VIG is a popular dividend ETF from Vanguard to capture U.S. dividend growth stocks. But is it a good investment? I review it here.

First, note that I don't chase dividends. But of course many investors prefer to use dividends to supplement their current income, particularly in retirement. Others just prefer dividend-paying stocks because it feels good. I even designed a dividend-focused portfolio for income investors that utilizes VIG.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

VIG Methodology, Dividend Yield, and Fees

VIG is the Vanguard Dividend Appreciation ETF. It launched in 2006. Since that time, it has amassed over $65 billion in assets.

The fund's name does not mean that it “appreciates” dividends in the sense that it's thankful for them. This ETF captures dividend growth stocks, companies with a historically increasing dividend. That is, these companies have a dividend that has appreciated over time.

Top 10 holdings include household names like Johnson & Johnson, Microsoft, Home Depot, and Coca-Cola.

VIG tracks the S&P U.S. Dividend Growers Index. These are U.S. stocks with a growing dividend over at least the past decade (10 consecutive years). The fund shaves off the top 25% highest yielding stocks from its selection universe, as high yield is sometimes a sign of an unstable company. Holdings are market cap weighted and are capped at 4%.

At the time of writing, VIG has 291 holdings, a dividend yield of 1.96% and an expense ratio of 0.06%.

Since it excludes REITs, this certainly isn't the highest yielding fund out there, but it should be one of the more reliable ones.

VIG Sector Composition

Note how VIG tilts toward sectors famous for dividends like Consumer Staples and Financials, and basically excludes Energy stocks and REITs.

| Sector | Weight |

|---|---|

| Basic Materials | 4.8% |

| Consumer Staples | 13.5% |

| Consumer Discretionary | 9.4% |

| Financials | 15.1% |

| Healthcare | 15.9% |

| Industrials | 13.5% |

| Energy | 0.1% |

| Technology | 22.6% |

| Telecommmunications | 1.7% |

| Utilities | 3.4% |

| Real Estate | 0.0% |

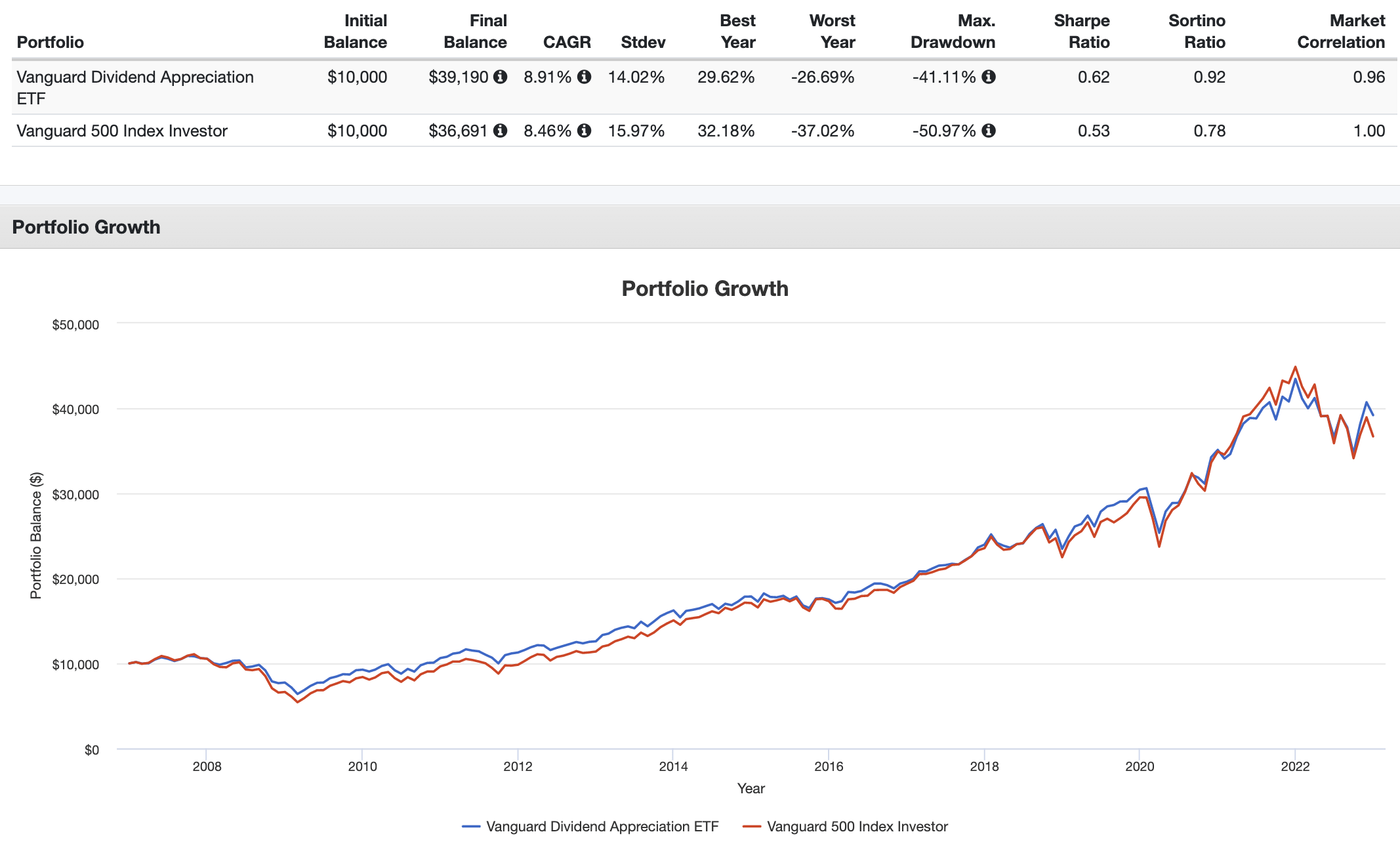

VIG Performance

Going back to 2006 when VIG launched and looking through 2022, it has beaten the S&P 500 on both a general and risk-adjusted basis, with lower volatility and a smaller max drawdown:

Is VIG a Good Investment?

So is VIG a good investment? Maybe.

In terms of factor exposure, VIG provides appreciable exposure to both the Profitability and Investment factors. I delved into factors in a separate post here. As I've noted elsewhere, the historical success of dividend investing as a whole is largely rooted in these factor premia.

VIG also happens to be one of the cheapest dividend funds out there with a fee of 0.06%.

As I said earlier, VIG is certainly not the highest yielding dividend fund out there, but it is an efficient and effective way to capture large, high-quality companies with strong profitability that are able to grow their dividend year after year. If a company fails to meet that requirement, it is dropped from the fund.

These companies typically have wide economic moats, meaning a competitive advantage over competitors that protects its long-term profitability and market share. While we might expect these to be Value stocks, VIG actually slightly tilts Growth.

Because of all this, I made VIG a component in the dividend portfolio I designed for income investors.

Conveniently, VIG should be available at any major broker, including M1 Finance, which is the one I'm usually suggesting around here.

What do you think of VIG? Let me know in the comments.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Leave a Reply