The CAOS ETF from Alpha Architect aims to address left tail risk during tumultuous periods of “chaos” in the stock market. I review it here and explore how CAOS does this and why you might want to consider it in your investment portfolio.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

Introduction – Tail Risk

To set the stage for a discussion of the CAOS ETF, let's first very briefly talk about tail risk to give you an idea of the particular circumstances this fund aims to address. I already have a dedicated blog post on tail risk here, so this section here in this post will just be a short high-level summary.

Essentially, tail risk refers to the risk of highly unlikely events, which we sometimes call “black swans.” We're specifically concerned with the left “tail” of the returns distribution, which is a negative event that impacts the portfolio, a quintessential familiar example of which is a sudden and severe stock market crash like we saw in 2008.

By definition, left tail events are inherently rare and typically unpredictable, making them difficult to reliably address. Put simply, we're talking about the probability of a large loss in the portfolio outside the range of what we usually see.

To make matters worse, we as humans also tend to underestimate the likelihood of such extreme adverse events, which we call optimism bias. This is especially true of young, inexperienced investors with a high risk appetite.

As you might imagine, tail risk becomes more impactful as one's time horizon shortens, such as for the retiree who is withdrawing from the portfolio regularly, for whom a major market crash could be catastrophic, just as was the case for those hoping to enter retirement around 2008.

If you've been around this website long enough, you know I'm always a proponent of broad diversification within and across asset classes. The idea here in this context is to take that traditional diversification concept one step further with a product to specifically address a particular circumstance.

So let's look at how the CAOS ETF can potentially do that.

CAOS ETF – Alpha Architect Tail Risk ETF

Investors with a low tolerance for risk and/or nearing retirement usually utilize treasury bonds to attempt to address such tail risk in their portfolios alongside stocks, and that is a perfectly sensible and valid idea, but admittedly that “crisis alpha” of treasury bonds is not 100% guaranteed. Here, specific to CAOS, we're taking it one step further and utilizing derivatives like put options to further insulate the portfolio against such extreme adverse events. In the words of the creator Wes Gray from Alpha Architect, portfolios should be “robust to chaos,” hence the ticker.

Let's specifically look at how the CAOS ETF works.

Principal Strategy – Tail Risk Hedging

CAOS is primarily buying derivatives called put options on the famous S&P 500, which are options contracts that increase in value as the underlying index falls in value. In other words, they basically provides a constant inverse exposure to the stock market. As a brief reminder, put options give the buyer the right, but not the obligation, to sell the underlying at an agreed-upon strike price at or before expiration.

Think of this like an insurance policy. Just like you pay a monthly car insurance premium with the expectation of a large payout in the event of a major car accident, here you pay a monthly premium in the form of the cost of the options contracts for a potentially large payoff in the event of a major stock market crash. The more severe the crash is, the higher the payoff of the put option is. We call this a convex payoff profile.

Now of course it's entirely possible that you go your entire life and never get in a car accident and never need to use your car insurance. But that doesn't mean you shouldn't buy car insurance. In the context of investing in financial markets, we would expect to see at least 3 major crashes over a 30-year period. The market does not just constantly and steadily go up.

In this context, these options contracts are specifically referred to as “protective puts,” as they aim to “protect” your long stocks exposure. The fund is rolling these contracts for you monthly so that you don't have to manually. We also refer to this specific strategy as tail hedging. CAOS aims to put 3-6% of its assets into this hedging strategy at any given time. Since the fund will capitalize on the profits of this option hedging strategy for you in the event of a severe market crash, this means you don't have to monitor and attempt to try to time the market, which tends to be more harmful than helpful. As an aside, Simplify similarly use such protective puts as a small part of their long equities fund SPD.

This general strategy of hedging tail risk isn't really new. Seasoned investors may recognize the overall idea as very similar to that of the appropriately named TAIL ETF from Meb Faber and Cambria, which launched in 2017. The differentiator is the unique, thoughtful, and innovative implementation from Wes Gray and the gang at Alpha Architect and the sub-advisor Arin Risk Advisors here with CAOS.

CAOS previously traded as a mutual fund under the ticker AVOLX starting in 2013 before converting to an ETF in 2023. Wes Gray of Alpha Architect actually owned AVOLX years ago and approached Arin Risk Advisors, who ran the fund, to see if they'd be up for converting it to the more tax-efficient ETF structure.

Mitigating Return Drag

Of course, the obvious next question is “Is this insurance policy worth the premium?”

We expect a big payout if the market crashes, but then we typically only see a major crash about every 7 years on average. The rest of the time while the market is just chugging along going up on average and not experiencing severe drops, we're still paying for that insurance every month, i.e. the cost of the options contracts. We might expect that the cost of ownership to outweigh the payoff benefit for the occasional crash. Such a scenario would be called negative carry, referring to the cost of the negative return of holding or carrying the hedge. We typically expect tail risk hedges – or really any insurance policy – to exhibit negative carry.

This is where the other collateral assets inside the CAOS ETF come into play as one of the aspects that makes this fund special.

First, CAOS is sometimes utilizing a strategy called short put spreads to get back some cash to offset the cost of the protective puts we talked about earlier. For the sake of brevity, I'm not going to get too in the weeds on this trade because this is not a post on options trading, but essentially it involves selling a put to receive a premium and then using that cash to buy a put with a lower strike price that is cheaper. Selling put spreads also provides a premium when the market is going up.

Next, CAOS is also holding another product from Alpha Architect themselves which is BOXX for effective Treasury-Bills-like exposure. As a reminder, Treasury Bills, or T-Bills for short, are ultra-short-term bonds from the U.S. government which are referred to as the “risk-free asset.”

I talked about BOXX in a separate blog post here. Essentially, it is achieving synthetic tax-efficient T-Bills-like exposure via its own options contracts on the S&P 500, for which the specific strategy is called a “box spread,” hence the name of the fund. For our purposes here, with some hand waving on the underlying box spread options trade, this basically means we're getting the return of T-Bills in a tax-efficient manner inside CAOS to further help offset the cost of the put options we discussed earlier. In fact, at this time, BOXX itself comprises roughly 60% of CAOS.

Ok, so we've clearly got a lot of various options trading going on under the hood. Let's zoom back out and summarize what's happening. All in all, we're basically collecting some cash monthly during “normal” market appreciation to offset the cost of the main purpose of the fund which is buying the protective puts as the tail risk hedge. This is a very important consideration, because it means far less performance drag during “normal” good times than would otherwise be expected if we were only rolling put options.

Video

At this point, you may be interested in an overview video from Alpha Architect themselves to reinforce everything we just went over. If not, keep scrolling to keep reading.

Tax Efficiency

Moreover, CAOS aims to deliver this hedge exposure as tax-efficiently as possible by minimizing distributions and using the ETF structure's benefits, which is important considering these types of trades and assets are typically not very tax-friendly. This means CAOS potentially gives us cost-effective downside protection for taxable space that previously didn't really exist!

Performance

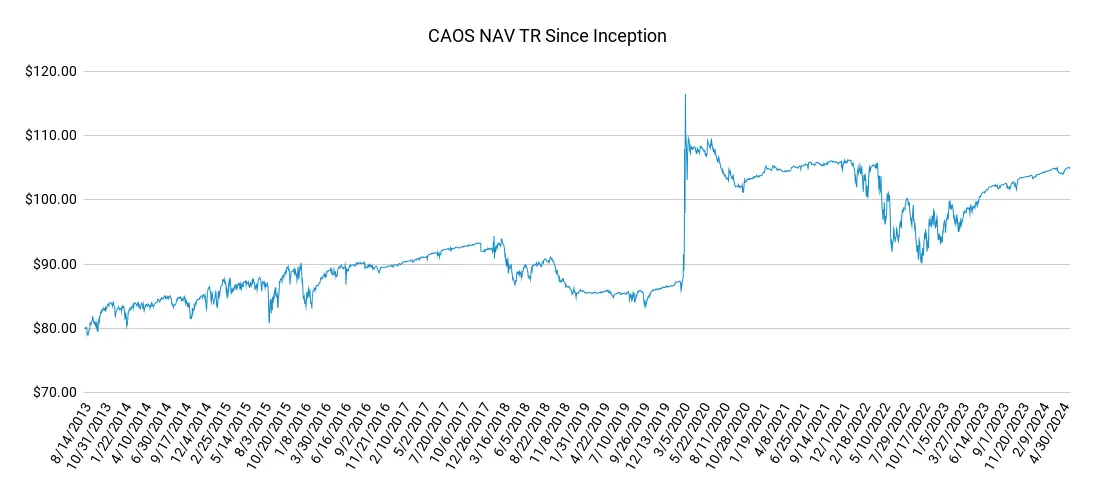

It makes little sense to judge the performance of CAOS on its own (because we'd be holding it alongside stocks), but impressively and perhaps counterintuitively, these cost-mitigating measures have allowed CAOS itself to deliver a positive return of about 30% over its lifetime since 2013, meaning it has actually had positive carry:

You can see in that chart that CAOS performed exactly as we'd hope for that March 2020 flash crash when it skyrocketed significantly by about 40%. This serves as a real-world example of the viability and utility of such a strategy and, in my opinion, inspires confidence in its incorporation into one's portfolio.

Further Specific Methodology Discussion

Let me also remind you, as I've noted several times already, that we expect CAOS to shine in a sudden, severe stock market crash, not in a flat or mild bear market. This is because CAOS is holding “out of the money” (OTM) put options, meaning the market really needs to move for them to pay out. These options are far cheaper than “in the money” (ITM) put options. For the experienced nerds here wanting specifics, CAOS targets a 30-60% out-of-the-money range on the SPX. This means that if the S&P 500 is trading at $10,000, CAOS would usually be holding put options with strikes from $7,000 down to $4,000.

Remember earlier how I referred to the convex payoff profile of these put options. If the market drops a lot very quickly, our put options get more and more valuable. Specifically, the ideal scenario for CAOS's OTM put options is a drawdown greater than 25% within a period of about 60 days, naturally accompanied by high market volatility. From the prospectus:

“The Fund’s three primary objectives are: (i) to gain a varying amount of market exposure to the Index; (ii) limit risk relative to a decline in the Index and profit from a market dislocation event; and (iii) generate a series of cash flows. The Sub-Adviser considers a market dislocation event (also known as a tail risk event) when the Index suffers an extreme market decline (generally greater than 25%) within a few months accompanied by a sustained increase in expected Index volatility (generally greater than 50).”

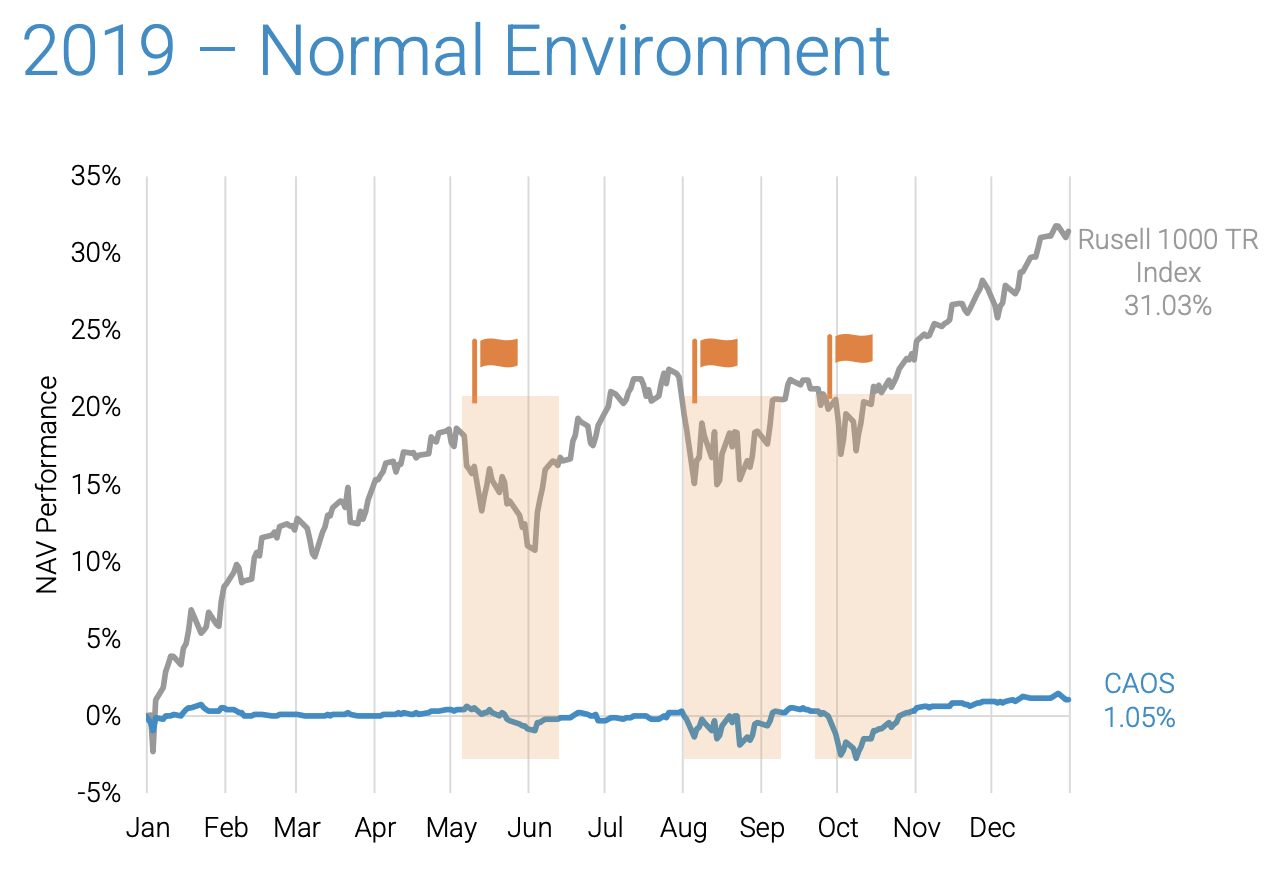

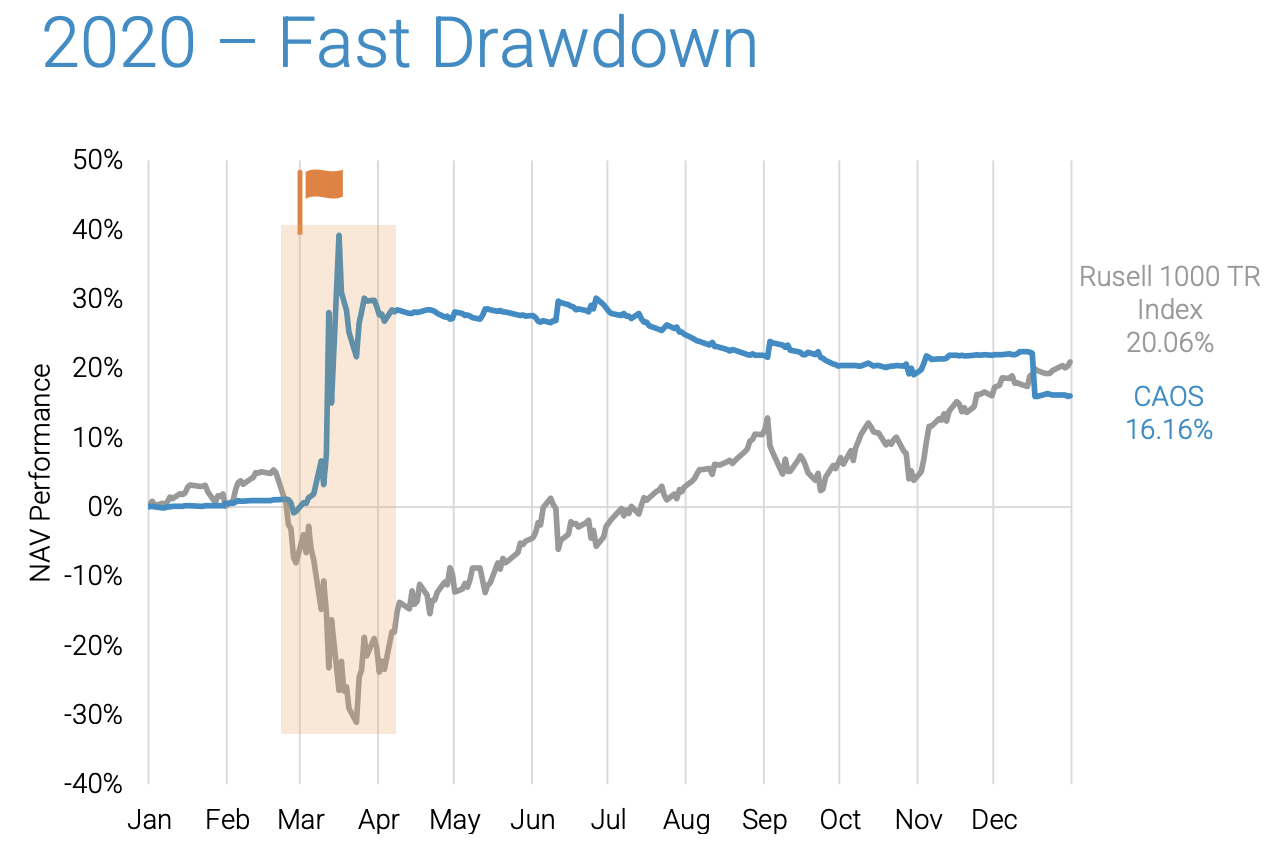

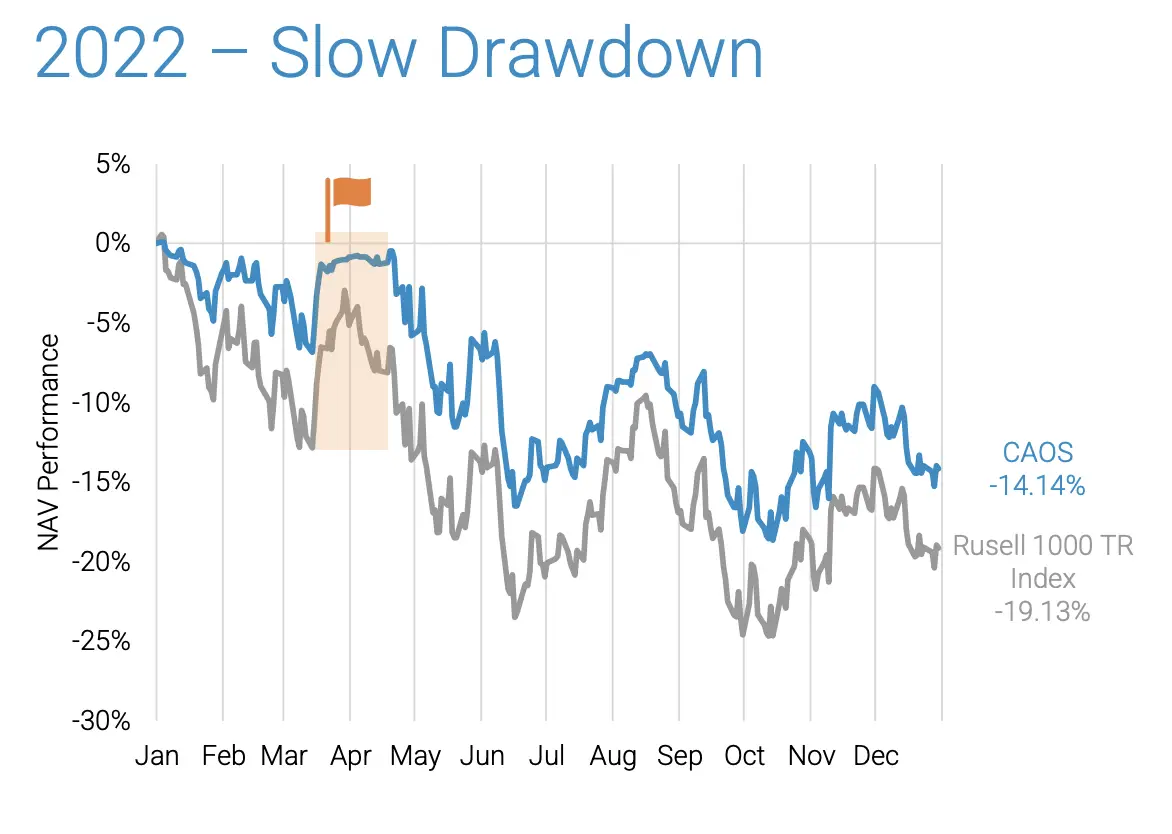

But if the market is just very gradually going down over a prolonged period, like we saw in 2022, for example, CAOS is not going to do much. It's worth noting though that this sort of market behavior is pretty rare. Again, think of CAOS as portfolio insurance for extreme events. Here's this idea visualized:

Here's the actual performance from 2019, 2020, and 2022 respectively illustrating these different scenarios. Click each individual image to enlarge.

In other words, the “success” of CAOS, if we want to call it that, depends entirely on the speed and severity with which the crash occurs. Again, think of the 2008 Global Financial Crisis and the March 2020 flash crash as examples of the type of fast and deep drawdowns we're attempting to address here.

Risk

This fund's strategy may sound intimidating and confusing for you, and you're probably curious about the tangible downside risk of this fund per se.

For those less familiar with the nature of put options, let me perhaps quell your fear a bit by pointing out that the maximum amount one can lose is the defined cost of the put option contracts. The fund does not have an unlimited loss potential. So no, you are not going to blow anything up by owning CAOS.

Technically, there are also specific nonzero risks like derivatives risk and counterparty risk, but going into detail on these is beyond the scope of this blog post. As usual, investors are encouraged to do their own due diligence.

Is CAOS a Good Investment?

Ok, so who should own CAOS? Should you buy it? Is it a good investment?

It's possible that you already own BOXX as a tax-efficient cash-equivalent investment but now you're also intrigued by the idea of downside protection with CAOS. In that case, instead of simply adding in CAOS, you might consider closing out your BOXX position before adding CAOS, because remember that CAOS itself holds BOXX inside it. And I don't mean that the individual holdings of BOXX are in CAOS. I mean the CAOS ETF literally holds the BOXX ETF.

As a hypothetical example to illustrate, let's say you have 6% of your portfolio in BOXX as a cash holding. You could achieve that same exposure to BOXX by instead holding 10% CAOS, which would be roughly 6% BOXX for the total portfolio, getting you that same cash exposure you already had. Granted, of course, the CAOS position in totality will not behave like a comparable BOXX position, for better or worse, so take that idea with a grain of salt.

In the interest of full disclosure, let me reiterate that while you're obviously not required to hold bonds alongside your stocks and while CAOS would arguably be expected to behave like treasury bonds at certain times, CAOS is not a 1:1 replacement for a bonds allocation. It is a specific, arguably esoteric tool with a very specific purpose. The tail risk hedge in this instance further diversifies the portfolio in the event that bonds don't come to the rescue in a stock market crash. Its purpose may or may not be desirable to you, depending on your personal circumstances like goals, time horizon, and risk profile.

At the same time, I would also remind you that most investors severely overestimate their tolerance for risk and underestimate the probability of catastrophic black swan events, so while many would probably disagree with me, I would argue that CAOS is not unsuitable for the young accumulator with a long time horizon. Many young investors who started in the last decade or so have not lived through a scenario like 2008 that would test one's emotional fortitude. Those who traded and sold in a panic during that time had worse portfolio outcomes and many were likely scared away from stocks for years thereafter, if not forever. I always say the best portfolio is the one you can stick with through good times and bad. In that sense, CAOS may prove useful even if only to provide peace of mind and let you sleep easier at night.

One could also argue that if you specifically seek crash protection for your long equities position, you can get by more efficiently with a lower allocation to CAOS compared to a higher allocation that would be required with traditional treasury bonds that would hopefully deliver “crisis alpha,” thereby providing a capital-efficient way to diversify your diversifiers. Thinking of CAOS this way may get you pondering ways to incorporate it into a “return stacking” strategy with leverage – wherein drawdowns are more damaging – with something like RSSB.

All that being said, I usually say investors should aim to fully understand what they're buying and why they're buying it, and I'll be the first to admit that is likely an unusually high hurdle here in this case with both CAOS and BOXX, especially for novices.

I'd also be remiss not to mention that tail risk hedging strategies are typically best used tactically, wherein you sell out of the tail risk hedge when it goes up to then take that insurance payout and buy more stocks while they're down, but of course that's market timing, which I usually don't condone, and that idea sounds much easier than it is in practice. Moreover, buy-and-hold index investors may not be checking their portfolios often enough to effectively time a crash.

Lastly, let's talk about fees. After a fee waiver of 0.07%, CAOS has a net expense ratio of 0.63%, which may seem high at first glance, but I think it's not unreasonable for all the options trading going on under the hood that we discussed earlier. The space of tail risk hedges and inverse exposure also typically carries higher fees.

CAOS ETF Model Portfolios

So how do you incorporate this thing in a real portfolio?

Again, think of CAOS as basically an insurance policy with a specific use case: tail risk hedging for rare and extreme events. Because of this, and because of the aforementioned convexity of OTM put options, we only need a dash of CAOS to exert its intended effect, regardless of what else is in the portfolio.

Before I throw around some numbers, let me preface by saying it's impossible to know or even test what might be an optimal allocation to a tail risk hedge like this because of its relatively narrow application and because of the inherent unpredictability of black swans. See the chart above with the March 2020 crash as an example to illustrate this fact. Future crashes may be larger in magnitude than any we've ever seen historically, or they may all be smaller than any we've seen in the past. We can only know what is optimal in hindsight.

I also want to say the following examples are purely hypothetical examples to illustrate the concept and are not actual recommendations. They are also just my opinion of how I might implement this product.

So all that being said, I think something around 5-10% CAOS in the portfolio is a reasonable allocation. We're basically giving up a small amount of space for that insurance policy in case things really hit the fan. I'd argue the percentage allocation is largely irrelevant to whatever else is in the portfolio, assuming there are at least some stocks in there, which is the long exposure we're aiming to protect in the first place.

For a hypothetical example to illustrate, let's assume a young investor with a long horizon is all in on global stocks with a total market index fund like VT from Vanguard. She is okay with usual market volatility but wants some protection against quick, extreme events. Thus, adding a tail risk hedge might look like 90% VT and 10% CAOS. To view this actual portfolio and invest it in using M1 Finance if you want to, click this link to do so. Obligatory reminder to do your own due diligence on whether or not such a strategy is suitable for you.

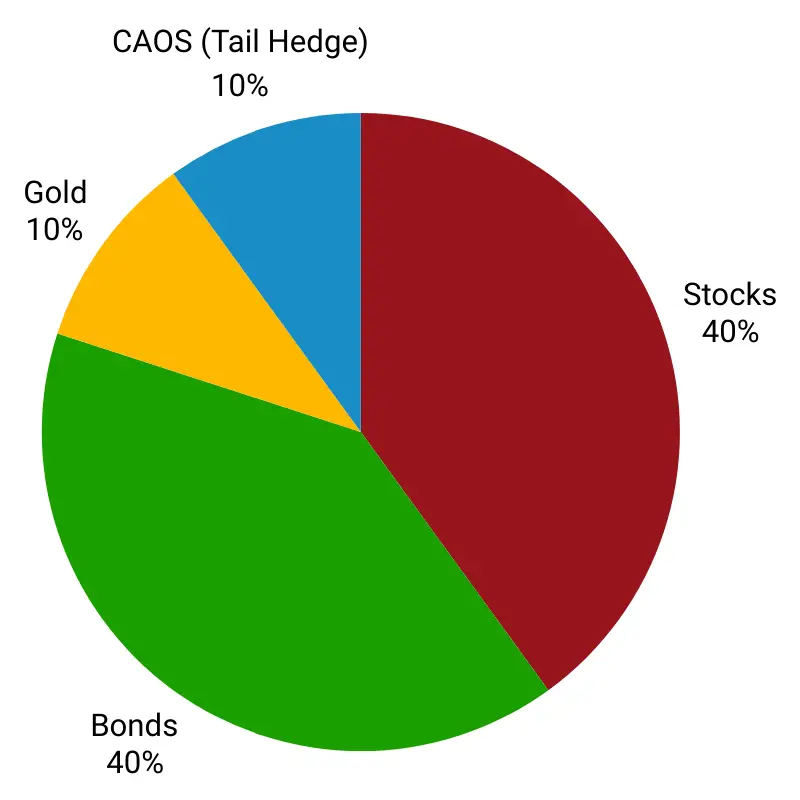

On the other end of the spectrum, a retiree may already have a well-diversified portfolio of stocks, bonds, and gold, but now they want to specifically add a tail risk hedging strategy. Let's say they have a pretty conservative hypothetical portfolio of 40% stocks, 50% bonds, and 10% gold. In this instance, because our tail hedge piece CAOS is likely going to be positively correlated with bonds on average, and because the stocks piece is what we're trying to protect in the first place, I would take space from the bonds allocation to result in:

40% stocks

40% bonds

10% gold

10% CAOS (tail risk hedge)

Using live funds from my “best in class” ETFs list, this hypothetical model portfolio might look like this:

40% VT

40% SCHR

10% GLDM

10% CAOS

To view this actual portfolio and invest it in using M1 Finance if you want to, click this link to do so. Obligatory reminder to do your own due diligence on whether or not such a strategy is suitable for you.

I'm not at all trying to sound self-important, but since you're sitting here reading this opinion piece on this website, at this point you're also probably wondering if I personally own the CAOS ETF. I can say that while I do not currently own CAOS, I am also not at all opposed to owning it. I currently still have a pretty long investing horizon, but I probably will incorporate CAOS in my own portfolio in 5-10 years.

Conveniently, CAOS should be available at any major broker, including M1 Finance, which is the one I'm usually suggesting around here.

What do you think of the CAOS ETF? Do you own it? Are you planning to buy it? Let me know in the comments.

Disclosure: I am long BOXX.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

The CAOS ETF was actually the AVOAX mutual fund during March 2020. Source: “Tail Hedging with the CAOS ETF”, Alpha Architect YouTube channel

This raises questions… Were there differences in strategy there between AVOAX and CAOS? Would the current CAOS strategy have perform identically to AVOAX during March 2020? Is a backtest even possible?