SGOV was long one of the go-to ETFs for T-bills. Now Vanguard launched their own T-bills ETF with VBIL. Which should you choose? I compare them here.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

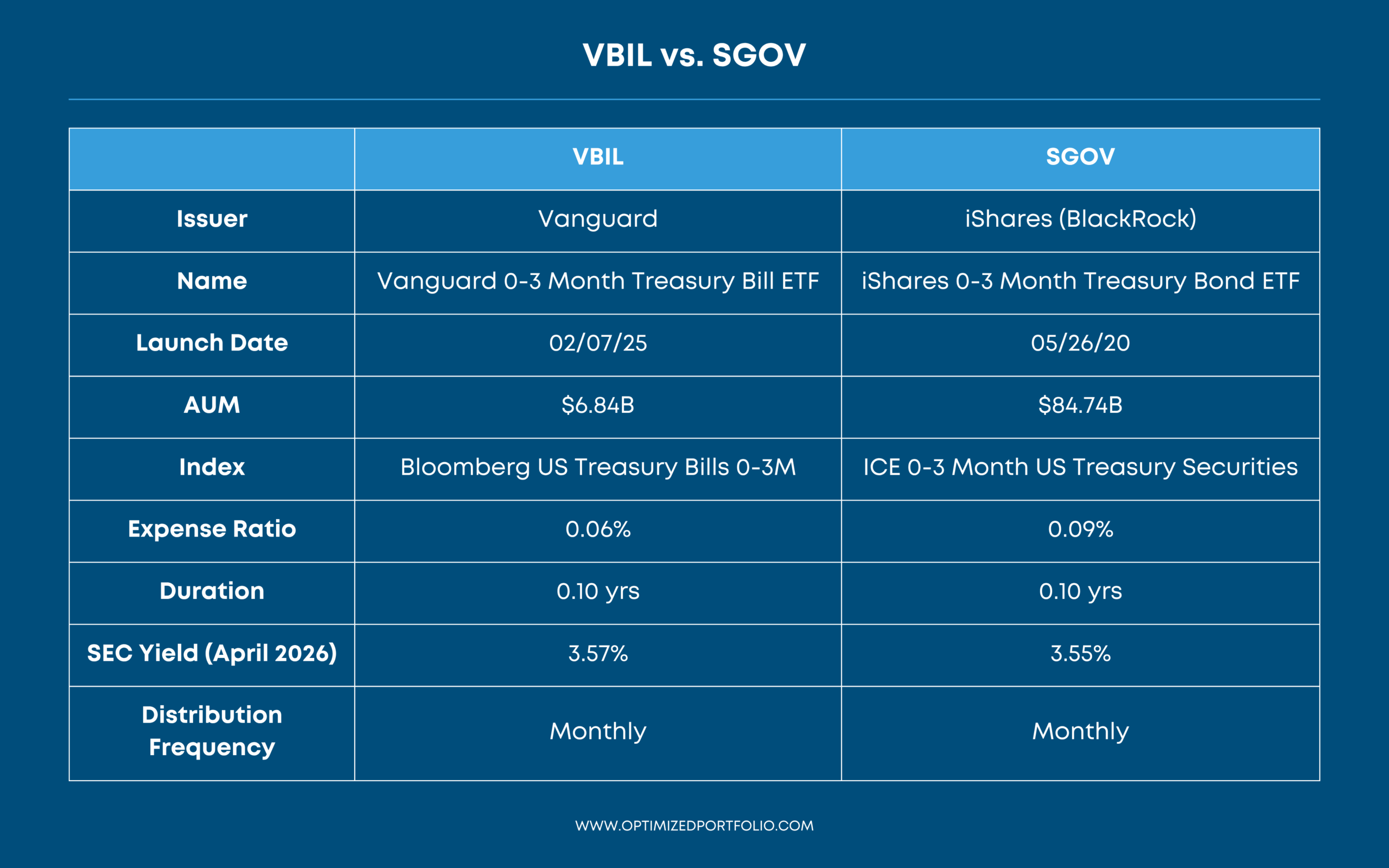

VBIL vs. SGOV Comparison Table

Before we get into details, here's a quick comparison table of VBIL vs. SGOV:

| VBIL | SGOV | |

|---|---|---|

| Issuer | Vanguard | iShares (BlackRock) |

| Name | Vanguard 0-3 Month Treasury Bill ETF | iShares 0-3 Month Treasury Bond ETF |

| Launch Date | 02/07/25 | 05/26/20 |

| AUM | $6.84B | $84.74B |

| Index | Bloomberg US Treasury Bills 0-3M | ICE 0-3 Month US Treasury Securities |

| Expense Ratio | 0.06% | 0.09% |

| Duration | 0.10 yrs | 0.10 yrs |

| SEC Yield (April 2026) | 3.57% | 3.55% |

| Distribution Frequency | Monthly | Monthly |

Data as of April 2026.

Here's that same comparison table as an image if you want to save or share it:

Intro – SGOV and T-Bills

So one of my most popular blog posts and videos is my simple overview of SGOV. This makes sense, as it has long been one of the most popular ETFs to capture short-dated US Treasury Bills, or T-bills for short, with over $80 billion in assets at this point in 2026.

T-bills are considered to be what we call a “cash equivalent,” a safe parking spot for unused cash that would be roughly comparable to the virtual risklessness of a savings account at a bank. In fact, the 3-month US Treasury Bill is quite literally known as the “risk-free rate,” to which other assets' yields are compared. The yield of T-bills is still looking pretty attractive in 2026 near 4%.

Both VBIL and SGOV function as continuously rolling T-bill ladders wrapped in ETF packaging. The fund holds roughly 28 individual Treasury bill issues spread across the 0-3 month maturity spectrum. When a T-bill in the portfolio matures and redeems at face value, the proceeds get reinvested into freshly issued T-bills at the next auction. You never touch anything. You just own a share of the fund and collect monthly distributions.

This is the appeal: all the yield of holding T-bills directly but none of the manual auction management and calendar gymnastics that comes with TreasuryDirect.

NAV stability comes from the ultra-short duration. With an effective duration of a little over 1 month, a 1% move in interest rates shifts the NAV by roughly 0.1%, which is just noise. SGOV's 52-week price range has been $100.27-$100.74. That's less than half a percent of variation over an entire year. The NAV does follow a predictable sawtooth pattern: it drifts slightly upward as T-bill discount accretes between distributions, and then drops on ex-dividend dates when monthly income is paid out.

SGOV from iShares launched in 2020, and investors have since flocked to it for their cash management needs due to both the robust history of iShares as a fund provider and the relatively low fee of SGOV at 0.09%.

Vanguard Launches VBIL

After weirdly previously having no products for Treasury Bills, Vanguard finally launched 2 new ETFs for them in 2025 in the form of VGUS for bills maturing in less than 12 months, and VBIL – the one more comparable to SGOV – for bills maturing in 3 months or less. I briefly summarized VGUS and VBIL in a separate post here.

Vanguard investors are particularly happy to now have Vanguard products for Treasury Bills, but all investors are potentially interested in these new offerings because their expense ratio of 0.06% is slightly lower than that of SGOV at 0.09%. I'd also be willing to bet that fee will come down further in the coming years, as is the Vanguard way. VBIL has very quickly amassed an impressive $3 billion in assets in about 6 months since it launched in early 2025.

Now that it's been out for a year, 2026 feels like a good time to make the comparison to SGOV and see what's what.

VBIL vs. SGOV – Index Implications on Taxes

VBIL and SGOV can be considered, for all intents and purposes, nearly identical. Both hold T-bills with maturities of 3 months or less, albeit via different indexes. But that index difference does have a subtle implication.

SGOV seeks to track the ICE 0-3 Month US Treasury Securities Index, while VBIL seeks to track the Bloomberg 0-3M Treasury Bill Index. In practice, the portfolios end up being almost identical, since the vast majority of securities with sub-3-month maturities are T-bills. The more meaningful difference is in how each index handles cash between rebalance dates.

SGOV's ICE index rebalances monthly on the last calendar day of each month and doesn't provide for reinvestment of maturing proceeds between those dates. So when T-bills mature mid-month, the proceeds sit in cash, specifically in BlackRock Cash Funds (repos), until the next rebalance. As of year-end 2025, about 6.7% of SGOV's portfolio was sitting in these repo vehicles at any given time.

Repos, while backed by Treasuries, are not considered direct U.S. government obligations for state income tax purposes. This is why SGOV's state tax-exempt percentage is about 97.5% instead of 100%.

VBIL doesn't have this problem. It achieves 100% state tax exemption by avoiding repos entirely and investing directly in T-bills throughout the month. For investors in high-tax states, this is a tiny but real advantage.

VBIL vs. SGOV – Performance and Distributions

Performance-wise, we'd expect VBIL and SGOV to behave nearly identically, at least pre-tax, and indeed they have thus far in VBIL's short lifespan. When two products offer the same exposure, I think it's reasonable to simply prefer the one with the lowest fee, which is VBIL. Basically, VBIL is the cheaper Vanguard equivalent of SGOV.

In the interest of full disclosure, extending that logic, there are other comparable funds for T-bills at the same or lower fees like XHLF, for example, which I covered in a list here.

Both VBIL and SGOV distribute dividends monthly, which will show up on 1099-DIV (not 1099-INT) since they're ETFs.

What do you think of VBIL? Are you going to switch to it from SGOV? What's your T-bills ETF of choice? Let me know in the comments.

Disclosures: None.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Leave a Reply