The COWZ ETF from Pacer seeks to hold “cash cows” – US large cap stocks with higher free cash flow yield. I review it here.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

COWZ ETF Overview

For any kind of reliable stability within stocks, we probably want to invest in a company that is profitable, meaning its revenue is greater than its expenses. Some perhaps don't realize that the famous S&P 500 Index for US large cap stocks already has this fundamental criterion for inclusion.

But what if we could go one step further and focus in on those US large cap stocks with higher-than-average profitability? Doing so might give our equities position more stability and lower volatility, particularly during bear markets.

Enter the COWZ ETF from Pacer. It's called the Pacer U.S. Cash Cows 100 ETF. As the name suggests, this ETF aims to narrow in on 100 US large cap stocks that exhibit higher cash flow and earnings than their peers, calling these particular stocks “cash cows.” In investing speak, we would call these “high quality” stocks.

Why would we be interested in these stocks in the first place?

Well, as I just hinted at, stocks with higher earnings are likely to be more resilient during tough times, and likely have comparatively greater free cash flow to return capital to shareholders in the form of dividends. We would specifically say these stocks as a group would be expected to have lower volatility, which is variability of return, compared to the broader market.

This just means this basket of stocks would be expected to not fluctuate up and down as much, potentially resulting in a smoother ride. This would obviously benefit investors like retirees who are using their investment portfolio for regular income to cover expenses, or those who simply have a lower tolerance for risk and are looking to attempt to mitigate major drops.

For factor investors like myself, COWZ would also be a way to specifically target the Profitability factor, denoted RmW for “Robust minus Weak,” in a portfolio that may otherwise be lacking.

Now let's look at how exactly the COWZ ETF achieves such exposure by analyzing its selection methodology.

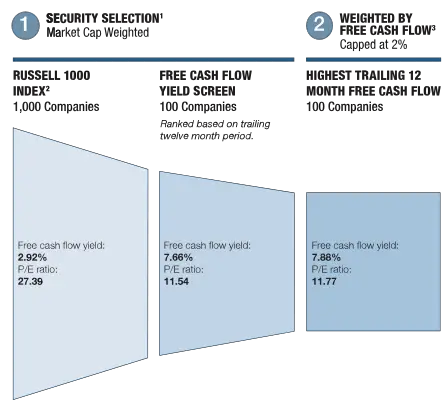

The fund starts with the Russell 1000 Index as its selection universe, which is a broad index of US large cap stocks comprising over 90% of the total US stock market by weight. It then screens for projected free cash flow and earnings for the next 2 years. COWZ then ranks and weights that subset from greatest to least trailing 12-month free cash flow yield and picks the top 100 stocks on that list for inclusion. Free cash flow yield is the ratio of free cash flow to enterprise value, so we're still screening for Value. This resulting index, the Pacer US Cash Cows 100 Index, caps individual holdings at 2% and is rebalanced quarterly. Top holdings include names like CVS, Chevron, and Exxon.

Pacer themselves maintain that Value strategies are flawed, or at least suboptimal, without also screening for free cash flow. They suggest that the traditional idea of simply looking at a valuation ratio like price-to-book alone is no longer a viable strategy due to the intangible assets of modern companies versus the tangible assets of companies a half century ago when the Value premium was alive and well. The evidence seems to indicate this idea of considering earnings is probably a prudent idea, particularly in smaller stocks, which their newer sister CALF covers.

This approach has proved attractive, and the COWZ ETF has certainly been a “cash cow” itself for Pacer, with the fund now boasting over $22 billion in assets after launching in late 2016.

Let me reiterate once again that these are Value stocks. We could find Growth stocks that exhibit higher-than-average earnings and cash flow, which is the first step in the selection process for this index, but then COWZ is again comparing that cash flow to the price of the stock and eliminating ones that are relatively expensive, which is effectively a Value screen. It's perhaps worth noting that this is very similar to how Warren Buffett invests. If for some reason you wanted to mimic his investing thesis without directly buying Berkshire Hathaway, COWZ may be a very good proxy.

Unsurprisingly, this selection methodology of COWZ results in positive loadings across all 5 factors in the Fama-French 5-Factor Model – Beta, Size, Value, Profitability, and Investment. This makes sense, as again these tend to be more conservative, established, blue chip large caps with robust earnings that don't reinvest aggressively into R&D. In doing the research for this post, I realized I had cavalierly mentioned this factor exposure in a Reddit thread over a year ago but did not delve too far into the details of the fund at the time.

Though of course, it's also important to note that this selection process currently results in COWZ massively overweighting Energy stocks and massively underweighting technology stocks, the latter of which have soared in recent years. At one point recently, the Energy sector comprised about 1/3 of the fund. Of course this hasn't always been the case, but before Energy, it was Industrials. COWZ investors who don't look too intently under the hood may be disappointed to learn that at this time, the entirety of FAANG, for example – Meta (Facebook), Apple, Amazon, Netflix, and Google – are completely absent from the fund, for better or worse. While I tilt Value myself, I also wouldn't want to entirely avoid large cap growth stocks.

It should also be no surprise that COWZ has a higher dividend yield than the market by about 25%, which may be of interest to dividend investors.

COWZ ETF Performance

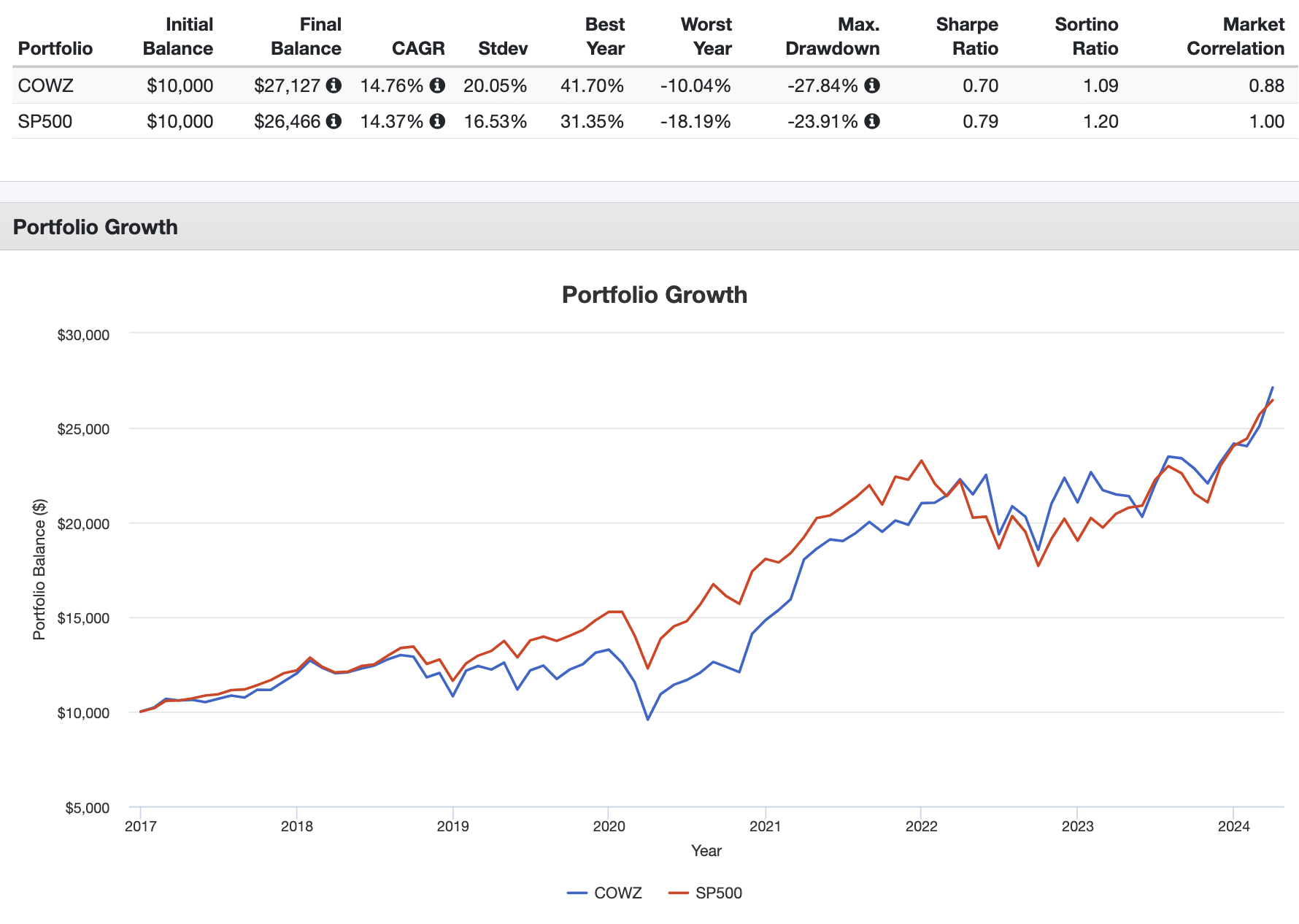

So how has COWZ delivered on its promises so far in terms of performance? Here's a backtest comparing it to the S&P 500 going back to COWZ's inception in 2016:

It has ever so slightly beaten the market over this time period, but seemingly almost entirely due to it massively outperforming in 2022 alone when cash was king and the broader market slowly bled out. Interestingly though, notice how its volatility and max drawdown have actually been greater than the market, resulting in a lower risk-adjusted return as measured by Sharpe and Sortino. This is perhaps due to the fund's sector weightings over time; remember this fund is only holding 100 stocks at the end of the day.

Also recall what I noted earlier about COWZ possibly being more appropriate for risk-averse investors; this has not been the case so far. In fairness, it's perhaps worth noting that if we zoom out a bit and look at the worst year metric, COWZ finished the year down 10% compared to 18% for the broader market, though even this statistic is a bit misleading. The worst year for COWZ was 2018. The worst year in this period for the market was 2022. In 2018 when COWZ was down 10%, the market was down only 5%. This is illustrated by the imperfect correlation of the annualized return of COWZ versus the market of “only” 0.80.

Is COWZ a Good Investment?

So is COWZ a good investment? Probably not.

Now seems like a good time to get to how much COWZ costs. Its expense ratio is 0.49%, which I think is pretty pricey for what you're getting here in a handful of relatively simple earnings and cash flow screens. These days, in the same price range or even sometimes cheaper, we've got multi-asset, option overlay, and levered funds – and sometimes combinations thereof – that are far more complex. There's nothing really special or proprietary going on with COWZ in my opinion, though admittedly I also can't really speak to how much other fund providers are specifically focusing on free cash flow yield as a primary indicator in their methodologies. My hunch is that it is not as much of a golden goose as Pacer make it out to be, but I could be wrong.

In other words, this fund just seems objectively expensive. It would be one thing if the fund provided global equities exposure wherein there's maybe an argument for the higher trading costs in Emerging Markets. But here we're just talking about US large caps, which are the cheapest stocks to trade. I would have expected the fee to come in at no more than half of what it is.

In fairness, Pacer's target audience is not retail investors, but rather financial advisors who are going to be buying their products for clients, so advisors may be less sensitive to these fees than they perhaps should be. This is a win-win for Pacer and advisors, as Pacer gets revenue and advisors get to use unique and specific marketing materials with clients surrounding the potential merits of free cash flow yield. This arguably comes at a cost to the clients, though, who are paying more in fees and commissions. Only time will tell if COWZ is able to deliver outsized returns that make up for its higher fee.

We also saw that COWZ hasn't really delivered on some of its purported merits so far. But maybe you still want the non-trivial factor exposure it provides in one fell swoop. But then seasoned factor investors should be aware that we've now got a plethora of more focused factor funds, such as those from Avantis, that deliver comparable and arguably superior exposure at about half the price. I'm the first to admit that fees are relative to what you're paying for, and I'd prefer this fund's approach over an indiscriminate Value screen, but again I see no objective reason to pay this much for what COWZ is providing.

A few examples that come to mind for comparable exposure would be AVLV from Avantis, SCHD from Schwab, or even the pretty naive VYM dividend fund from Vanguard, all of which are significantly cheaper and probably more tax-efficient as well. This is likely a marketing choice, but COWZ seems like both an inefficient dividend fund that doesn't want to call itself a dividend fund, and an inefficient factor fund that doesn't want to call itself a factor fund.

As I hinted at earlier, I'd also submit that COWZ is not really suitable as a core holding, with its comparatively small basket of 100 large cap stocks from one single country and some pretty lopsided sector weights. I'd probably prefer if the selection methodology went one step further and capped sector weights to avoid such concentration.

Further, recognize that COWZ is constantly churning stocks. If you're a stock picker, you may have some picks that you plan to hold forever. COWZ is basically doing the opposite. Every quarter, the fund is re-evaluating its holdings and doing quite a bit of buying and selling. Not only is this unfavorable from a tax perspective like I already mentioned, but this also means COWZ very rarely holds on to any particular stock for more than about a year.

In fact, on average, 90% of its holdings are overturned within any given 12-month period! For this reason, as we might expect, COWZ has negative loading on the Momentum factor, as it's constantly trimming the winners over pretty short time periods.

I'll be curious to see how COWZ performs over the long term going forward if the Value premium makes a strong comeback. Pacer have marketed free cash flow yield as their unique selling proposition. If it ends up somehow being the holy grail indicator of higher returns over the next 20+ years, I'll write about it. Until then, I don't see myself paying half a percent for it.

Conveniently, COWZ should be available at any major broker, including M1 Finance, which is the one I'm usually suggesting around here.

Make sure you use COWZ with a Z. There is also a COWS with an S that is a different fund.

What do you think of the COWZ ETF? Do you own it? Are you planning on buying it? Let me know in the comments.

Disclosure: None.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.