Financially reviewed by Patrick Flood, CFA.

Index investing is a simple yet powerful approach to consistent investment portfolio growth. Here we’ll explore what index funds are, their benefits, how they work, how to invest in them, and some of the best index funds for 2024.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

[toc]

What Is an Index Fund?

An index fund, as the name implies, is simply an investment product designed to track a particular index in the stock market. There are many indexes, broad and narrow, for different asset types. Some of the most popular indexes are ones like the S&P 500, the Dow Jones, and the Nasdaq 100, for example, which track subsets of the U.S. stock market. A notable distinction is that investors cannot directly invest in an index per se; an index fund that tracks the index must be used.

Indexes can be composed by a committee based on specific criteria, like the S&P 500, or strictly calculated formulaically, like with the Russell 1000. The nuances of that composition methodology are largely negligible, as the S&P 500, for example, is still an excellent barometer for “the market” as a whole because it is a broad index that contains over 500 companies that span all industries of the U.S. economy.

Other indexes are more narrowly focused, such as the NASDAQ US Dividend Achievers Select Index, which tracks a subset of companies in the S&P 500 that have a history of an increasing dividend payment, and the MSCI US Investable Market Information Technology Index, which tracks stocks in the technology sector. In this sense, while index investing is often associated with broad indexes like the total stock market, technically, investors can still call themselves “index investors” while using narrow sector funds or specific market segments.

Index funds abound based on cap sizes, geography, sector, asset type, niche markets, and more. Be wary of narrowly-focused index funds with inherently less diversification, more risk, and higher fees. Typically, as the fund narrows in scope, risk and fees increase.

Index funds simply replicate the behavior of the index, usually by holding most, if not all, of the same assets as the index itself. Let’s look at the benefits of index funds.

The Benefits of Index Funds

So why are index funds advantageous? If you’ve landed on this page, you likely already know that most active managers underperform their benchmark index, and that simply buying an index fund tends to be the best long-term investing strategy. John Bogle, founder of Vanguard and considered “the father of index investing,” suggested that investors should simply “buy the whole haystack” instead of looking for the needle. Warren Buffett agrees, writing in a 2016 letter to shareholders that “when trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap outsized profits, not the clients. Both large and small investors should stick with low-cost index funds.”

The evidence has shown that even most professional investors can’t pick winners that beat the market over 10+ years, much less the average retail investor like you and me. On the 50th birthday of the S&P 500 index, only 86 of the original 500 companies remained. Blindfolded monkeys randomly throwing darts for stock picks have beaten top hedge fund managers not just once, but consistently.

Most stocks underperform the market; only a select few drive massive returns. Specifically, for U.S. stocks from 1926 through 2017, in terms of lifetime dollar wealth creation, only 4% of stocks accounted for the net gain above T Bills. Looking at global stock returns from 1990 through 2018, only 1.3% of stocks accounted for the positive wealth creation in excess of T Bills. In short, we should reliably expect to see the empirical results we’ve observed historically: that stock picking strategies, especially those that are poorly diversified, tend to underperform the market.

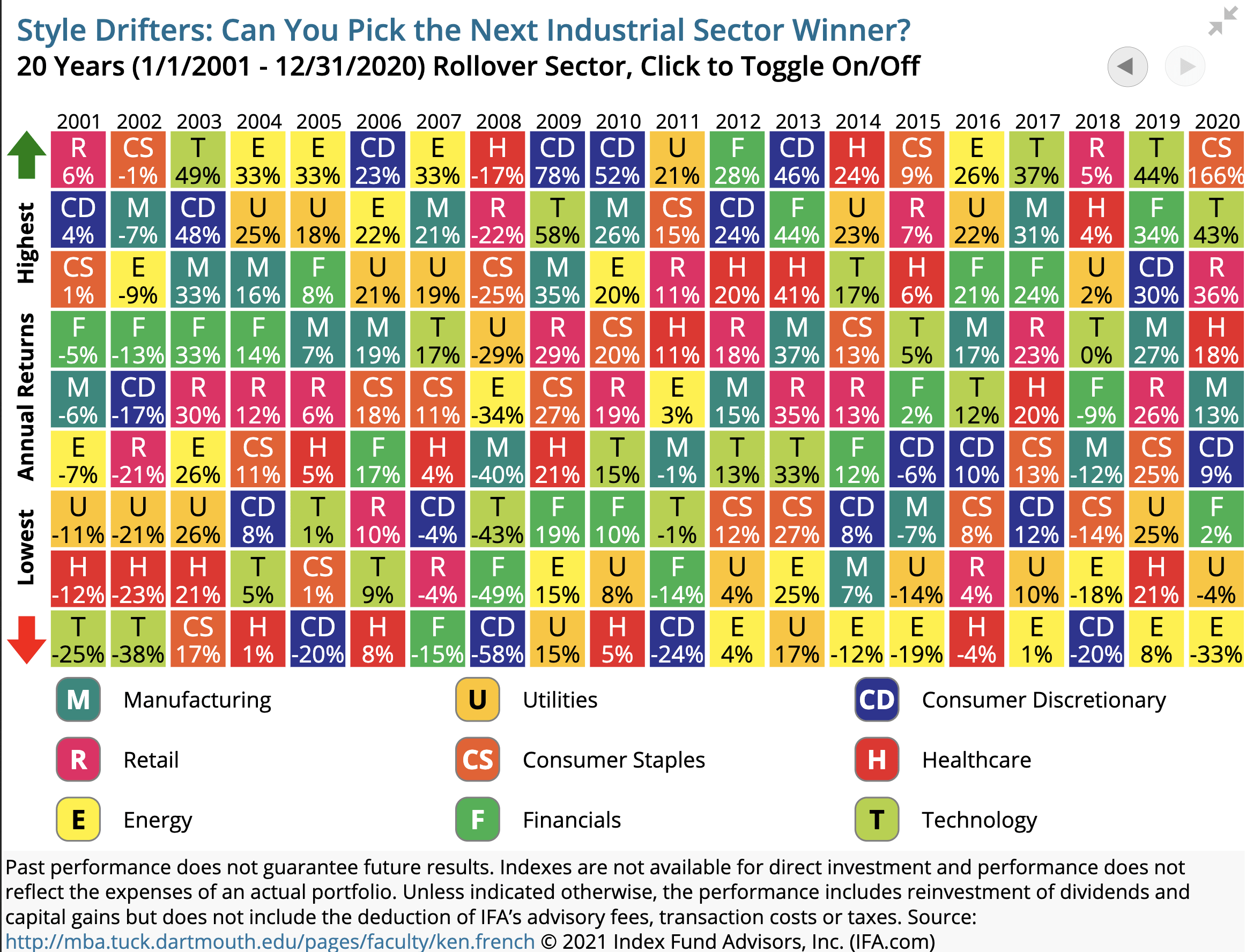

Even sector bets are usually not a prudent move, as they’re just stock picking lite. Betting on sectors increases uncompensated risk – additional risk without an increase in expected return. In doing so, investors increase their chances of underperforming the market. Just like with individual stocks, some sectors will outperform and some will underperform the market. How do we know which ones will do which? And during what time periods? What about different economic cycles? Tech has had a huge run recently. Will it continue? In short, no one knows:

The evidence also suggests that markets are efficient, meaning a stock’s price reflects all available information at any given point in time. That means anytime you as a retail investor get any news about a company, that news has already been “priced in” to its share value. As new information comes out, prices change, but that new information is impossible to accurately predict consistently.

Markets are forward-looking. Expectations of any company’s growth/decline are also already reflected in the share price. For a stock’s share value to grow, any future earnings must exceed those expectations, which may already be high. Similarly, a company’s share value can drop if those earnings are less than investors’ collective expectations, even if those earnings result in growth and profitability for the company itself.

People tend to be confused in certain instances like when the market rises after unemployment reports come out – this is because the numbers weren’t as bad as investors as a whole expected. Moreover, Wall Street spends millions of dollars to get these pieces of information days, hours, even minutes before they’re made public, so you are always at a disadvantage in trying to pick stocks or project their movement because of this asymmetrical availability of information.

Think of indexing versus stock picking almost like the tortoise versus the hare. With index funds, we’re the former, slow and steady. Naturally, in doing so, we’re never going to hit a home run. A little speculation/picking is fine to keep things fun, just don’t do it with the bulk of your portfolio. Diversification seems to be the only free lunch with investing. If you want to try to pick some unicorn stocks, do so with no more than 10% of the portfolio. As Bill Bernstein says, the goal should not be to get rich, but rather to avoid dying poor.

Such is the beauty of index funds. You get exposure to the success of any sector and any stock at any given time in a market index fund, while altogether eliminating sector risk and single company risk. They’re also self-cleansing in that growing companies rise within the fund and bad companies drop off. They allow you to immediately access broad diversification, thereby lowering portfolio volatility and risk, avoiding high fees that erode returns, and guaranteeing market returns. This is especially important for young and/or beginner investors. Simplicity is also an important benefit of index funds, as complexity can add unnecessary time, effort, and headache.

Index funds allow you to sit back, relax, and be hands-off in your investing journey. You have full transparency knowing exactly what you’re invested in at all times, whereas actively managed funds only disclose holdings once quarterly. Thankfully, people are wisening up to these facts, and index investing is rapidly growing in popularity. Gone are the days when average investors were forced to pay high fees to managers and advisors.

Another added benefit of index funds is their relative tax-efficiency. Because the composition of broad indexes doesn’t change often, index funds usually have low turnover. That is, they don’t do a lot of buying and selling, thus avoiding capital gains, making them suitable for a taxable brokerage account. You can also obviously invest in index funds in your 401(k) or IRA.

What About Active Management and “Downside Protection?”

Okay, so we don’t expect active managers to be able to pick winners and outperform the market. But what about “protecting the downside?” Wouldn’t active managers be better able to hedge against market turmoil by avoiding losers?

This is the primary argument trotted out in favor of active management – that the skill of managers picking securities allow your investments to perform better and more smoothly through market downturns, effectively losing less than the market. The idea is that active managers can adjust the portfolio on the fly to minimize losses.

Unfortunately, the evidence says this isn’t the case. Essentially, consistently successful defensive skill is rare, and one-time instances can usually be chalked up to luck. Managers that are able to lose less than the market during one downturn are almost never able to repeat that feat during the next period of market turmoil, much less over a long-term horizon through multiple downturns.

Remember, greater risk in the market as a whole is usually compensated by greater reward. Consequently, it is basically impossible to build a portfolio that is expected to outperform the market that also has lower risk than the market. Over the long term, on average, actively managed funds either outperform during bull markets and underperform during bear markets, or vice versa; they cannot do both consistently.

In the bear market of 1998, for example, the S&P 500 dropped 19% while the average managed fund dropped 22.2%. In 2008, Standard & Poor’s themselves concluded: “The belief that bear markets favor active management is a myth. A majority of active funds in eight of the nine domestic equity style boxes were outperformed by indices in the negative markets of 2008. The bear market of 2000 to 2002 showed similar outcomes.”

Remember too that all this is before fees and commissions, which eat into the returns from active management even more. Because of this, as Nobel-winning economist William Sharpe pointed out in The Arithmetic of Active Management, the average passive index fund investor must necessarily outperform the average active investor, as managers cannot generate enough consistent alpha to overcome their own fees.

Those wanting “downside protection” in bear markets should turn to things like bonds, Utilities, and Consumer Staples that tend to rise – or at least fall less – than the market during stock crashes.

Now that you know why index investing is a great long-term investing approach, let’s dive into how index funds work.

How Do Index Funds Work?

Index funds are the investment vehicles, traded as a mutual fund or ETF (exchange-traded fund), that replicate the behavior and performance of the underlying index they seek to track. So how do they do that?

Index funds usually simply hold the same securities, at the same weights, as the underlying index. This can be 100% of the components of the index, or a sufficiently representative sample. Index funds are usually weighted by the market capitalization (size) of the companies they hold. These funds usually use passive management and formulaic sampling to attempt to track the index, which keeps fees low, as opposed to active management where managers seek to beat the index by manually analyzing and selecting investments, which commands higher fees.

Brokers usually do not disclose their exact sampling methodology, but we can see and quantify the tracking error of index funds, or how accurately they mimic the index. Specifically, tracking error refers to the difference in the net asset value (NAV) of the fund’s holdings and the value of the components of the index in aggregate. A greater tracking error means less accurate replication of the index. An index fund that simply buys 100% of the investments in the index at their respective weights will have zero tracking error, but would be more expensive to manage – and thus would have higher fees – than an index fund that uses representative sampling. Vanguard, for example, is famous for using index sampling and still minimizing tracking error, resulting in some of the lowest fees around for their index funds.

Those fees for funds are called expense ratios. Again, Vanguard has always been a pioneer for lowering fees, making investing more accessible and more profitable for the average DIY retail investor. Most of their broad index funds have expense ratios less than 0.10%. In comparing two equal funds, expense ratio is a major factor to consider, as fees can eat into returns.

Now that you know how index funds work, let’s look at how to invest in an index fund.

How To Invest in an Index Fund

Again, index funds come in the form of passive mutual funds and ETFs (exchange-traded funds), both of which can be bought through a typical brokerage. These investment vehicles track an index as described above so that you can just buy shares of a single product instead of buying hundreds of different individual stocks. Mutual funds and ETFs are very similar, but there are some key differences to note:

- Mutual funds usually have a minimum investment requirement. ETFs do not.

- The share price for mutual funds is calculated and executed at the end of the trading day on which the order placed. With ETFs, you have control over the price at the time of the order, as they are traded just like stocks on an exchange.

- Mutual funds are sometimes actively managed, which usually means higher fees.

Considering these things, ETFs can be seen as more flexible than mutual funds. Most passively managed mutual funds have an ETF equivalent.

So to invest in an index fund, all you need to do is choose an online broker (I’d suggest M1 Finance; I wrote a review of it here), choose an index (or a few) to invest in, e.g. the S&P 500, and buy as many shares as you’d like. It’s that simple! Don’t know which index(es) to choose? Let’s look at some of the best index funds.

The Best Index Funds – Stocks

There is a wide variety of index funds out there, but not all index funds are created equal. In selecting the best index funds, we’re looking for high liquidity, low tracking error, low fees, broad diversification, a reliable provider, and a solid track record. I’m usually a fan of Vanguard funds whenever possible, as they typically offer the lowest fees, so you’ll see many Vanguard index funds in the list below. Vanguard actually invented and introduced the first index fund in 1976. The abbreviation of each fund you see below is called the ticker symbol, used to quickly find the fund when placing an order through a broker.

VOO – Vanguard S&P 500 ETF

No list of index funds is complete without the stalwart S&P 500 index. It is the most popular index to invest in, comprised of the 500 largest American companies that make up roughly 82% of the entire U.S. stock market. The historical annualized return of the S&P 500 has been about 10%. VOO is Vanguard’s ETF to track the S&P 500 index. The fund was established in 2010 and has an expense ratio of 0.03%.

VTI – Vanguard Total Stock Market ETF

Whereas VOO only contains large companies, the total U.S. stock market contains roughly 18% smaller companies, known as small-cap and mid-cap stocks. Interestingly, small- and mid-caps have outperformed large-caps historically, though they are naturally slightly more risky. You can access these with an index fund that tracks the entire U.S. stock market. VTI from Vanguard does just that, tracking the CRSP US Total Market Index. VTI is a component of many lazy portfolios. The fund contains over 3,500 stocks and has an expense ratio of 0.03%.

VXUS – Vanguard Total International Stock ETF

While VTI is the whole U.S. stock market, VXUS from Vanguard is the entire international (ex-US) stock market. Most U.S. investors have home country bias, favoring U.S. stocks, but international stocks provide an important diversification benefit because they are not perfectly correlated with U.S. stocks. During the period 1970 to 2008, an equity portfolio of 80% U.S. stocks and 20% international stocks had higher general and risk-adjusted returns than a 100% U.S. stock portfolio. I choose to allocate 20% to international stocks in my portfolio.

VXUS seeks to track the FTSE Global All Cap ex US Index. In other words, this ETF is composed of all stocks outside the United States. VXUS is an important piece of the Bogleheads 3 Fund Portfolio. This fund has an expense ratio of 0.08%.

VT – Vanguard Total World Stock ETF

We can go one step further and combine the last two funds to arrive at the global stock market via Vanguard’s Total World Stock ETF, which tracks the FTSE Global All Cap Index. This gets you fully diversified globally with stocks across all sectors, geographies, and cap sizes. At their market weight, U.S. stocks account for roughly half of the global stock market. VT contains over 8,500 stocks and has an expense ratio of 0.08%.

VIG – Vanguard Dividend Appreciation ETF

Prefer dividend stocks? The Vanguard Dividend Appreciation ETF invests in stocks with a history of an increasing dividend payment that comprise the NASDAQ US Dividend Achievers Select Index (formerly known as the Dividend Achievers Select Index). This fund contains a little over 200 stocks and has an expense ratio of 0.06%.

I analyzed VIG in detail in a separate post here.

VTWO – Vanguard Russell 2000 ETF

Want to only invest in small companies? The Russell 2000 index contains the 2,000 smallest stocks in the U.S. stock market. It is the most common benchmark for “small-cap” index funds. VTWO from Vanguard tracks that index and carries an expense ratio of 0.10%.

QQQ – Invesco QQQ Trust

QQQ from Invesco tracks the famous NASDAQ 100 index, which is composed of mostly tech stocks. The index holds the largest non-financial companies listed on the NASDAQ exchange. This collection of stocks has had a great run in recent years from the stellar performance of Big Tech. In fact, Apple, Amazon, and Microsoft make up over 1/4 of this index. The fund has over $100B in assets and has an expense ratio of 0.20%.

ESGV – Vanguard ESG U.S. Stock ETF

A new wave of interest surrounds socially responsible investing – investing in companies that are screened for specific criteria based on environmental, social, and corporate governance (ESG). This fund from Vanguard tracks the FTSE US All Cap Choice Index, excluding stocks in the following industries: adult entertainment, alcohol, tobacco, weapons, fossil fuels, gambling, and nuclear power, as well as companies that do not meet standards of U.N. global compact principles and companies that do not meet certain diversity criteria. This fund has an expense ratio of 0.12%.

VNQ – Vanguard Real Estate Index Fund

Investing in real estate can add some extra diversification to a stock portfolio with its low correlation to the stock market. This is done with Real Estate Investment Trusts, or REITs for short. The Vanguard Real Estate Index Fund is the most popular REIT fund and seeks to track the MSCI US Investable Market Real Estate 25/50 Index. This fund has an expense ratio of 0.12%.

The Best Index Funds – Bonds

Bonds are the primary diversifier and flight-to-safety asset of choice because they tend to go up when stocks go down, providing downside protection and reducing portfolio volatility and risk. Based on your personal risk tolerance and time horizon (and subsequent asset allocation), you may want some bonds in your portfolio. Here are some of the best bond index funds.

AGG – iShares Core U.S. Aggregate Bond ETF

To diversify within bonds, investors can simply get exposure to the entire U.S. bond market via the iShares Core U.S. Aggregate Bond ETF, which tracks the Barclays Capital U.S. Aggregate Bond Index. This index includes treasury bonds, corporate bonds, and mortgage-backed securities (MBS). The fund has an expense ratio of 0.05%.

BNDX – Vanguard Total International Bond ETF

To diversify even further with bonds, investors may opt to go outside the U.S. and invest in foreign bonds. BNDX from Vanguard tracks the Bloomberg Barclays Global Aggregate ex-USD Float Adjusted RIC Capped Index (USD Hedged) and has an expense ratio of 0.08%. BNDX is the prescribed foreign bond holding in the Bogleheads 4 Fund Portfolio.

GOVT – iShares U.S. Treasury Bond ETF

If you’re like me, you might prefer to only invest in government debt on the bonds side. The iShares U.S. Treasury Bond ETF seeks to track the Barclays Capital U.S. Treasury Bond Index, providing broad exposure to the U.S. Treasury Bond market. This fund has an expense ratio of 0.15%.

Where to Buy These Index Funds

All of these ETFs should be available at any major broker. My choice is M1 Finance. The online broker allows you to construct your own custom portfolio of stocks and/or ETFs, or simply invest in pre-made, expert-built portfolios of low-cost ETFs. M1 has zero fees and offers fractional shares, dynamic rebalancing, and a modern, user-friendly interface and mobile app. I wrote a comprehensive review of M1 Finance here.

Canadians can find the above ETFs on Questrade or Interactive Brokers. Investors outside North America can use Interactive Brokers.

Disclosures: I am long VOO in my own portfolio.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Thanks for creating great educational content on investing John!

Are there any specific reasons to you tilt towards Vanguard funds compared to Schwab’s like SCHG, SCHD, etc? I’ve found these tickers have provided slight alpha over their Vanguard counterparts looking at past 10 years performances and the fees/expense-ratios are lower if not comparable.

When talking about the best performing ETF you completely missed the boat. What about SOXL? It left all the others in the dust.

I don’t really talk about the “best performing ETF,” because that has no bearing on the future. SOXL is a 3x leveraged semiconductors fund; enough said.