TQQQ has grown in popularity after a decade-long raging bull market for large cap growth stocks and specifically Big Tech. But is it a good investment for a long term hold strategy? Let’s dive in.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

[toc]

Video – TQQQ ETF Strategy Review

Prefer video? Watch it here:

What Is TQQQ?

TQQQ is a 3x leveraged ETF from ProShares that aims to deliver 3x the daily returns of the NASDAQ 100 Index.

Explaining how a leveraged ETF works is beyond the scope of this post, but I delved into that a bit here. Basically, these funds provide enhanced exposure without additional capital by using debt and swaps. This greater exposure usually comes at a pretty hefty cost, in this case an expense ratio of 0.95% at the time of writing. The “normal” 1x fund QQQ has an expense ratio of about 1/5 that at 0.20%.

These funds are typically used by day traders, but recently there seems to be more interest in holding them over the long term. TQQQ has become extremely popular in recent years due to the bull run from large cap tech, which comprises a huge percentage of the fund. There’s even an entire community on Reddit dedicated to this single fund.

But What About Volatility Decay for TQQQ?

The daily resetting of leveraged ETFs means the fund only provides the return multiple relative to the underlying index on a daily basis, not necessarily over the long term. Because of this, volatility of the index can eat away at gains; this is known as volatility decay or beta slippage.

Unfortunately, the financial blogosphere took the scary-sounding “volatility decay” and ran with it to erroneously conclude that holding a leveraged ETF for more than a day is a cardinal sin, ignoring the simple underlying math that actually helps on the way up. In short, volatility decay is not as big of a deal as it’s made out to be, and we would expect the enhanced returns to overcome any volatility drag and fees.

That said, note that leveraged ETFs typically carry hefty fees. TQQQ has an expense ratio of 0.95%.

Drawdowns Are Important

I’m not one to parrot the “leveraged ETFs can be wiped out” idea (thanks to modern circuit breakers, meaning mechanically TQQQ can’t go to zero because trading would be halted before the underlying is able to drop by 33.4% in a single day), but if QQQ drops by 5%, TQQQ drops by 15%. People tend to focus on volatility decay and forget that major drawdowns are actually the bigger concern here. This is because simple math again tells us that it requires great gains to recover from great losses:

As a simplistic example using dollars, suppose your $100 portfolio drops by 10% ($10) to $90. You now require an 11% gain to get back to $100.

TQQQ Is TQQQ A Good Investment for a Long Term Hold Strategy?

Probably not, at least not with 100% TQQQ. But there may be hope; stay tuned.

The graph above illustrates in theory why a 100% TQQQ position is not a good investment for a long term hold strategy.

Many are jumping into TQQQ after seeing the last decade bull run of large cap growth stocks, as TQQQ has only been around since 2010 and is up over 5,000% from then through 2020:

Looks great, right? Not so fast. This is called recency bias – using recent behavior to assume the same behavior will continue into the future. As we know, past performance does not indicate future performance. Moreover, a decade – especially one without a major crash – is a terribly short amount of time in investing from which to draw any sort of meaningful conclusions.

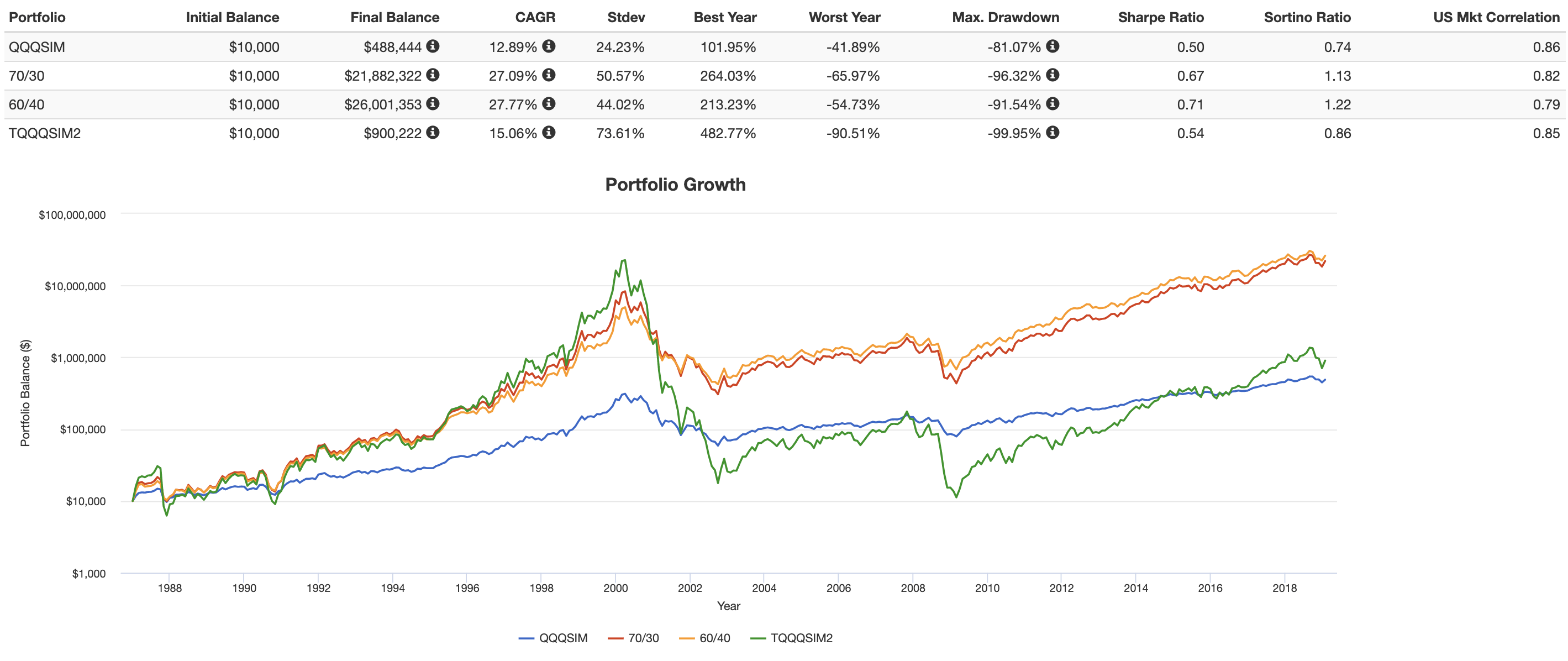

TQQQ vs. QQQ

So we need to go back further to get a better idea of how TQQQ performs through major stock market crashes, which we can do by simulating returns going back further than the fund’s inception. Going back to 1987 for TQQQ vs. QQQ tells a somewhat different story:

Notice how if you buy and hold TQQQ alone, it is basically a timing gamble that depends heavily on your entry and exit points. Basically, it can take too long for the leveraged ETF to recover after a major crash. After the Dotcom crash of 2000, TQQQ didn’t catch up to QQQ until late 2007 right before it crashed again in the Global Financial Crisis of 2008. Had you bought in January 2000 right before the Dotcom crash, you’d still be in the red today:

So far I haven’t even touched on the psychological aspects of this idea. Most investors severely overestimate their tolerance for risk and can’t stomach a major crash with a 100% stocks position, much less a 300% stocks position. Holding TQQQ through the Dotcom crash would have seen a near-100% drawdown.

A Viable Strategy for Long Term TQQQ – Use Bonds with TMF

The above graphs tell us 100% TQQQ is only a viable strategy if we can perfectly predict and time the market, which we know is basically impossible.

So how can we make it work? By using a hedge to mitigate those harmful drawdowns. Diversification is your friend with leveraged ETFs. Treasury bonds offer the greatest degree of uncorrelation to stocks of any asset. I explained here why you shouldn’t fear them.

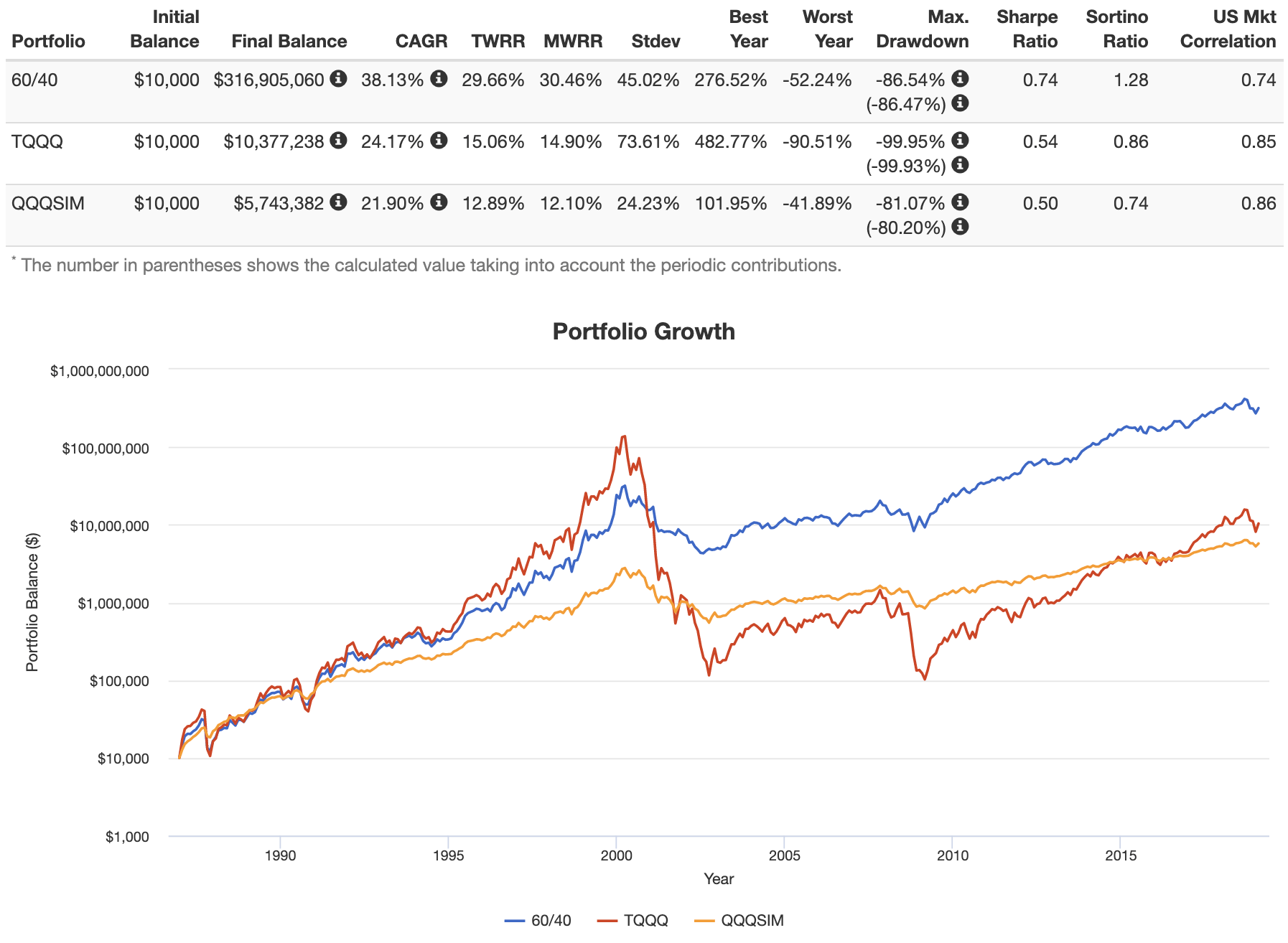

TMF is a very popular leveraged ETF for long-term treasury bonds. This is the same basis of the famous Hedgefundie Strategy. This idea is also extended with other assets like gold in my leveraged All Weather Portfolio.

Once again, the beautiful 60/40 portfolio – in this case 3x for 180/120 exposure – emerges as the best option (at least historically) in terms of both general and risk-adjusted returns:

While we expect lower bond returns in the future, it doesn’t mean TMF won’t still do its job. Think of it as a parachute insurance policy that bails you out in stock crashes.

Also remember the NASDAQ 100 is basically a tech index at this point, posing a concentration risk, and growth stocks are looking extremely expensive in terms of current valuations, meaning they now have lower future expected returns. For these reasons, I’m a fan of using UPRO instead (the Hedgefundie strategy).

Addressing Concerns Over Bonds

I’ve gotten a lot of questions about – and a lot of the comments in discussions on TQQQ strategies focus on – the use, utility, and viability of long-term treasury bonds as a significant chunk of this strategy. I’ll briefly address and hopefully quell these concerns below.

Again, by diversifying across uncorrelated assets, we mean holding different assets that will perform well at different times. For example, when stocks zig, bonds tend to zag. Those 2 assets are uncorrelated. Holding both provides a smoother ride, reducing portfolio volatility (variability of return) and risk.

Common comments nowadays about bonds include:

- “Bonds are useless at low yields!”

- “Bonds are for old people!”

- “Long bonds are too volatile and too susceptible to interest rate risk!”

- “Corporate bonds pay more!”

- “Interest rates can only go up from here! Bonds will be toast!”

- “Bonds return less than stocks!”

So why long term treasuries?

- It is fundamentally incorrect to say that bonds must necessarily lose money in a rising rate environment. Bonds only suffer from rising interest rates when those rates are rising faster than expected. Bonds handle low and slow rate increases just fine; look at the period of rising interest rates between 1940 and about 1975, where bonds kept rolling at their par and paid that sweet, steady coupon.

- Bond pricing does not happen in a vacuum. We’ve had several periods of rising interest rates where long bonds delivered a positive return:

- From 1992-2000, interest rates rose by about 3% and long treasury bonds returned about 9% annualized for the period.

- From 2003-2007, interest rates rose by about 4% and long treasury bonds returned about 5% annualized for the period.

- From 2015-2019, interest rates rose by about 2% and long treasury bonds returned about 5% annualized for the period.

- New bonds bought by a bond index fund in a rising rate environment will be bought at the higher rate, while old ones at the previous lower rate are sold off. You’re not stuck with the same yield for your entire investing horizon.

- We know that treasury bonds are an objectively superior diversifier alongside stocks compared to corporate bonds. This is also why I don’t use the popular total bond market fund BND. It has been noted that this greater degree of uncorrelation between treasury bonds and stocks is conveniently amplified during periods of market turmoil, which researchers referred to as crisis alpha.

- Again, remember we need and want the greater volatility of long-term bonds so that they can more effectively counteract the downward movement of stocks, which are riskier and more volatile than bonds. We’re using them to reduce the portfolio’s volatility and risk. More volatile assets make better diversifiers. Most of the portfolio’s risk is still being contributed by stocks.

- This one’s probably the most important. We’re not talking about bonds held in isolation, which would probably be a bad investment right now. We’re talking about them in the context of a diversified portfolio alongside stocks, for which they are still the usual flight-to-safety asset during stock downturns. Specifically, in this context, the purpose of the bonds side is purely as an insurance parachute to bail you out in a stock market crash. Though they provided a major boost to this strategy’s returns over the last 40 years while interest rates were dropping, we’re not really expecting any real returns from the bonds side going forward, and we’re intrinsically assuming that the stocks side is the primary driver of the strategy’s returns. Even if rising rates mean bonds are a comparatively worse diversifier (for stocks) in terms of future expected returns during that period does not mean they are not still the best diversifier to use.

- Similarly, short-term decreases in bond prices do not mean the bonds are not still doing their job of buffering stock downturns.

- Historically, when treasury bonds moved in the same direction as stocks, it was usually up.

- Interest rates are likely to stay low for a while. Also, there’s no reason to expect interest rates to rise just because they are low. People have been claiming “rates can only go up” for the past 20 years or so and they haven’t. They have gradually declined for the last 700 years without reversion to the mean. Negative rates aren’t out of the question, and we’re seeing them used in some foreign countries.

- Bond convexity means their asymmetric risk/return profile favors the upside.

- Again, I acknowledge that post-Volcker monetary policy, resulting in falling interest rates, has driven the particularly stellar returns of the raging bond bull market since 1982, but I also think the Fed and U.S. monetary policy are fundamentally different since the Volcker era, likely allowing us to altogether avoid runaway inflation environments like the late 1970’s going forward. Bond prices already have expected inflation baked in.

David Swensen summed it up nicely in his book Unconventional Success:

“The purity of noncallable, long-term, default-free treasury bonds provides the most powerful diversification to investor portfolios.”

Ok, bonds rant over. If you still feel some dissonance, the next section may offer some solutions.

Reducing Volatility and Drawdowns and Hedging Against Inflation and Rising Rates

It’s unlikely that any of the following will improve the total return of a strategy like this, and whether or not they’ll improve risk-adjusted return is up for debate, but those concerned about inflation, rising rates, volatility, drawdowns, etc., and/or TMF’s future ability to adequately serve as an insurance parachute, may want to diversify a bit with some of the following options:

- LTPZ – long term TIPS – inflation-linked bonds.

- FAS – 3x financials – banks tend to do well when interest rates rise.

- EDC – 3x emerging markets – diversify outside the U.S.

- UTSL – 3x utilities – lowest correlation to the market of any sector; tend to fare well during recessions and crashes.

- YINN – 3x China – lowly correlated to the U.S.

- UGL – 2x gold – usually lowly correlated to both stocks and bonds, but a long-term expected real return of zero; no 3x gold funds available.

- DRN – 3x REITs – arguable diversification benefit from “real assets.”

- EDV – U.S. Treasury STRIPS.

- TYD – 3x intermediate treasuries – less interest rate risk.

- TAIL – OTM put options ladder to hedge tail risk. Mostly intermediate treasury bonds and TIPS.

What About DCA / Regular Deposits Into TQQQ?

The backtests above buy and hold TQQQ with a starting balance of $10,000 and no additional deposits. Some will point out that an investor will usually be regularly depositing into the portfolio and that this would change the results. Since the market tends to go up and since major crashes are typically infrequent, regular deposits of $1,000/month into TQQQ actually doesn’t change the end result:

TQQQ/TMF Pie for M1 Finance

You’ll need to rebalance a strategy like this regularly, meaning getting allocations back into balance since these volatile assets may stray quickly from their target weights. I used quarterly rebalancing in the backtest above.

You might want to use M1 Finance to implement this type of strategy, as the broker makes rebalancing extremely easy with 1 click, and they even feature automatic rebalancing through which new deposits are directed to the underweight asset in the portfolio. I wrote a comprehensive review of M1 here.

Here’s a link for the M1 pie for 60/40 TQQQ/TMF.

Canadians can find the above ETFs on Questrade or Interactive Brokers. Investors outside North America can use Interactive Brokers.

Conclusion

Don’t go all in and don’t buy and hold TQQQ – or any leveraged stocks ETF – “naked” for the long term without a hedge of some sort, because sometimes they simply can’t recover from major drawdowns. The last decade has looked great for TQQQ, but don’t succumb to recency bias.

TMF is likely the most suitable hedge for funds like TQQQ and UPRO. For those with a weaker stomach who still want to use leverage, check out my discussion on levering up the All Weather Portfolio.

I also wouldn’t bother with any kind of forecast or price prediction. Technical analysis on a normal broad index ETF is already pretty meaningless. Trying to forecast a 3x LETF is almost certainly a fool’s errand.

Do you use TQQQ in your portfolio? Let me know in the comments.

Disclosure: I am long UPRO and TMF in my own portfolio.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Why not a simply strategy with moving average? Fe 170 dma out/in?

Is better solution than hefa.

I don’t try to time the market.

Great article, thanks John! I am still doing very well with TQQQ and my covered call strategy. Thank you.

Glad to hear it, John! Thanks!

Been a few years since you published the article, I am pretty heavy in tqqq and got in at a great time. I have been investing monthly into it and would like to know if you still consider leveraging TMF 60/40 as the most beneficial outcome for a longterm hold. Do you consider UPRO/TMF a better option?

Thanks for sharing, Blake! Congrats! I do still like the inclusion of TMF and I do still prefer UPRO.

Wonderful article and backtests! Thanks for all your hard work in this area.

I was drawn to the the 87% max drawdown even in the 60 TQQQ – 40 TMF portfolio, presumably during the Dotcom bust. Those who utilize leveraged ETF funds or anything QQQ-related must and do accept the wild volatilities that these strategies entail. However, a near-90% drawdown (even if in theory, let alone in actuality within the past two decades) probably makes even this hedged allocation a dead-on-arrival strategy, as no amount of outsized gains could make up for a real possibility of getting wiped out.

My question has to do with the mechanics of this. The whole point of hedging with bonds is that it is negatively or not correlated with the explosive returns of TQQQ, so I expected a less than 60% drawdown if the equites portion lost all value and the bonds held value or even gained during crash. Can you comment on how a near 90% wipeout occurred despite the hedging? And given the mechanics, could this strategy be salvaged to avoid that kind of wipeout – would something like a 50-50 or even 40 TQQQ-60 TMF allocation have fared notably better?

This would not have helped when it was needed the most, in all of 2022, when TQQQ and TMF were moving together in lockstep all year.

Slow bleed, not a sudden, severe crash. Certainly not ideal, but daily uncorrelation still held up just fine. That and both assets going down are not mutually exclusive. Long term strategy of necessity.

Another hedge portion of this strategy could be a basket of gold royalty stocks (WPM,FNV,RGLD). They tend to have low market correlation and around 3x gold returns, but without the geometric decay of a leveraged etf using swaps.

I wanted to go all in with TQQQ… Thanks for this instructive info,

Could you just clarify “You’ll need to rebalance a strategy like this regularly” please?

Suppose you have 50/50 TQQQ/TMF and TQQQ rises by 10% and TMF falls by 10%. Your allocation is now 55/45, so you would need to rebalance – selling TQQQ and buying TMF – to get back to your target 50/50 allocation.

if you’re dollar cost averaging TQQQ, then it doesn’t matter.. When the market recovers, TQQQ will be back at all time highs. If you keep loading up on it little by little, especially right now. You’ll be very rich in the next 10 years

I love your writing. I’m curious to see how you were able to backtest TQQQ in portfoliovisualizer all the way back to 1988 if the ticker as well as the tool only goes back to 2010 ? thanks in advance and keep up the great work!

Thanks Joey! As I noted in the post, I downloaded the historical returns data of the index to create my own simulation data and then uploaded that to PV as a custom data series.

Nice arcticle. Question: would this also apply to SOXL? for example since it’s down like 70% ytd it would need 233% gain to make up for it? Thanks alot.

Correct.

This article was written at basically a good time for the market. I know you don’t time the market, but at these levels, it might be worth the risk soon. Specifically TQQQ.

Really enjoyed reading your article. Look forward to reading more. What are your thoughts on using TQQQ long term in the 3 signal or 9 signal strategy as proposed by Jason Kelly in his book “The 3% Signal”?

Thank you,

Trey Cobb

Thanks, Trey. I don’t know what those strategies are. I’m not a fan of market timing in general; my technical analysis days are behind me.

Very thorough article. Thank you. Did you happen to compare your 60/40 TQQQ/TMF to 55/45 TQQQ/TMF? I am curious which one performs better (histortically). I suspect the difference is small, but not knowing is really bothering me. Haha. Thanks for your time.

No. The point was not to find an optimal allocation or even to suggest that as a strategy, but merely to show that diversifying is probably prudent when dealing with LETFs like TQQQ.

It seems that you used portfoliovisulaizer.com to simulate long term (before 2010) gains. But I am not able to simulate it for TQQQ cause the system keeps saying “The time period was constrained by the available data for TQQQ”. How did you do that?

As noted, created my own simulation data.

Hi, great article. But how do you get reliable pre-2010 data for TQQQ? As you mentioned, the fund didn’t exist…

As mentioned, created my own simulation data using the underlying index.

Are there steps by step instructions anywhere on how to do this? Thanks

Hey Bryant, there’s a thread on Bogleheads detailing the math but the steps are just:

1. Download daily historical return data of the underlying index.

2. Make a column in spreadsheet next to it for 3x those numbers minus fees and trading costs.

3. Done. Generate graph from spreadsheet or upload to PV as a custom data series.

I am long TQQQ with covered calls out-of-the money covered calls at various expiration dates and a range of strikes. For example, take a look at the premium of selling the Jan, 2024 $270 call. It has been in a range between $25 and $30. Now, consider re-investing the premium received and doing more buy/writes of TQQQ. My overall portfolio is about 66% TQQQ. Of the accounts that are TQQQ, they have a mix of about 60% in-the-money covered calls, and about 40% that are still out-of-the money. Again, every TQQQ share has a covered call associated with it.

Congrats.

I’m not sure I understand why one would do this. It’s basically limiting the extreme upside of TQQQ, of which is the reason to buy the ETF in the first place. It seems like a lot of busy work that may end up getting marginally better performance, if at all.

Agreed. Many tend to miss the fact that covered calls cap the upside.

Covered calls are a hedge against the stock same as buying a bond to hedge. I’m sure this guy has gotten hammered on his TQQQ over the last few months but still collected some premium from his covered calls

Covered calls are in no way a “hedge” and are definitely not the “same as buying a bond.”

I’m doing very well, with average cost per share well below $10, thank you.

doing very well now, thanks John

Great insight. Thank you for share. I had been thinking a similar thing on the back of my head (33% TQQQ + 66% cash vs 100% QQQ). I am glad you did the simulation out!

What do you think about buying a protective put option at let say 80% strike price quarterly? Will that be enough to cover the potential drawdown from any quarter?

Thanks!

Not sure. I don’t mess with options nowadays.

Hello John, great article, thank you for writing it!

How did you get the QQQ data and the treasury bonds as far as 1985? I’m particularly interested in the treasury bonds data: the ETF with oldest data that I can find is TLT, but it only dates back to 2003, after the dotcom bubble.

I did some back testing and I got the best performance (in the long term, both during bull and bear) by using a 5xQQQ that is rebalanced yearly. Have you tried anything similar? Would you personally consider using 5x ETFs or rebalancing yearly?

Leverage Shares seems to be the only provider of 5x ETFs, as far as I know: https://leverageshares.com/en/short-and-leveraged-etps/

Thank you!!

Thanks, Simone! I just downloaded historical returns data. For bonds just find a long treasury mutual fund like VUSTX.

No I would not use 5x. Those products are not ETFs.

Hi John,

Would you consider using VIXY for short-term hedging again liquidity crisis? e,.g. Mar 9 to Mar 20 last year?

Also, what is your take on TLT vs TMF: https://seekingalpha.com/article/4037686-why-tmf-will-tend-to-underperform-tlt-long-term

Would it make more sense to use margin for TLT instead of buying TMF directly?

Thanks

I don’t try to time the market. VIX futures are an insurance policy that isn’t worth the premium in my opinion. Can’t use margin in an IRA.

Great article. I’m still baffled as to how you can see the returns for HFEA and the 60/40 TQQQ/TMF portfolio and still only have 10% of your total portfolio allocated to HFEA…. You don’t think you’ll look back one day with regret?

Thanks, Adam. How can I only have 10% allocated to it? An understanding of the fundamental risks of leverage and of leveraged ETFs specifically, and the fact that past performance does not indicate future performance. Don’t succumb to recency bias and outcome bias.