but credit risk is functionally equivalent to holding T-bills directly. The main risks are reinvestment risk (yields fall as the Fed cuts) and inflation risk (your real return may be modest). You're not going to lose money in SGOV in any normal scenario.

Does SGOV pay dividends?

Yes, SGOV pays dividends monthly. The ex-dividend date is typically the first business day of each month, and payment follows within a few days.

Is SGOV good for an emergency fund?

Yes, with the asterisk that you may want to keep 1 month of bare expenses in a plain vanilla HYSA or checking account for genuine instant liquidity. SGOV requires T+1 settlement plus ACH transfer time (typically 2-4 business days total) before cash reaches your bank. The yield advantage over most savings accounts – especially after state taxes in high-tax states – is real and meaningful, but that liquidity gap is arguably worth noting.

Is SGOV exempt from state taxes?

Yes, SGOV's dividends are exempt from state taxes but are still taxed federally as income.

Is SGOV FDIC insured?

No, SGOV is not FDIC insured. FDIC insurance covers savings accounts. SGOV is a tradable security in the form of an Exchange-Traded Fund (ETF) that holds U.S. T-bills. However, SIPC insurance protects investors' securities at SIPC-member brokerage firms – up to $500,000 – in the event the brokerage fails financially.

Disclosure: None.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Hi John,

Just a heads up that it looks like the fee waiver was extended until June 30, 2024. Though they are waiving fewer basis points, not that it really matters right now. The new expense ratio is 0.07%

What are the chances the fee waiver doesn’t get renewed for 2023? Does the actual expense ratio change the calculation?

What about the new kid:

https://www.ustreasuryetf.com/etf/tbil/

Unlikely, but possible I suppose. Even without the waiver, SGOV would still be cheaper than TBIL.

The Public investing app just started a T-bills account advertising a 5.1% yield, but has a .60% annualized fee. It uses 26-week T-bills. Looks like SGOV might be one of the best alternatives for avoiding that higher fee?