What if I told you there’s a way to get the risk-free return of T-bills but in a way that’s more tax-efficient than buying T-bills directly or buying a T-bills fund like SGOV? Here I review the BOXX ETF and why you might want to consider it over your favorite T-bills ETF or money market fund for your cash management needs.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

Video

Prefer video? Watch it below. If not, keep scrolling to keep reading.

Intro – Cash and T-Bills (and SGOV)

So for short-term cash-equivalent investments, which you’d use for an emergency fund or for a short-term goal, you’ve got a few pretty standard options like a high yield savings account, certificates of deposit, treasury bills or T-bills for short, and money market funds. These are all about as low as it gets on the risk scale and pay something close to what’s called the risk-free rate, defined as the 3-month Treasury Bill rate. At the time of writing, that rate is around a very appreciable 5%, so these products have attracted more discussion and more investment recently.

The problem with all these is that you’re still taxed on that monthly interest or return because the IRS treats it as income, even if you’re just reinvesting it and letting that money grow inside the account. For example, if I earn $1,000 in interest throughout the year and I have a 22% marginal tax rate based on my income, I’m looking at a tax bill of $220 at the end of the year for that earned interest, even if I never withdrew and spent it. This scenario is actually what happened to me recently – and likely to many of you as well – with my favorite T-bills ETF SGOV.

And while obviously that interest is money you didn’t have previously so it’s all gravy even after taxes, I don’t know anyone who enjoys paying taxes, especially on money that’s not really being used for anything tangible.

But of course, that taxation is simply unavoidable, right? Well, maybe not anymore…

What Is BOXX?

Enter BOXX, an ETF from Alpha Architect that aims to deliver the risk and return profile of T-bills but in a more tax-efficient manner. Its full name is the Alpha Architect 1-3 Month Box ETF.

So how does it work?

First, recall that a fund like BIL or SGOV is holding plain vanilla T-bills straightforwardly and just rolling them. Nothing complicated or proprietary going on.

While it may sound counterintuitive, in attempting to resemble T-bills, BOXX doesn’t actually hold T-bills or any bonds at all. It uses highly liquid derivatives to synthetically extract a return resembling the risk-free rate. It does this specifically by simultaneously holding a synthetic long position and a synthetic short position on the S&P 500, and the difference in strike price between those should be close to the risk-free rate of return.

Here's a video overview of the fund from Alpha Architect themselves. Keep scrolling to keep reading.

How Does BOXX work? (Box Spreads)

This trade is known as a “box spread,” hence the name of the ETF.

If you’re reading this, chances are you’ve never even heard the term “box spread.” They’ve been around for a long time. Let’s look at how they work.

Specific to the S&P 500 Index, a box spread would consist of the following 4 option contracts:

- Long call on SPX

- Short call on SPX

- Long put on SPX

- Short put on SPX

We’ll use a hypothetical example from Alpha Architect themselves to illustrate how the trade works with these 4 contracts.

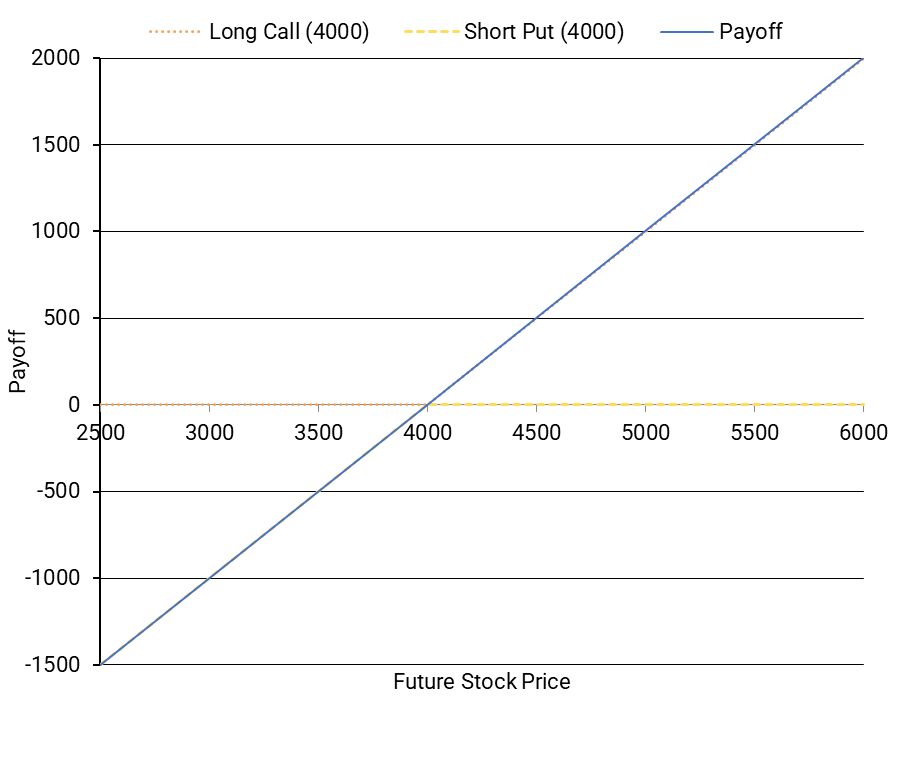

Suppose we buy a call and sell a put on the SPX (contracts 1 and 4 above) with the same 1-year expiration and the same strike price of $4,000.

Notice how the payoff profile in blue resembles that of a long stock position delivered one year from now – if the price goes above $4,000, you make money, and if the stock price goes below $4,000, you lose money.

This is effectively a replication of a stock future created using options, called a synthetic long position. These are also European options, so no early exercise risk.

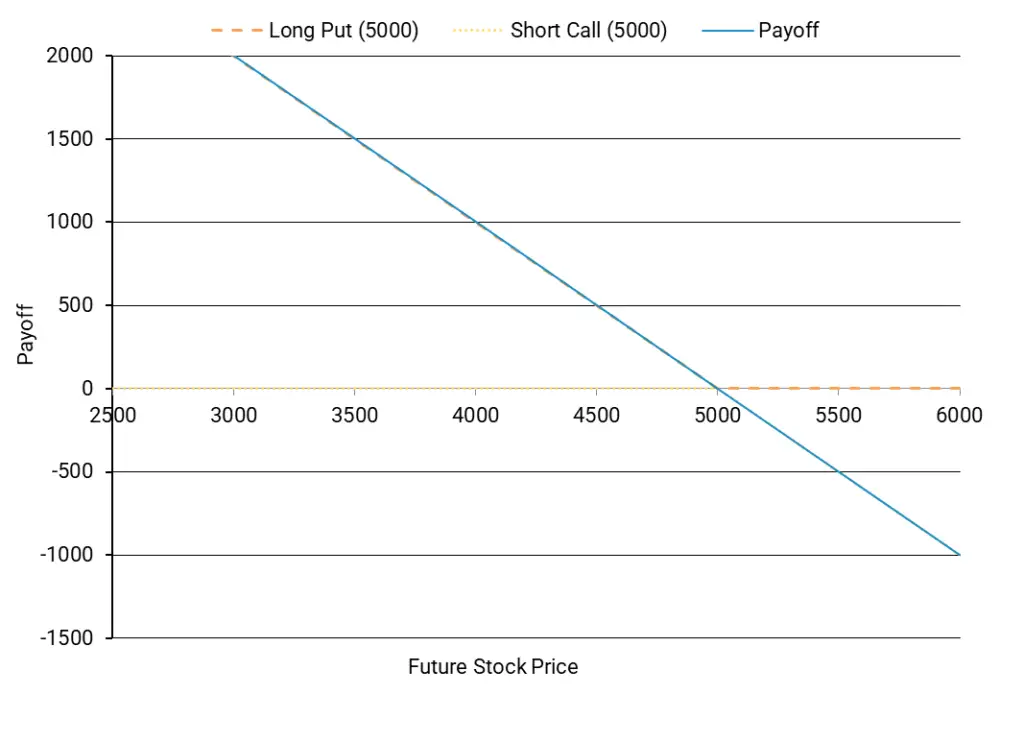

Now let’s look at another position using our other two contracts – buying a put and selling a call with the same strike price of $5,000 and an expiration one year from now.

Here’s what the payoff profile looks like for this position, effectively shorting the SPX, which we’d call a synthetic short. If the price goes below $5,000, we make money, and if the price goes above $5,000, we lose money.

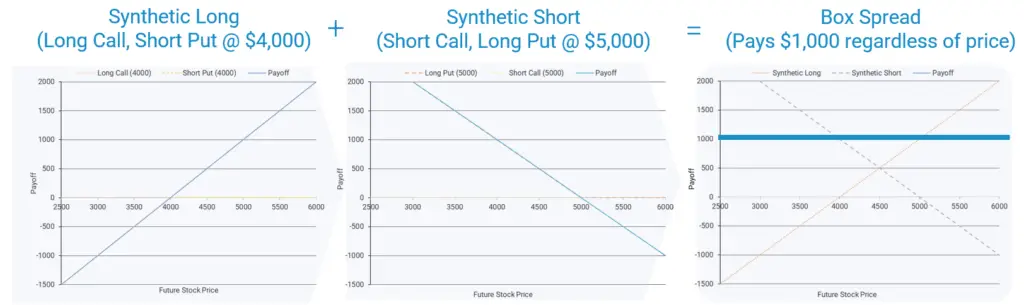

Combining these positions simultaneously effectively eliminates market risk and guarantees a payoff of the spread between the synthetic long and short positions, which is $1,000 in this case, and which is like the par value of a T-bill. Appreciate that this is not a mispricing arbitrage, but rather simply a natural byproduct of the way these contracts are correctly priced.

So we’re guaranteed to get $1,000 one year from now. How much does that $1,000 cost us today? The present value is likely an amount close to the future value of $1,000 discounted by the risk-free rate of 1-month T-bills. Again, using 5% as our implied rate, our hypothetical present value would be $1,000 divided by 1.05 which equals about $952.

Also realize that the price of the underlying index – the highly liquid S&P 500 in this case – and even the prices of the contracts themselves don't really matter that much for our purposes here. We're just concerned with the implied rate, which again is a T-bill-like interest rate, for effectively lending money in the options market.

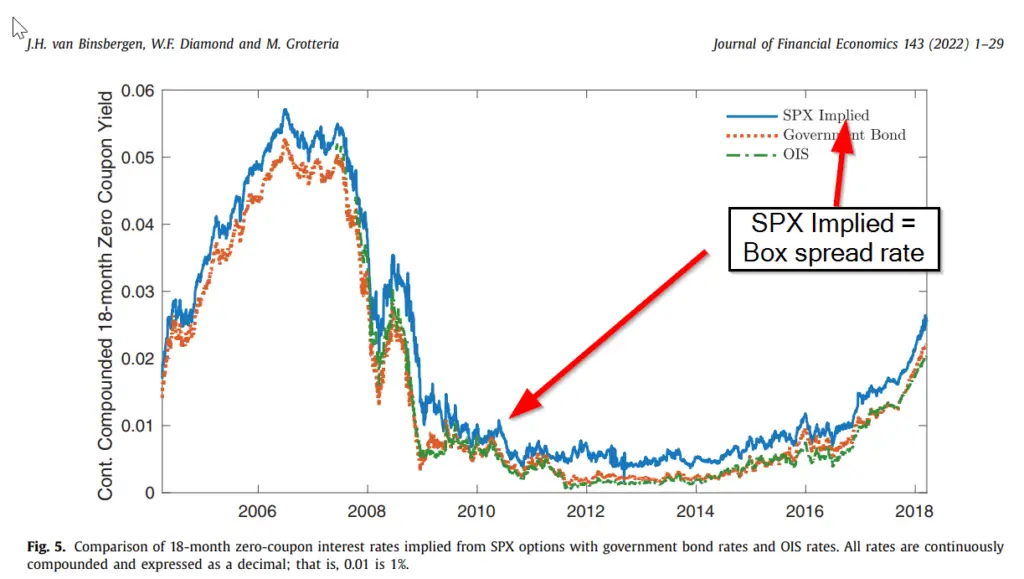

It’s worth noting that historically, box spread rates have always been higher than equivalent treasury bill rates, usually in the range of 0.25-0.35%, and we would expect that to continue, likely due to the comparatively greater risk of the former.

So now let’s talk about those risks…

Is BOXX Safe?

The primary question everyone asks is “Is BOXX safe?” What are the risks of this ETF?

Basically, we’re relying on the counterparty to pay on our options contracts. We call this counterparty risk.

The counterparty for U.S. Treasury Bills is obviously the U.S. government. The counterparty of box spreads is the Options Clearing Corporation, or OCC. While the former certainly sounds safer, S&P Global have actually given these two entities the same credit rating.

The OCC is considered a Systemically Important Financial Market Utility, or SIFMU, an entity whose survival is critical to the stability of the U.S. financial system due to their roles in the transfer, clearing, and settlement of payments and securities.

It’s also worth noting that the creditworthiness of the OCC has been tested throughout history, and the Fed would likely step in if anything went awry with the OCC (“too big to fail”), so for all intents and purposes, with some hand waving, OCC-backed options have similar counterparty risk to US government debt.

There's also nontrivial regulatory risk here surrounding tax treatment; I've got a whole section covering this below.

BOXX Tax Treatment

Now we get to the reason we’re all here in the first place: taxes!

So again, gains from treasury bills are taxed as ordinary income. That’s about as bad as it gets.

Taxation of box spreads is pretty complicated, but the gist is that options on indexes like the SPX are taxed as 60% long term capital gains and 40% short term capital gains, so we’re already coming out ahead, and then the ETF wrapper provides some additional benefits due to the unique creation and redemption process of the structure (specifically called in-kind redemptions). Put simply, BOXX is using an old tax loophole for ETFs in a new way.

In short, BOXX is able to defer distributions and carry forward capital losses of some of the options contracts, and distributions that do happen can be classified as capital gains. The fund was able to avoid distributions completely for 2023 and 2025.

Capital gains are not as friendly for those who live in states with high taxes like California, so the comparison becomes murkier, as T-bills are exempt from state taxes. I've included a calculator below for you to see how BOXX works for your personal scenario. Obligatory disclaimer to consult your tax professional on your specific circumstances.

The more tax-heavy your state is, the less BOXX's federal advantage matters, and above a certain state tax rate, a straightforward T-bills ETF like SGOV actually wins outright. For each federal bracket, here's the state income tax rate above which SGOV beats BOXX on a combined federal + state after-tax basis:

| Federal Bracket | Breakeven State Rate |

|---|---|

| 22% | ~4% |

| 24% | ~5% |

| 32% | ~10% |

| 35% | ~12% |

| 37% | ~10% |

This is why running your own personal numbers matters greatly here.

BOXX vs. SGOV

As a brief refresher, here's the quick comparison of BOXX vs. SGOV:

| BOXX | SGOV | |

|---|---|---|

| Full name | Alpha Architect 1-3 Month Box ETF | iShares 0-3 Month Treasury Bond ETF |

| Issuer | Alpha Architect / Arin Risk Advisors | BlackRock |

| Strategy | Box spreads on SPY (synthetic T-bill equivalent) | Direct ownership of 0-3 month U.S. T-bills |

| Expense Ratio | 0.19% | 0.09% |

| Federal tax treatment | Long-term capital gains (if held ≥1 year) | Ordinary income |

| State tax treatment | Subject to state capital gains tax | Exempt from state and local taxes |

| Distributions | Near-zero; return via NAV appreciation | Monthly |

| AUM | ~$11B | ~$84B |

But we're primarily concerned with that after-tax return…

After-Tax Return Calculator

Because that aforementioned state tax rate consideration is highly personal, I decided to make a calculator to illustrate BOXX's advantage or lack thereof for specific scenarios.

Remember, both BOXX and a T-bills ETF like SGOV target a yield in the neighborhood of the risk-free rate, but they get there differently, and the IRS treats them very differently. (I'm using SGOV as the example here for comparison purely because it's a very popular T-bills fund.)

BOXX uses box spreads to defer gains and target long-term capital gains treatment. SGOV holds actual T-bills and pays ordinary income monthly. This calculator focuses primarily on the tax dimension of that difference. (Note that the same comparison would apply to a money market fund like SPAXX, for example, for which distributions are taxed as ordinary income.)

One additional nuance to keep in mind, again, is that box spreads have historically earned a ~0.25-0.35% premium above T-bill yields – a “convenience yield” that exists because Treasuries carry unique liquidity and safe-haven demand that box spreads don't fully replicate. By default, this calculator ignores that premium for a cleaner apples-to-apples tax comparison, but you can toggle it on below to see the combined effect.

SGOV distributions are exempt from state income tax, because they're Treasury interest. BOXX capital gains are subject to state tax. This narrows BOXX's advantage significantly in high-tax states, and in some cases flips the outcome entirely. The breakeven state tax rate below shows exactly where that crossover happens for your inputs.

To state what may be obvious at this point, notice how BOXX's advantage widens as one's federal tax rate increases, but worsens as state tax rate increases, as again T-bills are exempt from state taxes. BOXX also obviously becomes increasingly advantageous as yield and holding period increase, as they allow for a higher total return and thus a wider gap.

Keep in mind the calculator below is showing projected hypothetical returns, not guaranteed or realized outcomes. It's also not tax advice; consult your tax professional.

BOXX Mechanism Change (to Heartbeat Trades)

In the interest of full disclosure, it's my understanding that BOXX's mechanism has actually changed a bit.

When BOXX launched in late 2022, it held SPX index options, as used in the example above. Also as noted above, SPX options are “Section 1256 contracts” under the tax code, which get an automatic 60% long-term / 40% short-term capital gains treatment regardless of how long you held them, which beats ordinary income.

But SPX options are cash-settled, so they can't be physically delivered to an authorized participant (AP) during the ETF creation/redemption process, meaning the standard ETF mechanism for flushing unrealized gains out of the fund couldn't be used. To compensate, Alpha Architect layered in a Booking Holdings (BKNG) stock straddle overlay designed to generate offsetting capital losses inside the fund.

In August 2024, that strategy seemed to hit a snag. Under the straddle rules of IRC Section 1092, losses from offsetting positions must be deferred, not immediately recognized. The result was BOXX's first-ever distribution on August 13, 2024 – $0.29 per share of capital gains – which surprised quite a few people who believed the fund would never distribute anything. Still pretty small, but nonzero nonetheless.

In fairness, Alpha Architect never claimed to always be able to always avoid distributions, so this was only a major surprise if you didn't fully understand what you were buying, which of course is quite possible and even likely with many people who owned BOXX.

Alpha Architect responded by pivoting to options on SPY (and occasionally QQQ), which are equity options rather than index options. Equity options can be physically delivered to APs in the creation/redemption process. This unlocks the standard ETF tax efficiency tool known as the “heartbeat trade,” governed by IRC Section 852(b)(6): when a RIC distributes appreciated property in-kind to a redeeming shareholder, the fund doesn't recognize that gain.

The practical result is BOXX's in-the-money option legs get distributed out to APs in redemption baskets, flushing accumulated gains without tax recognition at the fund level. The fund sells the out-of-the-money legs at a loss, booking capital losses. Ideally, your return thus accumulates entirely in NAV appreciation, not taxable distributions. And since all legs of a box spread are European-style (only exercisable at expiration), there's no early exercise risk that could disrupt the structure.

In layman terms, the hypothetical ideal net result for investors, assuming the current strategy holds, is you owe nothing until you sell your BOXX shares, at which point your gain is a long-term capital gain (if held over one year) taxed at a max federal rate of 20%. No monthly 1099-INT events, no annual capital gains distributions.

Is BOXX Worth It?

So is BOXX worth it? Maybe.

BOXX makes more sense if:

- You're a high-tax-bracket investor in a low- or no-income-tax state, holding cash in a taxable brokerage account for at least a year. This is the core use case the fund was designed for.

- You have large capital loss carryforwards sitting around. BOXX gains are capital gains, which offset accumulated losses. If you've been tax loss harvesting aggressively and have a stockpile you've been carrying forward, BOXX gains effectively cost you nothing in taxes.

- You're parking cash for an intermediate period and don't need monthly income. Unlike something like SGOV, which distributes monthly and generates a 1099-INT every January, BOXX just appreciates quietly.

BOXX makes less sense if:

- You're holding it in a tax-advantaged account (IRA, 401k, HSA). The box spread premium may still allow BOXX to beat T-bills pre-tax, but the tax efficiency advantage – the whole point of the fund – goes out the window here.

- Your holding period is under one year. Gains realized in under twelve months are short-term capital gains, which are taxed at ordinary income rates.

- You live in a high-tax state like California, New York, or New Jersey and are in a moderate federal bracket. As shown above, the state tax math can flip entirely against BOXX in these states for most bracket combinations. Do the calculation for your specific situation before assuming BOXX wins.

- You're income-oriented. BOXX intentionally aims to pay no distributions.

- You can't stomach regulatory uncertainty. The tax treatment isn't court-approved or IRS-blessed. If the prospect of a mid-stream rule change that retroactively affects your tax situation gives you pause, BOXX may not be for you.

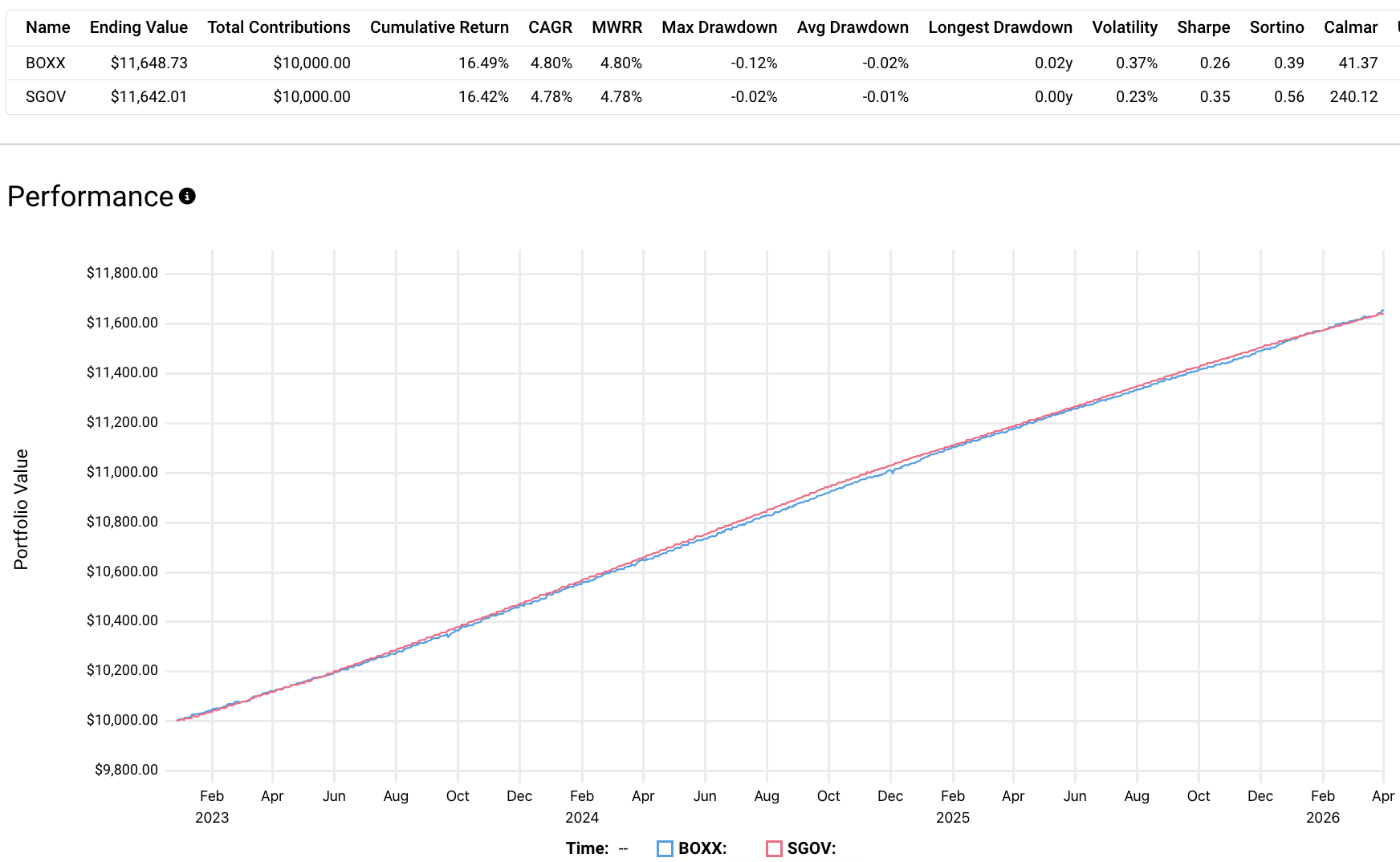

BOXX ETF Performance and Fees

At this point you’re probably thinking, okay, this all sounds nice in theory, but execution is another thing altogether. How has this thing actually performed in the real world?

As explained, the case for BOXX is fundamentally an after-tax story, which makes pre-tax return comparisons somewhat beside the point, but we can still look at them.

In its short lifespan thus far, BOXX has actually outperformed SGOV, even after its slightly higher fee of 0.19% and before taxes.

It’s worth noting that a fee waiver of 0.05% is in place for this fund, so it’s possible its net expense ratio might increase from 0.19% to 0.24% at some point, but my armchair estimation is that the box spread premium plus the tax savings would still outweigh that higher fee. Only time will tell.

Is BOXX Legal?

You'll find no shortage of speculative fearmongering articles out there on the potential detrimental impact of the IRS taking a closer look at what BOXX is doing, so I figured I'd add this section to be comprehensive here and at least inform people of the opinions out there on the nontrivial regulatory risk.

BOXX is legal, fully operational, has north of $10 billion in assets, and the IRS has not taken any action against it as of April 2026. But if you're the type of investor who actually reads fund documents (a habit I encourage), you'll notice BOXX's own prospectus dedicates substantial real estate to warning you that the tax treatment might not survive a legal challenge. That level of disclosure doesn't mean the fund is doing something wrong, but it does mean this is a calculated bet, not a guarantee, as I've tried to mention throughout this post.

The central legal concern is IRC Section 1258, the so-called anti-conversion statute. It recharacterizes capital gains as ordinary income when: (a) substantially all of a transaction's expected return comes from the time value of money (which a box spread obviously does — it's literally a synthetic loan), and (b) the transaction is either a straddle under Section 1092(c), or is marketed as producing capital gains from a time-value return.

BOXX's promotional materials prominently highlight capital gains treatment as the fund's core selling point. That potentially satisfies prong (b). The box spread structure's four offsetting legs fit the straddle definition under Section 1092(c), potentially satisfying prong (a). The fund's SAI acknowledges this directly:

“The Fund has received guidance from tax counsel regarding section 1258 of the Code and its applicability to the current investment strategy of the Fund, but such guidance is not necessarily persuasive or binding on the IRS.”

Several tax scholars have weighed in on this:

Daniel J. Hemel (NYU Law School) published “The Tax Trap Inside the BOXX” in Tax Notes Federal (March 2024). His conclusion was that the IRS would likely succeed in recharacterizing BOXX's gains as ordinary income under Section 1258, box spreads meet the straddle definition, and BOXX's marketing satisfies the conversion transaction marketing prong.

Steven Rosenthal (Tax Policy Center) published “Tax Gimmick in a BOXX” (March 2024). Rosenthal helped draft Section 1258 in 1993 as a Joint Committee on Taxation staffer. His view is: BOXX “violates both the letter and the spirit of the anti-conversion statute,” and Treasury could close the loophole quickly via regulation under Section 1258(c)(2)(D) without waiting for Congress.

Mark Leeds (Mayer Brown LLP) analyzed why the switch from SPX to SPY options was necessary inTax Notes Federal in 2024, explaining the technical reason SPX options couldn't work with Section 852(b)(6)'s in-kind redemption mechanism.

BOXX's prospectus is clear on the downside scenario: if the IRS successfully challenges the fund's tax position, BOXX could fail to qualify as a RIC, meaning the fund itself would pay corporate taxes and all distributions would be recharacterized as ordinary income for shareholders. The gains you deferred could become taxable in a way you didn't plan for, and depending on timing, you could find yourself with penalties for underreported income.

The prospectus also notes that if an IRS ruling applied retroactively, the fund could owe “deficiency dividends” and penalties for prior years' incorrect information reporting.

So all that sounds pretty scary, but let's take a deep breath and zoom out for a sec. The IRS has had years and billions of dollars of evidence to look at, and they haven't acted. At $10+ billion, BOXX is not exactly hiding. The most likely explanation is that the tax risk is real but the IRS has more important things to worry about, or is waiting for additional legal vehicles to challenge it.

BOXX is appropriate for investors who understand they're making a bet on a gray area of tax law, not exploiting a court-approved certainty. Size your position accordingly, document your basis carefully, and don't be surprised if the rules change mid-game. The fund itself is telling you this is possible.

Conclusion

Worst case is probably that the box spread premium and the fee cancel out, and we’re left with just the tax savings as the main benefit, but of course remember that’s the main reason we started looking at this fund in the first place. Cap gains over income and the deferral thereof are huge benefits for most people.

Savvy investors have wisened up to this idea, as BOXX now impressively boasts over $10 billion in assets after only a little over 3 years. I think it’s an incredibly clever, innovative product that provides retail investors access to institutional lending rates in an easy, low-cost, packaged solution that requires much less effort and intimidation than implementing a box spread on your own. Wes Gray and the Alpha Architect team spent 7 years figuring out this product.

In the interest of full disclosure, I moved my own cash into BOXX from T-bills (via SGOV), but I am in no way affiliated with Alpha Architect.

Conveniently, BOXX should be available at any major broker, including M1 Finance, which is the one I'm usually suggesting around here.

What do you think of the BOXX ETF? Do you own it? Are you planning on buying it? Let me know in the comments.

References

Alpha Architect – BOXX ETF fund page, prospectus, and box spread explainer materials. https://alphaarchitect.com/funds/boxx/

Van Binsbergen, J.H., Diamond, W., & Grotteria, M. (2022). “Risk-free interest rates.” Journal of Financial Economics, 143(1), 1-29. https://doi.org/10.1016/j.jfineco.2021.05.009

Federal Reserve Bank of New York, Liberty Street Economics – “Options for Calculating Risk-Free Rates.” October 2023. https://libertystreeteconomics.newyorkfed.org/2023/10/options-for-calculating-risk-free-rates/

CME Group – “Index Options Box Spreads as Financing Tool.” 2024. https://www.cmegroup.com/articles/2024/index-options-box-spreads-as-financing-tool.html

Options Industry Council / OCC – “Listed Options Box Spread Strategies for Borrowing or Lending Cash.” https://www.optionseducation.org/getmedia/2ae6c8bd-9a8e-4d2f-8168-19b6ff9e3589/listed-options-box-spread-strategies-for-borrowing-or-lending-cash.pdf

Internal Revenue Code Section 1256 — Tax treatment of regulated futures contracts and non-equity options. https://www.law.cornell.edu/uscode/text/26/1256

Disclosure: I own BOXX.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

California is one of the worst examples of tax benefits of BOXX for many. However, if you are in the 35% federal bracket and 15% capital gains bracket, the 20% federal tax savings outweighs the top California bracket. Extreme example though.

What do you think about the risk that the IRS taxes the fund as ordinary income instead of capital gains, as discussed in the tax risk section of Alpha Architect’s prospectus for BOXX? Looks like this might collapse into essentially a t bill fund with higher fees depending on that ruling

Could you use BOXX in place of a money market account for daily cash needs or would you need to hold it for at least a year to reap the benefits? Thanks. Love your site!

Great question. Comparatively less beneficial over the short term but still beneficial over MMF. Much greater benefit after a year.

Jon,

Ignore my previous question. I reread the article and found the answer. Thanks again.