A backdoor Roth IRA is a way for high income earners to indirectly contribute to a Roth IRA who would otherwise be ineligible. Here we'll look at what it is and where, why, and how to open one.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

What Is a Backdoor Roth IRA?

A backdoor Roth IRA is a way for high income earners to still be able to contribute to the account from which they'd otherwise be ineligible based on their income level.

An important thing to note right off the bat is that the “backdoor Roth IRA” is a technique or process, not an account type. In that sense, the phrase “open a backdoor Roth IRA” technically doesn't really make sense. The name refers to a strategy to indirectly contribute to a Roth IRA, hence the name “backdoor.”

Moreover, “backdoor Roth IRA” is not an officially recognized term by the IRS. Thus, you might have an easier conversation with your tax professional using the terms “contribute” and “convert,” since that's all that's happening.

Basically, high income earners can't contribute to a Roth IRA. This backdoor technique allows them to.

Now let's talk about exactly how a backdoor Roth IRA works.

How Does a Backdoor Roth IRA Work?

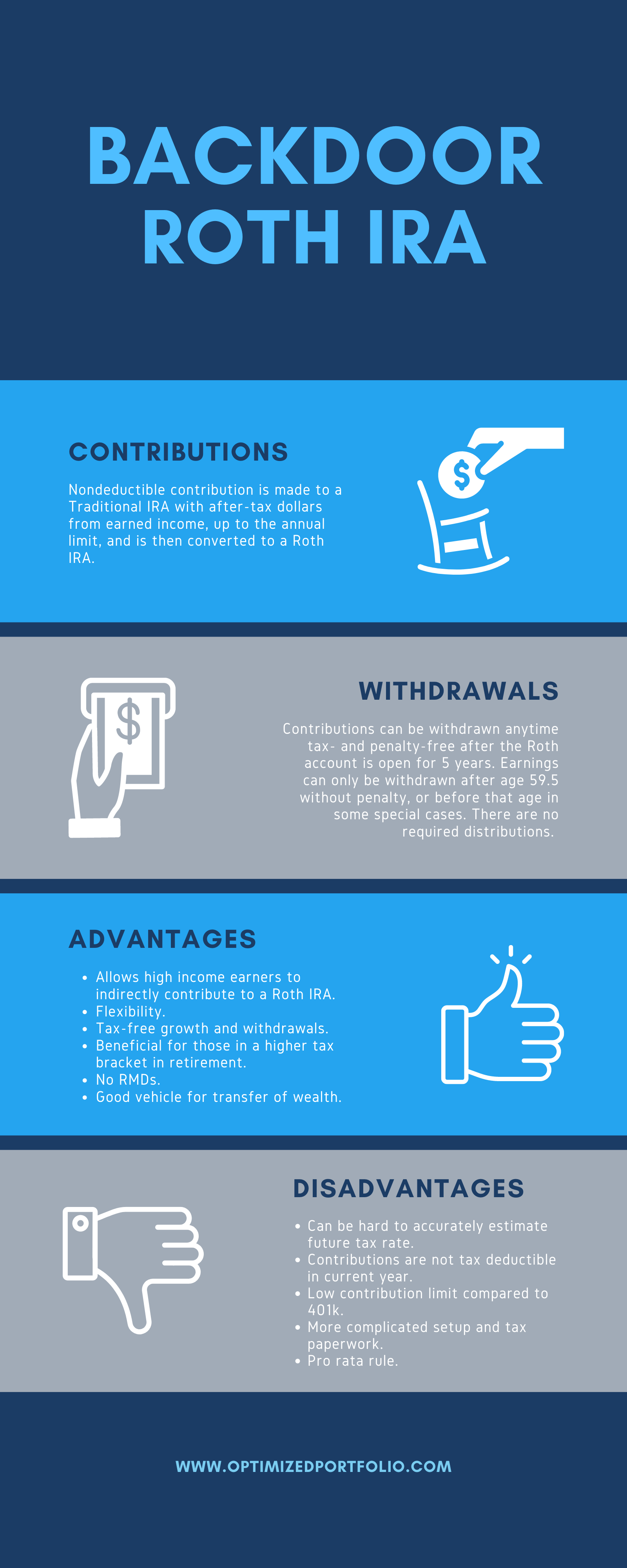

The backdoor Roth IRA works by making a nondeductible after-tax contribution to a Traditional IRA and then converting that contribution to a Roth contribution after the fact. The reason this works is because there is no income limit to open a Traditional IRA account.

Afterward, the investor will have an empty Traditional IRA account and a funded Roth IRA account. The Traditional IRA wrapper can stay open year to year and spend most of its time with a zero balance. The investor can then go buy securities inside the Roth IRA. I'd suggest index funds.

It's worth noting at this point that the word “nondeductible” refers to the contribution, not the account. There is no such thing as a “nondeductible Traditional IRA” account.

Remember that contribution is made with post-tax dollars and cannot be deducted from taxable income. Because of this, there are no taxes due at conversion. However, if any of the funds in the Traditional IRA that you want to convert weren't taxed already, you will owe taxes on them at the time of conversion.

For example, if there's $1,000 of pre-tax contributions in a Traditional IRA and $3,000 in nondeductible after-tax contributions, and you roll over the entire $4,000 into a Roth IRA, you'll owe taxes on that $1,000 and no taxes on the $3,000.

You'll also obviously owe taxes on any earnings that have occurred in the time between the contribution and the conversion. Those deductible contributions and earnings will be taxed as ordinary income and may even kick you into a higher tax bracket.

As such, hopefully you can see that the simplest approach is to make one single nondeductible cash contribution for the year, don't buy any securities, and immediately convert that cash to a Roth IRA contribution. This massively simplifies the paperwork come tax time.

I'll put it another way to stress the importance of this point. If you have any earnings before conversion, no matter how small, it greatly complicates the tax paperwork.

As an aside, you can roll over an entire Traditional IRA to a Roth IRA at once if you want, even if its amount is greater than the annual contribution limit.

Speaking of which, next we have to briefly cover a very specific and important rule called the pro rata rule.

Backdoor Roth IRA Pro Rata Rule

Users of the backdoor Roth IRA technique should be aware of the pro rata rule, a rule from the IRS which, in this context, states that if the investor has other Traditional IRA accounts, any conversion will be considered as if it came proportionately from all Traditional IRA accounts. This means that if you have multiple Traditional IRA accounts, the conversion will be taxed proportionately based on the ratio of pre-tax to after-tax dollars across all those accounts holistically, not just the one you are converting.

Essentially, if you've already got a Traditional IRA, SEP IRA, SIMPLE IRA, or rollover IRA, you'd want those to be zero before doing a backdoor Roth IRA, as being forced to pay taxes via the pro rata rule negates a lot of the benefits of the backdoor Roth IRA technique.

The best way to do this would probably be to roll those over into your 401k if you have one, as the 401k is not included in the pro rata calculation. This could also be a Solo 401k if you're self-employed. The next best way would be to convert them all to a Roth IRA in one fell swoop as mentioned earlier. If the IRA balance is relatively small, I'd probably just do the latter.

Next we'll talk about who the backdoor Roth IRA is ideal for.

Who Is a Backdoor Roth IRA For?

Remember the Roth IRA has income limits of around $150,000 for single investors. Above that, you're not eligible to open one. Period.

This investor can still open a Traditional IRA, but they can't deduct any of the contributions from their taxable income. Thus, the backdoor Roth IRA technique allows this high-income investor to convert that nondeductible Traditional IRA contribution to a Roth IRA.

Simply put, the backdoor Roth IRA is for the high income earner who still wants the characteristics of a Roth IRA. We'll go over those specific characteristics and why they might be appealing in the next section.

Why Is a Backdoor Roth IRA Useful?

So we just discussed how the backdoor Roth IRA technique is ideal for a high income earner. But why would this person want to convert to a Roth IRA in the first place?

Recall from my deep dive on the Roth IRA that the main function of the account is that contributions are allowed to grow tax-free and later be withdrawn in retirement tax-free. This is great if the investor expects to be in a higher tax bracket in retirement, or if you simply believe tax rates will increase significantly in the future.

Also remember that Roth IRA contributions in this case can be withdrawn anytime for any reason tax- and penalty-free after 5 years (because technically they're considered converted funds and not contributions in this case), and earnings can be withdrawn anytime after age 59.5. There are also special cases that allow for the early withdrawal of earnings without penalty, including:

- First time home purchase; you can withdraw up to $10,000.

- Higher education expenses

- Medical expenses

- Death

- Disability

- Substantially equal periodic payments

Consult your tax professional if any of those apply to you.

Roth IRAs also do not have required minimum distributions, or RMDs, like 401k's and Traditional IRAs do. This makes it a great wealth transfer vehicle because your heirs can withdraw tax-free. You can withdraw as much or as little as you want during your lifetime. The lack of RMDs also arguably saves you time, effort, and headache in retirement when gathering records and preparing taxes.

For all these reasons, the Roth IRA has arguably the greatest flexibility of all retirement accounts available to American citizens, and is thus also particularly useful for those hoping to retire early, such as the FIRE (Financial Independence Retire Early) movement.

Also note that you can have a Roth IRA in addition to an employer-sponsored plan (ESP) like a 401k. Doing so would also diversify your tax treatment.

Backdoor Roth IRA Tax Form 8606

Speaking of taxes, you'll be looking at an extra form at tax time for a backdoor Roth IRA: IRS Form 8606

This form is for nondeductible Traditional IRA contributions. Specifically, it's calculating any taxes owed on the conversion, which, if you do things right, should be zero.

Make sure your tax professional is familiar with this form; I've heard it's screwed up often.

Backdoor Roth IRA Investments

Just like with a Traditional IRA, if you've used the backdoor Roth IRA technique to convert to a Roth, you have a wide variety of investment choices including mutual funds, Exchange Traded Funds (ETFs), stocks, bonds, money market funds, certificates of deposit (CDs), cryptocurrency, and more. You can even hold investment real estate in a Roth IRA.

Backdoor Roth IRA Deadlines

In terms of deadlines, IRA contributions for the current year must be made before tax day of the following year, so April 15 for most folks. The Roth conversion can happen anytime – you can do it the same day as the contribution or wait days, months, or even years, though I wouldn't recommend waiting, for the reasons discussed earlier.

Most savvy investors like myself try to max out their annual IRA contributions in the first week of January each year since we know investing a lump sum all at once beats dollar cost averaging on average.

Backdoor Roth IRA Income and Contribution Limits

It's worth going over the income limits for the Roth IRA to know whether or not you need to do a backdoor Roth IRA. To be clear, these are limits under which you'll be eligible for a “regular” Roth IRA. Above these limits, you'll need to do the backdoor conversion. These limits typically change every year so the numbers here may be outdated depending on when you're seeing this.

Eligibility to contribute to a Roth IRA is determined by your Modified Adjusted Gross Income, or MAGI for short:

| Rules | Limit |

|---|---|

| 2023 Contribution Limits | $6,500; $7,500 if age 50 or older. |

| 2024 Contribution Limits | $7,000; $8,000 if age 50 or older. |

| 2023 Income Limits – Single | $153,000; phase-out begins at $138,000. |

| 2024 Income Limits – Single | $161,000; phase-out begins at $146,000. |

| 2023 Income Limits – Married Filing Jointly | $228,000; phase-out begins at $218,000. |

| 2024 Income Limits – Married Filing Jointly | $240,000; phase-out begins at $230,000. |

Backdoor Roth IRA Benefits Infographic

To recap the main benefits of using the backdoor Roth IRA technique, here's an infographic:

How To Do a Backdoor Roth IRA – Steps

Let's recap the exact steps for how to do a backdoor Roth IRA:

- Open a Traditional IRA account with a broker. More on this one in a sec below. This is your IRA custodian.

- Make a single nondeductible contribution to that Traditional IRA for the year. Do not try to deduct this contribution on your 1040 tax return later. Leave this deposit as cash; do not buy any securities.

- Immediately request the broker to convert that nondeductible contribution to a Roth IRA. The broker may ask you to also open a Roth IRA account on your own first if you don't already have one, or they may do that for you as part of the conversion process.

- Once the conversion is complete (usually within several business days), you will now have a funded Roth IRA account and an empty Traditional IRA account. Keep both accounts open to repeat the process next year. You can now go buy investments (stocks, bonds, ETFs, etc.) inside the Roth IRA once the cash has settled.

- Correctly fill out IRS Form 8606 at tax time.

Most brokerages like Schwab, Fidelity, Vanguard, etc. offer both Traditional and Roth IRAs, thus you should be able to do the backdoor Roth IRA technique at any of them. That said, some may be more cumbersome than others. If you've already got accounts at a brokerage, contact to ask them about their mechanics regarding backdoor Roth IRA conversions.

Some brokers specifically advertise and have dedicated instructions and protocols in place for the backdoor Roth IRA technique. One such broker happens to be my choice which is M1 Finance. The broker has automatic deposits and withdrawals, a sleek mobile app, and dynamic rebalancing of new deposits, among other things. I wrote a comprehensive review of the platform here.

Backdoor Roth IRA FAQ's

There seems to be speculation every year that the backdoor Roth IRA will be eliminated or “go away.” We can't know this ahead of time, so it's best to use it while we've got it. If it is indeed eliminated, you'll still own your Traditional IRA and your Roth IRA.

Is the backdoor Roth IRA legal?

Yes, the backdoor Roth IRA is legal. In fact, the IRS has explicitly given the technique its blessing.

Is the backdoor Roth IRA allowed in 2022?

Yes, the backdoor Roth IRA is allowed in 2022, provided you comply with applicable tax laws. Consult your tax professional at tax time to make sure things go smoothly.

Is the backdoor Roth IRA allowed in 2023?

Yes, the backdoor Roth IRA is allowed in 2023, provided you comply with applicable tax laws. Consult your tax professional at tax time to make sure things go smoothly.

When did the backdoor Roth IRA start?

Technically the backdoor Roth IRA with the establishment of the Roth IRA via the Taxpayer Relief Act of 1997. The strategy has been around for a long time but has become more popular in recent years as more people have become aware of it.

Are backdoor Roth IRA contributions taxable?

Yes, backdoor Roth IRA contributions are made with after-tax dollars.

Why does the backdoor Roth IRA exist?

Simply put, the backdoor Roth IRA exists because the IRS allows for the conversion of nondeductible Traditional IRA contributions to Roth contributions irrespective of income.

It is useful because it allows high income earners who would otherwise be ineligible for a Roth IRA to contribute to one indirectly.

Can you withdraw backdoor Roth IRA contributions?

Yes, you can withdraw backdoor Roth IRA contributions provided the account has been open for at least 5 years.

What about the Step Transaction Doctrine?

There used to be a questionable concern related to the backdoor Roth IRA about an IRS judicial principle called the Step Transaction Doctrine, which basically says if the constituent steps of a particular process were invalid or illegal and so close together to obviously be a premeditated plan, then the integrated result – in this case the backdoor Roth IRA technique – is also rendered invalid or illegal, and vice versa.

Thankfully, we no longer need to worry about that. The IRS clarified in 2018 that they're fine with the backdoor Roth IRA technique and that we don't need to wait between the initial contribution step and the conversion step.

Do you utilize the backdoor Roth IRA? Are you thinking about using it after reading this blog post? Let me know in the comments.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Leave a Reply