The Traditional IRA explained. This is a guide for the U.S. tax-deferred individual retirement account. Here we'll explore what a Traditional IRA is, who they're for, when to contribute, and where, why, and how to open one.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

Video

Prefer video? Watch it below. If not, keep scrolling to keep reading.

What Is a Traditional IRA?

A Traditional IRA is simply a U.S. retirement savings vehicle by which investors contribute pre-tax income, that money grows tax-deferred, and the withdrawals later in retirement are taxed as ordinary income.

The Traditional IRA was established in 1974 by the Employee Retirement Income Security Act. IRA stands for individual retirement account. As the name suggests, this is an account designed to help individuals save for retirement.

Who Can Contribute To a Traditional IRA?

Whereas an account like a 401k is tied to your employer, anyone with earned income below the can open a Traditional IRA on their own. Contributions may be tax-deductible depending on your income. We'll cover income limits later.

How Does a Traditional IRA Work?

The main function of the Traditional IRA is that contributions are made with pre-tax dollars (in most cases they are tax-deductible), those contributions are allowed to grow tax-deferred, and withdrawals later in retirement are taxed as ordinary income. In other words, contributions to a Traditional IRA are taxed on the back end and not on the front end.

Those contributions must be made in cash. There are limits imposed by the IRS for the amount of annual contributions that can be made to a Traditional IRA. We'll go over these contribution limits in a bit.

Traditional IRAs have what are called required minimum distributions, or RMDs. This means you have to start withdrawing after age 73 whether or not you actually need that money. This is because Uncle Sam wants to collect on his tax revenue that you've avoided up to that point.

Accountholders can start withdrawing without penalty at age 59.5. Withdrawals before that age will incur a 10% penalty plus taxes.

There are also special cases that allow for the early withdrawal of earnings without penalty, including:

- First time home purchase; you can withdraw up to $10,000.

- Higher education expenses

- Medical expenses

- Death

- Disability

- Substantially equal periodic payments

Consult your tax professional if any of those apply to you.

Also note that you can open a Traditional IRA in addition to an employer-sponsored plan (ESP) like a 401k. But having an ESP reduces the amount the IRS allows you to contribute to a Traditional IRA. If you leave an employer, you'll also usually have to roll over your 401k into a Traditional IRA.

Traditional IRA Investments

You have a wide variety of things you can invest in inside a Traditional IRA, including mutual funds, ETFs (Exchange Traded Funds), stocks, bonds, money market funds, certificates of deposit (CDs), cryptocurrency, and more. You can even hold investment real estate in a Traditional IRA.

When To Contribute To a Traditional IRA

A Traditional IRA can be created anytime, but contributions for the current year must be made by the owner's tax deadline, which is typically April 15 of the following year.

For those contributing every year to save for retirement, remember that the evidence indicates that on average it is advantageous to get money in the market as soon as possible, which is why savvy investors try to max out their annual contribution as soon as possible each year around January 1.

Note that contributions must come from earned income, which could include wages, salaries, commissions, bonuses, and business income (if self-employed). The following sources are not eligible:

- rental income

- interest income

- pension income

- annuity income

- stock dividends

- capital gains

Traditional IRA Income and Contribution Limits

Now we'll cover the income and contribution limits for a Traditional IRA. Note that these typically change every year so the numbers here may be outdated depending on when you're seeing this.

Eligibility to make tax-deductible contributions to a Traditional IRA is determined by your Modified Adjusted Gross Income, or MAGI for short, and your tax filing status. If eligible, you can deduct contributions whether or not you itemize deductions on your tax return.

If your income is too high, nondeductible contributions can still be valuable because that money is allowed to grow tax-deferred. If your income is so high that you're also ineligible to contribute to a Roth IRA, you can do a technique called the “Backdoor Roth IRA” where you convert that nondeductible Traditional IRA contribution to a Roth IRA contribution .

At this time in 2024, the annual contribution limit for individuals for a Traditional IRA is $7,000 if below age 50 and $8,000 if age 50 or older, up from $6,500 and $7,500 respectively for 2023.

The current annual income limits to be eligible to deduct Traditional IRA contributions in 2024 are $87,000 if single and $143,000 if married filing jointly. Phase-outs for reduced deductions begin at $77,000 if single and $123,000 if married filing jointly.

Also note that your Traditional IRA contribution cannot exceed the income you earned for that year.

Here's a recap of those limits in a table:

| Rules | Limits |

|---|---|

| 2023 Contribution Limits | $6,500; $7,500 if age 50 or older. |

| 2024 Contribution Limits | $7,000; $8,000 if age 50 or older. |

| 2023 Income Limits – Single | No deduction above $83,000; phase-out begins at $73,000. |

| 2024 Income Limits – Single | No deduction above $87,000; phase-out begins at $77,000. |

| 2023 Income Limits – Married Filing Jointly | No deduction above $136,000; phase-out begins at $116,000. |

| 2024 Income Limits – Married Filing Jointly | No deduction above $143,000; phase-out begins at $123,000. |

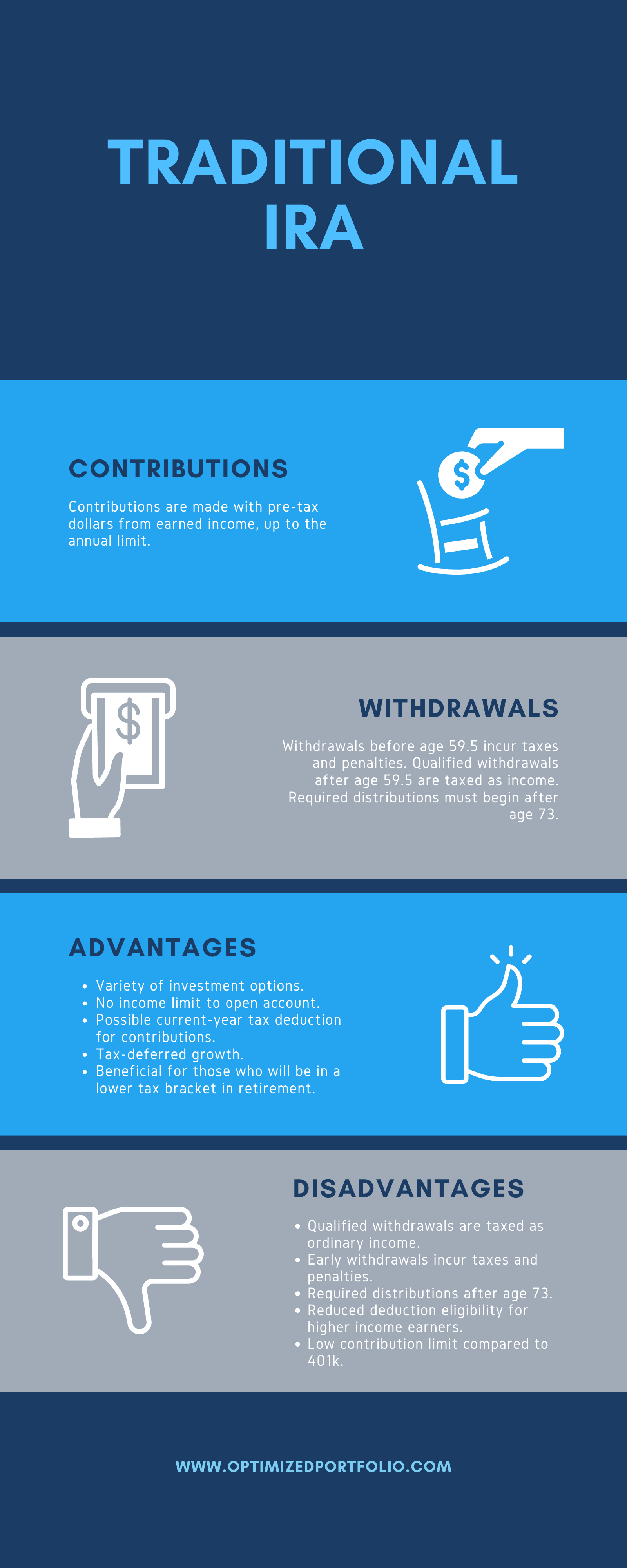

Traditional IRA Infographic

To recap, here's an infographic with the main characteristics of note of a Traditional IRA:

How To Open a Traditional IRA

Most brokerages like Schwab, Fidelity, Vanguard, etc. offer both Traditional IRAs. You'll just choose which one you want when opening a new account. My choice is M1 Finance. The broker has automatic deposits and withdrawals, a sleek mobile app, and dynamic rebalancing of new deposits, among other things. I wrote a comprehensive review of the platform here.

Traditional IRA FAQ's

There is no “best” Traditional IRA. The account structure and functions are universal regardless of provider; a Traditional IRA at Vanguard is the same as a Traditional IRA at Fidelity. My choice of broker is M1 Finance. Note, however, that your investment options may be limited to things like CDs if you open an IRA at a traditional bank.

Is Traditional IRA tax deductible?

Contributions to a Traditional IRA are usually tax deductible, depending on income level and tax filing status. Traditional IRA withdrawals are taxed as income.

Does Traditional IRA have income limits?

There are no income limits to open a Traditional IRA, however there are income limits that determine eligibility to deduct Traditional IRA contributions from taxable income.

Is Traditional IRA pre tax?

Yes, Traditional IRA contributions are considered pre-tax because they are tax-deductible in most cases.

Can Traditional IRA contributions be deducted from taxes.

Yes, in most cases Traditional IRA contributions can be deducted from taxes. Eligibility is determined by your income level and tax filing status.

Can Traditional IRA transfer to beneficiaries at death?

Yes, a Traditional IRA can transfer to beneficiaries at death, but note that withdrawals from the account will still be taxed as income.

Can Traditional IRA be converted to Roth?

Yes, you can convert a Traditional IRA to a Roth IRA, but note that you'll pay taxes on all the previous contributions in doing so, as those contributions.

Will Traditional IRA go up?

Whether or not your Traditional IRA goes up in value is going to depend on the assets you've invested in. We expect investments like stocks and bonds to have positive returns over the long term, though of course this is not guaranteed.

Will Traditional IRA go away?

The Traditional IRA will probably not go away, at least not anytime soon. It is the only individual retirement account that is tax-exempt.

Does Traditional IRA reduce taxable income?

Yes, in most cases. Traditional IRA contributions are usually tax-deductible. This is determined by your income level and tax filing status.

Can Traditional IRA be used for college?

Technically, yes. There are special cases for withdrawing early from a Traditional IRA without penalty, one of which is higher education expenses. Consult your tax professional on your specific situation.

Does Traditional IRA have RMDs?

Yes, Traditional IRAs do have RMDs, or required minimum distributions, that must start after age 73.

Are Traditional IRA contributions tax deductible?

Yes, in most cases. Traditional IRA contributions are usually tax-deductible. This is determined by your income level and tax filing status.

Are Traditional IRA distributions taxable?

Yes. Because Traditional IRA contributions are not taxed on the front end, distributions on the back end are taxed as income.

Who can open a Traditional IRA?

Anyone with earned income can open a Traditional IRA.

What Traditional IRA should I invest in?

Most modern brokers offer Traditional IRAs. My choice is M1 Finance. You get to choose what products to invest in inside the Traditional IRA account.

Can Traditional IRA lose money?

This will depend on what investments you've bought inside your Traditional IRA. We expect assets like stocks and bonds to have positive returns over the long term, but this is not guaranteed, and these investments can easily lose money over the short term.

Can Traditional IRA be inherited?

Yes. Note, though, that withdrawals will still be taxed.

How does a Traditional IRA grow?

Your Traditional IRA account value grows based on whatever growth occurs with the investments you choose inside the account.

How is a Traditional IRA taxed?

Traditional IRA contributions are usually tax-deductible. Growth inside the account is tax-deferred and distributions are taxed as income.

When is a Traditional IRA started?

There is no age requirement for opening a Traditional IRA. Anyone in the U.S. with earned income can open one.

When does a Traditional IRA make sense?

A Traditional IRA makes the most sense when you know for sure that your tax rate when withdrawing in retirement will be lower than your current tax rate while contributing.

When do you make Traditional IRA withdrawals?

Qualified withdrawals can be made from a Traditional IRA after age 59.5. Annual withdrawals are required after age 73.

Why is a Traditional IRA better than a Roth IRA?

A Traditional IRA is not objectively better than a Roth IRA. Whether or not it is better is entirely situational. The Traditional IRA is the better choice when your tax rate in retirement will be lower than your current tax rate. A Roth IRA also has a little more flexibility in terms of withdrawing contributions anytime and not requiring distributions. I compared the Roth IRA and Traditional IRA in more detail here.

Do you have a Traditional IRA? Are you thinking about opening one? Let me know in the comments.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Leave a Reply