A 529 account or “529 plan” is a tax-advantaged investment account to save for future education expenses. Here we'll look at what it is and where, why, and how to open one.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

What Is a 529 Account?

A 529 account, legally known as a “qualified tuition plan,” is named after section 529 of the IRS tax code. It is an investment account that allows for tax-advantaged growth to use for future education expenses.

While the less common Prepaid Tuition Plan is under the 529 umbrella, this article will focus on the much more common Education Savings Plan.

Purpose

A 529 account may be a good consideration for those wanting to save for college.

Even though 529 plans are governed by the IRS, they are operated by a state or educational institution, which is why options and tax benefits differ among states.

Qualified education expenses for which you can use 529 funds include tuition, fees, books, supplies, certain room and board costs, computer equipment, technology expenses, tutoring, and even student loan repayments.

While 529 accounts are often associated with college savings, they can also be used for eligible K-12 tuition expenses and apprenticeship programs as well.

Tax Benefits

The main benefit of a 529 account is federal tax savings. Growth inside the account is tax-deferred, and withdrawals for qualified education expenses are free from federal taxes and in many cases, state taxes as well.

In most states, there are also state tax benefits for 529 plan contributions, such as a state income tax deduction. Contributions are not deductible from federal income taxes.

Contribution Limits

Contribution limits vary among states, but are typically very high, in excess of $300,000.

There are no annual 529 plan contribution limits, but contributions greater than the annual gift tax exclusion ($17,000 in 2023) will count against your lifetime estate and gift tax exemption ($12.92 million in 2023).

Investment Options

529 plans typically offer a pretty limited menu of investment options that include index funds and target date funds to suit different risk tolerances and time horizons. Be sure to watch out for high fees, though.

How Does a 529 Account Work?

The 529 account is opened by the owner, usually a parent or guardian for the benefit of a child's future higher education expenses. The child is the beneficiary. You'll need the personal information of the beneficiary, including social security number, at the time of opening the account.

Anyone of any age with a Social Security number can be a beneficiary. The beneficiary can even be the same person who opens the account, meaning you can save for your own future education expenses.

Unlike a custodial account, the owner retains control of the account until all money is withdrawn and can change the beneficiary at any time, such as if the original one decides not to pursue higher education.

If the beneficiary wants to use 529 funds for anything other than qualified education expenses, they'll incur a 10% penalty and federal income taxes on the earnings portion of any withdrawals. There are a few exceptions for which this penalty is waived:

- If the beneficiary receives a tax-free scholarship.

- If the beneficiary attends a U.S. Military academy.

- If the beneficiary dies or becomes disabled.

There are no income restrictions on making contributions to a 529 plan.

To open the account, you must be a U.S. adult (18+) with a U.S. mailing address and Social Security number.

Most plans allow you to set up automatic recurring deposits from a linked bank account, or you can just invest whatever you want whenever you want.

A popular tactic is to make lump sum contributions around birthdays, holidays, or other occasions. 529 plans can also accept gift contributions from family and friends.

Most 529 plans allow you to distribute the payments directly to the account owner, the beneficiary, or the school.

Special Considerations for 529 Plans

529 plan owners and beneficiaries are not restricted to a plan from their home state, but you'll usually get greater tax benefits using your home state's plan. Compare the features, investment options, fees, and tax benefits of different state plans before choosing one. Hypothetically, you could be a North Carolina resident, invest in a New Hampshire 529 plan, and send your student to college in New Mexico.

When applying for need-based financial aid, 529 assets are considered parental assets. Since financial aid formulas typically assess parental assets at a lower rate compared to student assets, having a 529 account may have a smaller impact on eligibility for financial aid. However, distributions from a 529 plan count as student income, which can affect the following year's financial aid eligibility.

Due to the penalty and tax burden if 529 funds are not used for education expenses, if the beneficiary is unsure about higher education, it may make more sense to simply use a plain taxable brokerage account as the savings vehicle, for which gains would be taxed as long term capital gains.

529 account withdrawals must happen in the same tax year as the expenses incurred, meaning you can't withdraw in late December for expenses weeks later in early January.

Each 529 plan can only have one beneficiary at a time. You can change the beneficiary later if one child doesn’t go to college but another one does, but you can’t name multiple children as beneficiaries simultaneously.

Investments in education savings plans are not guaranteed and may lose money. Their growth or lack thereof will depend entirely on the riskiness of the assets you choose. 529 plans will usually include some low-risk, principal-protected bank products that may be insured by the FDIC.

Lastly, rules and regulations surrounding 529 plans may vary by state, so be sure to research the specific plan offered by your state or consult a financial advisor for personalized guidance. Also make sure the education institution is eligible before opening the account and especially before withdrawing and using 529 funds.

Where To Open a 529 Account

529 accounts are typically available at most major brokers like Fidelity and Schwab.

There are also “direct-sold” plans that can be found via the state's plan's website. You can find these from the College Savings Plan Network.

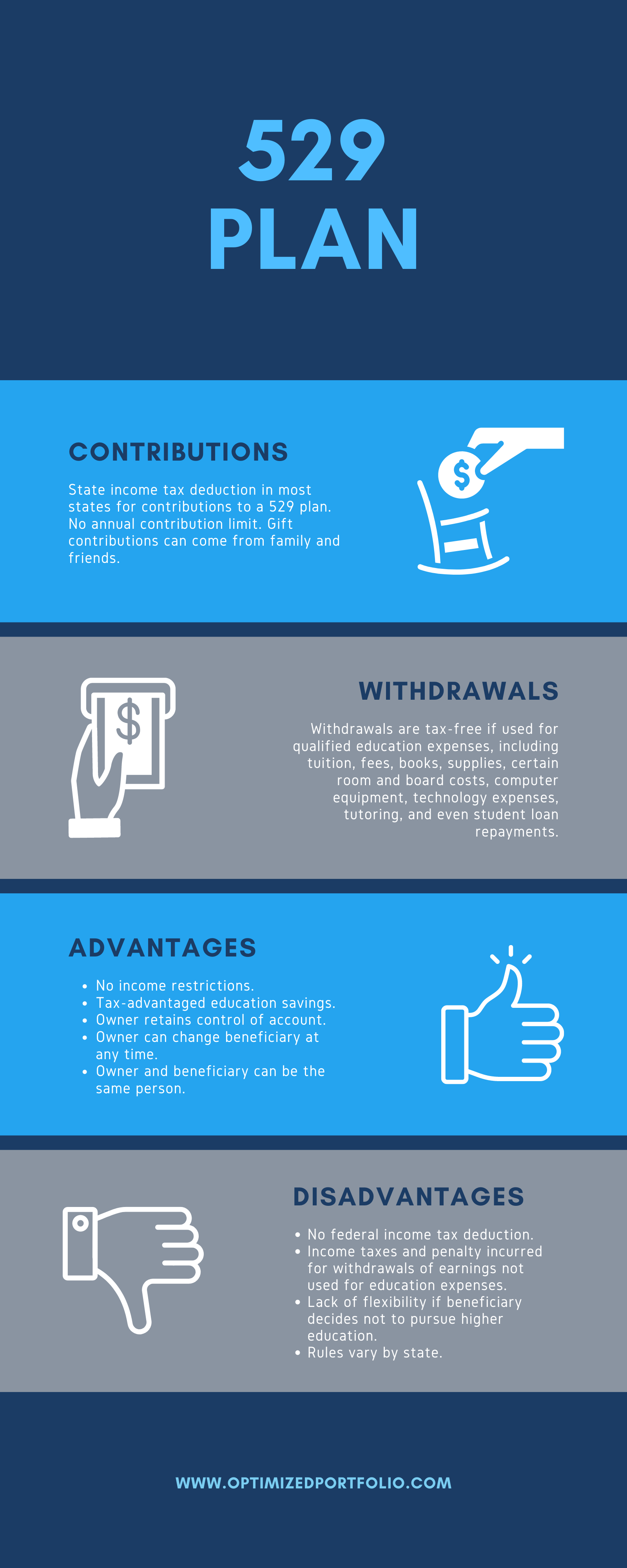

529 Plan Infographic

To recap the main advantages and disadvantages of using a 529 plan, here's an infographic:

Do you utilize a 529 plan? Are you thinking about starting one after reading this blog post? Let me know in the comments.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Leave a Reply