The Pinwheel Portfolio utilizes “colorful diversification and familiar symmetry.” Here we’ll take a look at its components, performance, and the best ETF’s to use in its execution.

Interested in more Lazy Portfolios? See the full list here.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

What is the Pinwheel Portfolio?

The Pinwheel Portfolio is a lazy portfolio created by Tyler from PortfolioCharts.com. He named it such because of its “colorful diversification and familiar symmetry.” He also designed the Golden Butterfly Portfolio. The Pinwheel Portfolio is probably the most visually appealing lazy portfolio.

The Pinwheel Portfolio was designed to span all 4 core assets: U.S. stocks, international stocks, bonds, and real assets. This maximizes diversification similarly to the David Swensen Portfolio.

Essentially, the Pinwheel Portfolio uses equal weightings of the 4 assets above, and then overweights (“tilts”) specific asset classes within each one in an attempt to optimize performance (greater expected returns) and reduce volatility and risk. These specific market segments have historically paid a risk premium.

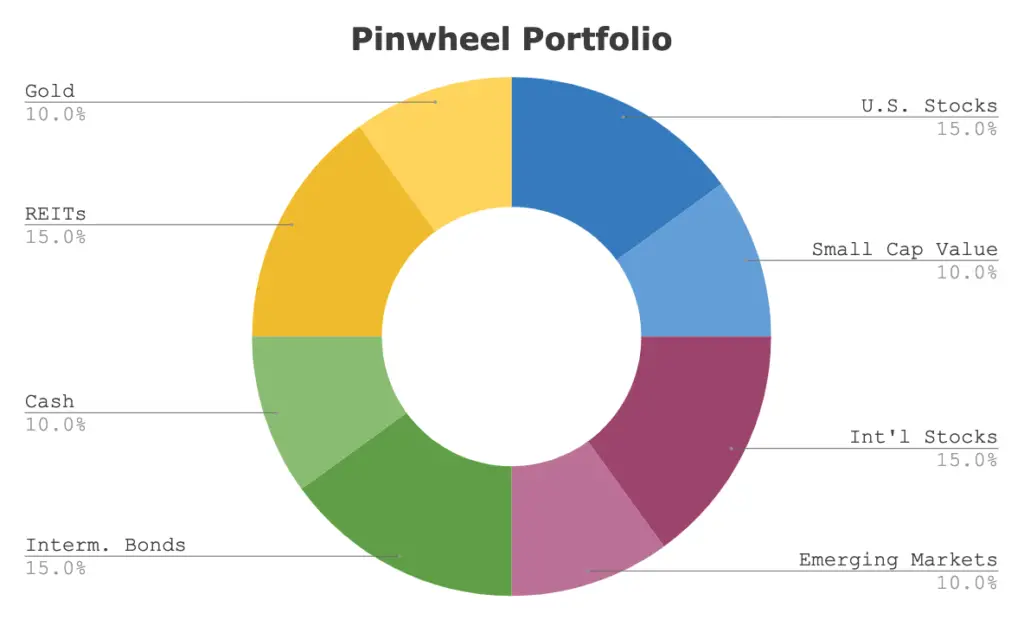

The Pinwheel Portfolio is as follows:

- 15% Total U.S. Stock Market

- 10% U.S. Small Cap Value

- 15% Total International Stock Market

- 10% Emerging Markets

- 15% Intermediate Bonds

- 10% Cash

- 15% REITs

- 10% Gold

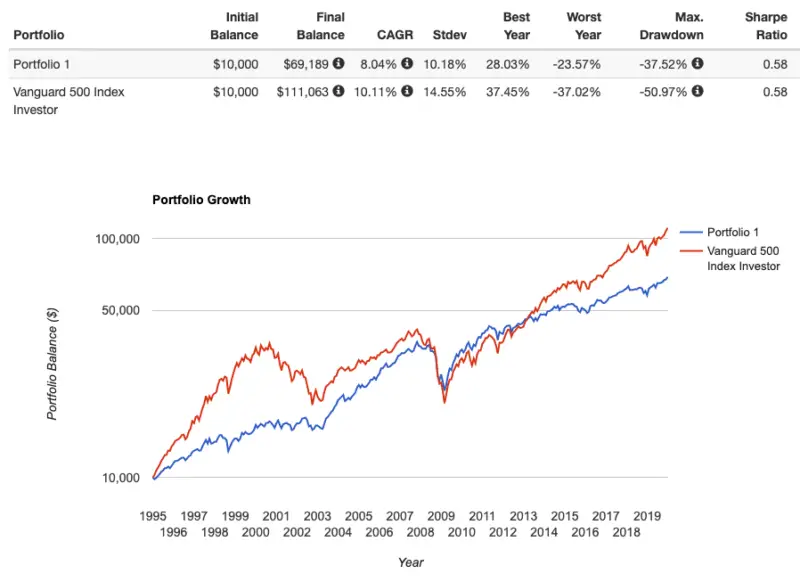

Pinwheel Portfolio Performance Backtest vs. the S&P 500

Going back to 1995, here's the Pinwheel Portfolio's performance vs. an S&P 500 index fund through 2019:

Compared to the S&P 500 index, the Pinwheel Portfolio has delivered an identical risk-adjusted return (Sharpe) since 1995, with lower volatility, as we'd expect.

I appreciate the Pinwheel's Portfolio's use of international diversification (most lazy portfolios don't) and the small cap value tilt to capture the Size and Value factor premia. I still think they exist, though they've suffered in recent years.

I also agree with Tyler that while many, myself included, aren't into gold, a 10% allocation is a much easier pill to swallow than 20-25% as with the Permanent Portfolio. The bonds, gold, and REITs act as diversifiers to help lower portfolio volatility and risk, providing a smoother, more stable ride as you can see in the graph above.

With the 10% allocation to cash, I'd probably be inclined to put the other 15% fixed income in long-term bonds instead of intermediate-term bonds, thereby basically getting a barbell approach on the 1/4 fixed income slice.

Pinwheel Portfolio ETF Pie for M1 Finance

M1 Finance is a great choice of broker to implement the Pinwheel Portfolio because it makes regular rebalancing seamless and easy, has zero transaction fees, and incorporates dynamic rebalancing for new deposits. I wrote a comprehensive review of M1 Finance here.

Using almost entirely low-cost Vanguard funds, we can construct the Pinwheel Portfolio pie like this:

- VTI – 15%

- VIOV – 10%

- VXUS – 15%

- VWO – 10%

- VGIT – 15%

- VGSH – 10%

- VNQ – 15%

- SGOL – 10%

You can add the Pinwheel Portfolio pie to your portfolio on M1 Finance by clicking this link and then clicking “Save to my account.”

Disclosure: I am long VWO in my own portfolio.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Any particular reason for VBR instead of something like VIOV? As you point-out in a different article VBR is more of a blend; it’s actually a small/mid index rather than a true small-cap index.

Sorry about that. Just hadn’t gotten around to swapping it out yet! I’ll try to get to that tonight if I remember.

Got it updated!

John,

I’m really learning a lot from reading your analysis of each lazy portfolio.

I noticed that the max drawdown for the Pinwheel Portfolio shown here (37.52%) differs substantially from the max drawdown shown on the Portfoliocharts website (26%).

This discrepancy exists for some other portfolios as well. For Golden Butterfly, you show a max drawdown of 16.64%. Portfoliocharts shows 11%. For most of the other portfolios I checked, the max drawdowns were within 1 or 2 percentage points. However, the discrepancy with the Pinwheel Portfolio really stood out to me.

My understanding is that there might be small differences due to the data set used or the calculation method or the years examined, but I wouldn’t think these factors would result in such a big delta as seen in the Pinwheel Portfolio. Is there another factor that might explain this? I’d also be interested in knowing your take on methodology and how using different methods and data sets produce different results (maybe a good blog post?).

Thanks.

Sorry for the late reply; your comments initially got flagged as spam.

Glad you’re enjoying the content!

I looked into this briefly and I’m honestly not sure why these differences in drawdown metrics are happening between the 2 sites. You’re right; they definitely should not differ that much. Unfortunately on PortfolioCharts it doesn’t show the year that drawdown occurred so I can’t even really attempt to match them up.

I suspect this is why, from Portfolio Charts:

Sounds like what PC is calling the “max drawdown” may actually be the “Worst Year” stat reported by PV. The “even worse than that in the middle of the year” is what PV is reporting on.

In any case, I’d be more likely to trust PV’s metrics.

I see, thanks.