M1 Finance provides Expert Pies that are pre-built portfolios available for you to invest in if you prefer not to choose your own investments. They are comprised of low-cost Vanguard ETF's. This is ideal for the investor who wants a lazy portfolio to be completely hands-off. M1's category of “General Investing” Expert Pies allow you to select a portfolio based on your personal risk tolerance.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

M1 maintains that these portfolios are mean-variance optimized (think Modern Portfolio Theory and Harry Markowitz). This is unnecessary in my opinion, and makes them complicated and uneven. This also gives them a comparatively heavy weighting to international equities. More specifically though, I believe these portfolios are suboptimal for these reasons:

- These pies use corporate bonds. Treasury bonds are superior.

- They invest in small-cap growth stocks, which haven't paid a risk premium historically.

- Bond duration for this portfolio is skewed too short/low in my opinion for what is supposed to be an “moderately aggressive” portfolio.

- Similarly, bond allocation, at 34%, is too high in my opinion to be considered “moderately aggressive.”

- The allocation to Emerging Markets pales in comparison to that of Developed Markets, but the former offers more of a diversification benefit by having a lower correlation to the U.S. market. Emerging Markets have also paid a significant risk premium historically.

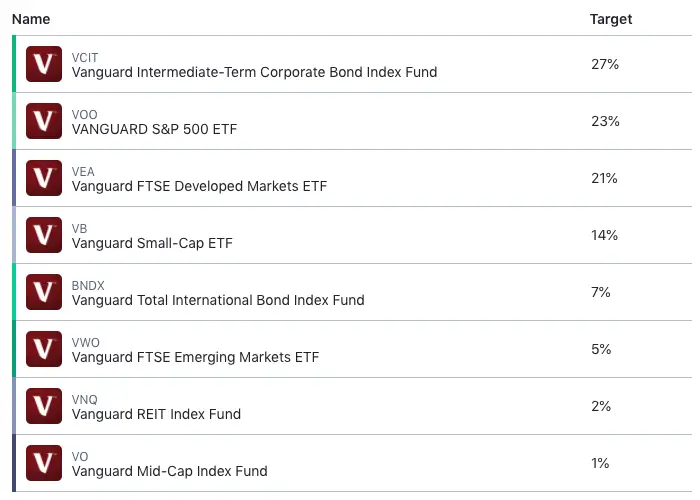

At the time of writing, M1's Moderately Aggressive Portfolio pie looks like this:

- 27% VCIT – Intermediate-Term Corporate Bonds

- 23% VOO – S&P 500

- 21% VEA – Developed Markets

- 14% VB – Small-Cap Blend

- 7% BNDX – Total International Bond Market

- 5% VWO – Emerging Markets

- 2% VNQ – U.S. REITs

- 1% VO – Mid-Cap Blend

In improving this portfolio, we're basically just going to fix the things I mentioned above:

- Avoid small- and mid-cap growth stocks and use their Value counterparts instead.

- Treasury bonds instead of corporate bonds.

- In making the portfolio truly more “aggressive,” bond holding will be set at 20% instead of 34%, and will utilize long-term treasury bonds with a longer average duration. We'll use VGLT for this.

- We're going to use a 1:1 ratio of Developed to Emerging Markets.

My resulting improved Moderately Aggressive Portfolio looks like this:

- 25% VOO

- 15% VEA

- 15% VWO

- 10% IVOV

- 10% VIOV

- 5% VNQ

- 20% VGLT

You can add this pie to your portfolio using this link.

Here are my improvements of the other variations of M1's General Investing Expert Pies.

What do you think of my attempt to improve M1's Moderately Aggressive Portfolio? Let me know in the comments.

Disclosure: I am long VOO and VWO in my own portfolio.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Apologies of this is a stupid question. I’m a recent college graduate who’s brand new to investing.

Is this a viable portfolio for a Roth IRA account?

Would all these lazy portfolios work for an M1 brokerage account as well as Roth IRA account?

Sure! Some are more tax efficient than others.

Hi John

Thank you for all the information you put out there for DYI. I always learn something new.

What is long with mid cap growth? I haven’t seen an article where you write about the disadvantage of using them. I also see you are long on VNQ. Is this in a taxable acc? I thought you dont like Reits.

Thanks in advance Pat.

Glad to hear it, Pat! In general, Growth has lower expected returns than Value, and mid cap growth tends to behave like small cap growth. I have some VNQ sitting in an old rollover IRA from a while back.