The term “lazy portfolio” refers to a portfolio designed to perform well in most market conditions, that can be held for an extended period without changing the asset allocation leading up to retirement. Popular examples are the traditional 60/40 Portfolio and the Bogleheads 3 Fund Portfolio.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Lazy portfolios are usually simple, diversified collections of low-cost index funds; no active management, market timing, or stock picking here. Jack Bogle, founder of Vanguard and considered the father of index investing, advocated for the “majesty of simplicity.” In this case, “lazy” isn't a bad thing.

Lazy portfolios arguably take index investing even further, taking the guesswork and complexity out of investing, allowing the investor to truly be “lazy” in their investing approach by eliminating the need to choose funds and the allocations thereof; the investor need only occasionally rebalance their lazy portfolio. This saves the investor time and alleviates potential stress and cognitive dissonance related to investing strategies, and also mitigates the investor's own biases. As such, they're perfect for the long-term buy-and-hold investor who wants to be hands-off. These benefits of portfolio simplicity are too often overlooked.

Below is an ever-evolving list of lazy portfolios, with links to my usually-brief analysis/review of each. On each respective page is a link to a pie of ETFs for use with M1 Finance. Whenever possible, I'm usually using low-cost Vanguard funds, or whichever provider has the lowest fees with sufficient AUM.

Canadian investors can use Questrade, and those outside North America can use eToro.

Similarly, when a particular risk factor is targeted, I've selected the fund with a favorable balance of factor loading, fees, and volume. I try to review and update these regularly as new funds emerge that may be a superior choice.

A lot of people email me asking which is the best lazy portfolio. That's subjective and highly personal; there's no single correct answer. “Best” for one person could mean greatest expected return. “Best” for someone else may mean the lowest volatility. More advanced investors may prefer a lazy portfolio that heavily utilizes factor tilts; others prefer simplicity.

Start by assessing your personal goals, risk tolerance, and time horizon, and choose an appropriate asset allocation. The “best lazy portfolio” is the one that allows you to sleep easy at night, ignore the short-term noise, avoid tinkering, and stay the course.

In most cases of US-only equities, I've also created a global version to capture international stocks for those understandably wanting more diversification.

Comment or email to request a lazy portfolio that I may have missed or haven't seen yet. The list of lazy portfolios below is in no particular order.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

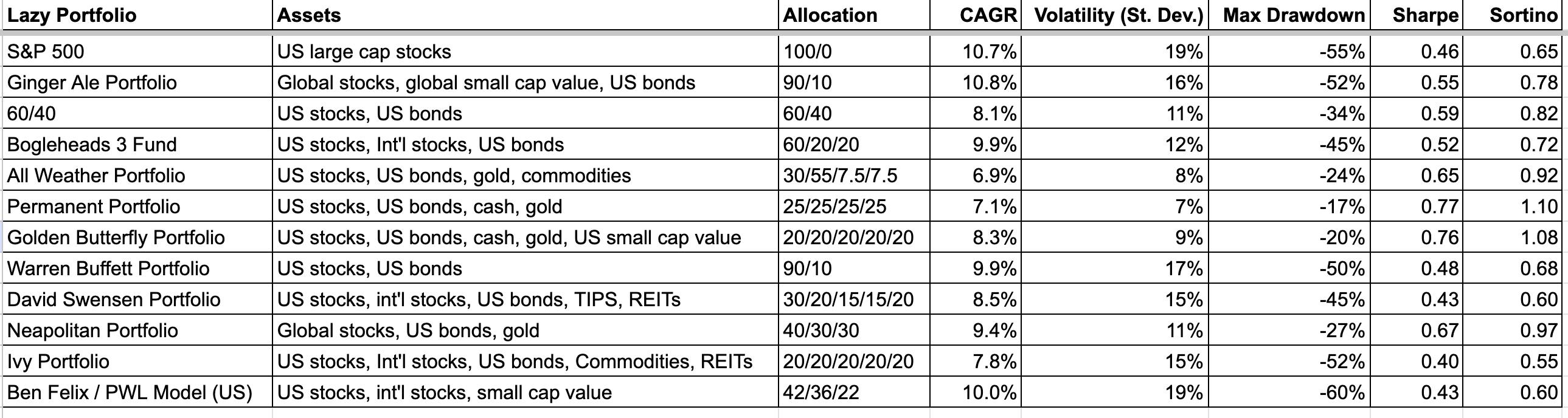

Lazy Portfolios Comparison Chart

I created a little comparison chart of some of the most popular lazy portfolios below. Here's the link to the Google Sheet. Take this with a handful of salt because I had to keep the time period the same of only about 22 years – which is terribly short – due to TIPS and Commodities only going back that far, and those are in portfolios like the Ivy Portfolio and Swensen's Yale Model. This chart basically just illustrates the effect of diversification on the efficiency of the portfolio (i.e. Sharpe and Sortino). Again, don't just choose a strategy because it had the highest return or the highest Sharpe ratio in recent years. I may add more to this sheet as time allows.

List of Lazy Portfolios

- Ginger Ale Portfolio (my own portfolio)

- Vigorous Value Portfolio (my design)

- Neapolitan Portfolio (my design)

- Factor Tank Portfolio (my design)

- Sample Retirement Portfolio (my design)

- Tom's Tail Risk Portfolio (my design)

- Ray Dalio All Weather Portfolio

- Golden Butterfly Portfolio

- Harry Browne's Permanent Portfolio

- Bogleheads 3 Fund Portfolio (global stocks, U.S. bonds)

- Bogleheads 4 Fund Portfolio (global stocks, global bonds)

- Bogleheads 2 Fund Portfolio (global stocks, global bonds)

- Warren Buffett ETF Portfolio (90/10)

- Paul Merriman Ultimate Buy and Hold Portfolio

- Paul Merriman 4 Fund Portfolio

- Ben Felix Model Portfolio

- 60/40 Portfolio

- Hedgefundie's Excellent Adventure (not “lazy,” I know; not for beginners)

- Custom Emergency Fund Replacement (low risk)

- David Swensen Portfolio (Yale Model)

- Meb Faber Ivy Portfolio

- Bernstein No Brainer Portfolio

- Bernstein Coward's Portfolio

- Frank Armstrong Ideal Index Portfolio

- Bob Clyatt Sandwich Portfolio

- Pinwheel Portfolio

- Bill Schultheis Coffeehouse Portfolio

- John's High Dividend Pie (for dividend income investors)

- Second Grader's Starter Portfolio

- All Asset No Authority Portfolio

- Larry Swedroe Portfolio (30/70, small cap value)

- Tim Maurer Simple Money Portfolio

- Rick Ferri Core 4 Portfolio

- JL Collins Simple Path to Wealth Portfolio

- Rob Arnott Portfolio

- Research Affiliates Model Portfolios

- Craig Israelsen 7Twelve Portfolio

- Roger Gibson 5 Asset Portfolio

- Roger Gibson Talmud Portfolio

- Gyroscopic Investing Desert Portfolio

- Scott Burns Couch Potato Portfolio (50/50)

- Scott Burns Margarita Portfolio

- Alexander Green's Gone Fishin' Portfolio

- NTSX with Diversification

- PSLDX Replication

- RPAR Replication

- SWAN + Gold

- Return Stacked Quad Core Portfolio

- Improved M1 Finance Ultra Aggressive Portfolio Expert Pie (100/0)

- Improved M1 Finance Aggressive Portfolio Expert Pie (90/10)

- Improved M1 Finance Moderately Aggressive Portfolio Expert Pie (80/20)

- Improved M1 Finance Moderate Portfolio Expert Pie (70/30)

- Improved M1 Finance Moderately Conservative Portfolio Expert Pie (60/40)

- Improved M1 Finance Conservative Portfolio Expert Pie (40/60)

- Improved M1 Finance Ultra Conservative Portfolio Expert Pie (20/80)

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

What do you think of Paul Merriman’s new two fund portfolio? (50% S&P 500, 50% Small Cap Value)

it would be super nice to have a combined spreasheet that showes the top 10 performers of this mix of lazy portfolies

Depends on time period. That will vary. I may try to work up something like this.

Could you please create a post on a lazy portfolio based on Jane Bryant Quinn’s book “How to Make Your Money Last?” Thank you!

Thank you for all the great work. Your article on Ray Dalio All Weather Portfolio has been one I’ve referred to many times. Are there any other portfolios with a similar level risk adjusted return to your 3X AWP (w Util) ? I appreciate your continued exploration. Well done.

Thanks, J Edward! Off the top of my head I’m not sure of a comparable risk-adjusted return portfolio but you could probably compare the backtests on some of those in the list. Maybe I’ll do a future post on that topic specifically. I know historically a 30/70 allocation has produced the highest risk-adjusted return so that makes me think of ones like the Swedroe Portfolio and Desert Portfolio.

Thank you very much for creating this amazing content John!

I’m a long time reader, first time poster out of Europe. I find your advice a lot more sensible than many other sources. I admire your ability to dumb down complex topics and also totally appreciate that you provide direct, actionable advice without BS (or marketing).

Even though your choice of funds are not available in Europe, where we lack some variety and pay a lot more fees for UCITS ETFs, I have learned a great deal from your articles. As a result, I have been tweaking my portfolio very gradually to increase my international diversification and factor exposure. Until very recently, my “diversified” portfolio consisted of a single actively managed fund that invested ~80% in Nasdaq 100 and charged over 2% in fees! I have been dollar cost averaging into it for a very long time though and got very good returns out of pure luck, in spite of my ignorance…

I hope my comment will motivate you to provide some content specifically for European investors in the future, considering what is available to us over here. I would also like to get your take on Gerd Kommer’s portfolios for example, especially the one with 20% exposure to 5 factors.

Thanks again for what you do!