Everyone always asks how I invest my own money. Some have basically pieced it together from various mentions across the blog, but I finally got around to laying it out in detail. I've named it the Ginger Ale Portfolio.

Interested in more Lazy Portfolios? See the full list here.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

Foreword – A Brief History of My Investing Journey

I hate when recipe websites tell an unnecessary, long-winded story before getting to the recipe, so feel free to skip straight to the portfolio by clicking here.

Starting around age 18, I spun my wheels for nearly a decade stock picking and trading options on TradeKing (which Ally later acquired), usually underperforming the market. I was naive and egotistical enough to think that I could outsmart and out-analyze other traders, at least on average.

Unfortunately, a math degree with a focus in statistics strengthened my faulty conviction for a few more years before I finally converted to index investing. Thinking back on that time and the way I traded (I don't think I can even call it investing) makes me cringe now, so these days I try to do whatever I can to help others – particularly new, young investors – avoid those same pitfalls I succumbed to. I'd be much further ahead now had I just indexed from the start.

Since I had previously only traded U.S. securities and entirely ignored international assets, when I converted to index investing, I went 100% VTI for the total U.S. stock market (U.S. companies do business overseas, right?) and wrote myself an Investment Policy Statement (IPS) to avoid stock picking as a hard rule going forward. I was also still tempted to try to time the market using macroeconomic indicators and by selectively overweighting sectors around this time before realizing that sector bets are just stock picking lite, market timing tends to be more harmful than helpful, and the broad index fund does the self-cleansing and sector rearranging for me.

Then I dug deeper into the Bogleheads philosophy and realized I was still being ignorant by avoiding international stocks (more on this below), so I decided to throw in some VXUS at about 80/20 U.S. to international. I kept reading and researching and digging and concluded that I still had way too much home country bias. The U.S. is only one country out of many around the world! So I switched to 100% VT. Global stock market, market cap weighted. Can't go wrong. And “100% VT” would still be my elevator answer for a young investor just starting out.

Then I got further into the nuances of evidence-based investing as well as the important behavioral aspects of investing and what the research had to say about these things – Fama and French, Markowitz and MPT, efficient markets, leverage, Black and Scholes, Merton Miller, asset allocation, risk tolerance, sequence risk, factors, dividend irrelevance, asset correlations, risk management, etc.

I started realizing that, in short, 100% VT is objectively suboptimal in terms of both expected returns and portfolio risk. Emerging Markets only comprise 11% of the global market. Small cap stocks make up an even smaller fraction. And we should probably avoid small cap growth stocks. And certain funds have superior exposure to Value than others based on their underlying index's selection methodology. And can I stomach the drawdowns that accompany a 100% cap weighted stocks position during a crash? This line of thinking led me to books and lazy portfolios from present-day advisors like William Bernstein, Larry Swedroe, Ray Dalio, Paul Merriman, and Rick Ferri, all of whom influenced my thought process and subsequent portfolio construction.

I also realized there's an observable tradeoff between simplicity and optimization. I'm a tinkerer by nature and tend to default to the latter, probably to a fault (i.e. overfitting and data mining), which is why this blog's name is what it is, for better or for worse. People say indexing is boring, but it doesn't have to be. There's still plenty of learning to be had, and subsequent research-backed improvements to be made in the pursuit of optimization if you choose to tinker.

But don't get me wrong. Simplicity is – and probably should be – a desirable characteristic of one's portfolio for most people. Whatever allows you to sleep at night, stay the course, and not tinker during market downturns is the best strategy for you. It can take some time (and probably a market crash) to figure out what that strategy is. The portfolio below will seem “simple” to a stock picker with 100 holdings; it may seem complex to the indexer who is 100% VT.

So below I've pieced together what I think is optimal for me, based on my understanding of what the research thus far has to say about expected returns, volatility, diversification, risk, cognitive biases, and reliability of outcome, all while realizing I may get it wrong and that I may want to change it in the future.

About the Ginger Ale Portfolio

Update July 2021: Got way too many emails from people using this portfolio and then asking me about TIPS and Emerging Markets gov't bonds (what they are, what they're for, etc.). They clearly didn't understand what they were buying. That's not good. So I removed those pieces.

I'm bad at thinking of clever names for things. When writing posts, I usually sip on a can of ginger ale, so the Ginger Ale Portfolio seemed like an appropriate name.

Aside from “lottery ticket” fun money in the Hedgefundie Adventure and my taxable account in NTSX, this portfolio is basically how my “safe” money is invested. Leverage, while perhaps useful on paper for any investor, is probably not appropriate for most investors purely because of the emotional and psychological fortitude its usage requires during market turmoil.

Thus, for a one-size-fits-most portfolio, I can't in good conscience just recommend a leveraged fund. Moreover, whatever I put below will likely just be blindly copied by many novice investors who won't even bother reading or understanding the details, so I have to take that fact into consideration and be at least somewhat responsible.

This portfolio is 90/10 stocks to fixed income using a long duration bond fund to, again, accommodate sort of a one-size-fits-most asset allocation for multiple time horizons and risk tolerances. I'd call it medium risk simply because it has some allocation to fixed income. It is a lazy portfolio designed to match or beat the market return with lower volatility and risk.

It heavily tilts toward small cap value to diversify the portfolio's factor exposure. It is also diversified across geographies and asset classes. Specifically, this portfolio is roughly 1:1 large caps to small caps and for U.S. investors, it has a slight home country bias of 5:4 U.S. to international, nearly matching global market weights.

In selecting specific funds, I looked for sufficient liquidity, appreciable factor loading (where the expected premium would outweigh the fee), low tracking error, and low fees.

Here's what it looks like:

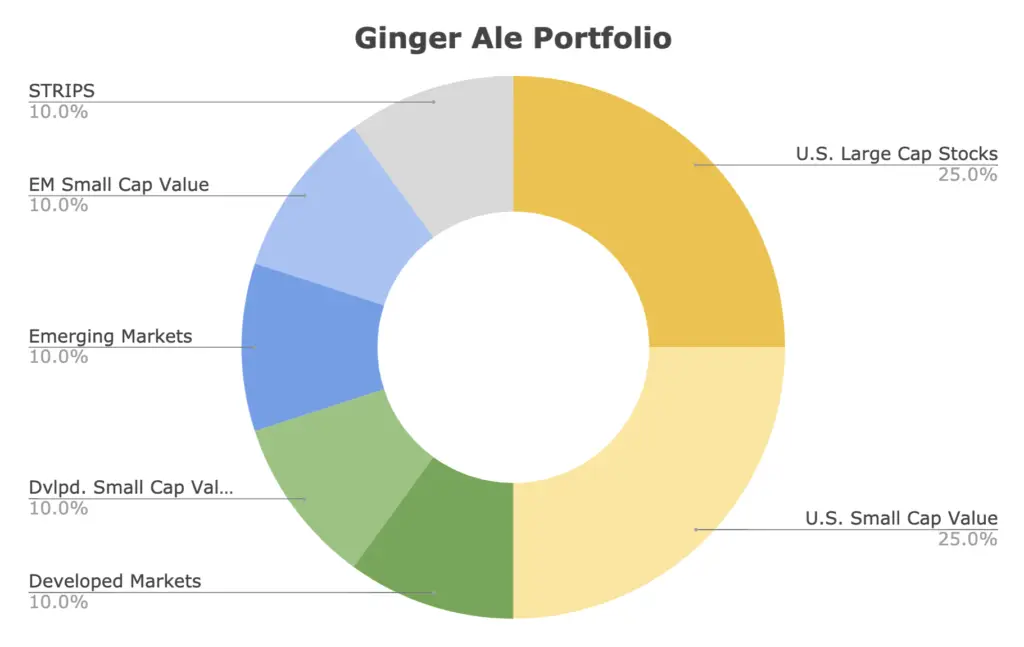

Ginger Ale Portfolio Allocations:

- 25% U.S. Large Cap Stocks

- 25% U.S. Small Cap Value

- 10% Developed Markets (ex-US)

- 10% Developed Markets (ex-US) Small Cap Value

- 10% Emerging Markets

- 10% Emerging Markets Small Cap Value

- 10% U.S. Treasury STRIPS

Below I'll explain the reasoning behind each asset in detail.

U.S. Large Cap Stocks – 25%

Most lazy portfolios use U.S. stocks – and specifically large-cap U.S. stocks – as a “base.” This one is no different, but they're still only at 25%. You'll see why later.

Not much to explain here. The U.S. stock market comprises a little over half of the global stock market and has outperformed foreign stocks historically. I don't feel comfortable going completely small caps for the equities side so we're keeping large caps here to diversify across cap sizes, as large stocks beat small stocks during certain periods, while small stocks beat large stocks over other periods.

This segment captures household names like Amazon, Apple, Google, Johnson & Johnson, Microsoft, etc. Specifically, we're using the S&P 500 Index – considered a sufficient barometer for “the market” – via Vanguard's VOO.

Why not use VTI to capture the entire U.S. stock market including some small- and mid-caps? I'll answer that in the next section.

U.S. Small Cap Value – 25%

I don't use VTI (total U.S. stock market) because I want to avoid those pesky small-cap growth stocks which don't tend to pay a risk premium. Even mid-cap growth hasn't beaten large cap blend on a risk-adjusted basis. Using VTI would also dilute my target large cap exposure.

Specifically, small cap growth stocks are the worst-performing segment of the market and are considered a “black hole” in investing. The Size factor premium – small stocks beat large stocks – seems to only apply in small cap value. As Cliff Asness from AQR says, “Size matters, if you control your junk.” Basically, if you want to bet on small caps, the evidence suggests you want to do so in small cap value, preferably while also screening for profitability.

By “risk premium,” I'm referring to the independent sources of risk identified by Fama and French (and others) that we colloquially call “factors.” Examples include Beta, Size, Value, Profitability, Investment, and Momentum. I delved into those details in a separate post that I won't repeat here, but I'll be referring to these factors and their benefits quite a few times below. Though it may sound like magic, the evidence suggests that overweighting these independent risk factors both increases expected returns over the long term and decreases portfolio risk by diversifying the specific sources of that risk, as the factors are lowly correlated to each other and thus show up at different times. The reason I don't want to go 100% factors like Larry Swedroe is because A) I don't have the stomach and conviction he has, and B) there's always the possibility of being wrong.

I know the exclusion of mid-caps entirely seems bizarre at first glance too. Factor premia tend to get larger and more statistically significant as you go smaller. That is, ideally you want to factor tilt within the small cap universe. That's exactly what we're doing here by basically taking a barbell approach in U.S. equities: using large caps and small caps to put the risk targeting exactly where we want it while still diversifying across cap sizes and equity styles. Essentially, we're letting large caps be our Growth exposure in the U.S. and consciously avoiding small- and mid-cap growth stocks.

In short, small cap value stocks have smoked every other segment of the market historically thanks to the Size and Value factor premiums. “Value” refers to underpriced stocks relative to their book value. Basically, cheaper, sometimes crappier, downtrodden stocks have greater expected returns. Small cap value stocks are smaller and more value-y than mid-cap value stocks. Thus, no mid-caps. (As an aside, Alpha Architect basically takes this idea to the extreme – finding the absolute smallest, cheapest stocks and concentrating in only 50 of them; talk about a wild ride.)

I don't want it to seem like I think this is some profound, contrarian approach. Using VTI (total stock market) instead of VOO (S&P 500) would be perfectly fine, and at only 25% of the portfolio, the difference is admittedly probably negligible. The simple point is that I've already decided on a specific small cap allocation, and I'm choosing to get that exposure through a dedicated small cap value fund rather than through VTI. Similarly, I've also already decided on a specific “pure,” undiluted large cap allocation, and I'm choosing to get that exposure through the S&P 500 Index.

Previously, the S&P Small Cap 600 Value index (VIOV, SLYV, IJS) was basically the gold standard for the U.S. small cap value segment. AVUV, the new kid on the block from Avantis, has provided some extremely impressive exposure – superior to that of those funds – in its relatively short lifespan thus far, so much so that it recently replaced VIOV in my own portfolio. I went into detail about this in a separate “small value showdown” post here. In a nutshell, it has been able to capture smaller, cheaper stocks than its competitors, with convenient exposure to the Profitability factor, all while considering Momentum in its trades, and we would expect the premium to more than make up for its slightly higher fee.

Including small caps also took the famous 4% Rule up to 4.5% historically.

Developed Markets – 10%

Developed Markets refer to developed countries outside the U.S. – Australia, Canada, Germany, the UK, France, Japan, etc.

At its global weight, the U.S. only comprises about half of the global stock market. Most U.S. investors severely overweight U.S. stocks (called home country bias) and have an irrational fear of international stocks.

If you're reading this, chances are you're in the U.S. As I just pointed out, odds are favorable that you also overweight – or only have exposure to – U.S. stocks in your portfolio. The U.S. is one single country out of many in the world. By solely investing in one country's stocks, the portfolio becomes dangerously exposed to the potential detrimental impact of that country's political and economic risks. If you are employed in the U.S., it's likely that your human capital is highly correlated with the latter. Holding stocks globally diversifies these risks and thus mitigates their potential impact.

Moreover, no single country consistently outperforms all the others in the world. If one did, that outperformance would also lead to relative overvaluation and a subsequent reversal. During the period 1970 to 2008, an equity portfolio of 80% U.S. stocks and 20% international stocks had higher general and risk-adjusted returns than a 100% U.S. stock portfolio. Specifically, international stocks outperformed the U.S. in the years 1986-1988, 1993, 1999, 2002-2007, 2012, and 2017. For the famous “lost decade” of 2000-2009 when U.S. stocks were down 10% for the period, international Developed Markets were up 13%.

For U.S. investors, holding international stocks is also a way to diversify currency risk and to hedge against a weakening U.S. dollar, which has been gradually declining for decades. International stocks tend to outperform U.S. stocks during periods when the value of the U.S. dollar declines sharply, and U.S. stocks tend to outperform international stocks during periods when the value of the U.S. dollar rises. Just like with the stock market, it is impossible to predict which way a particular currency will move next.

Moreover, U.S. stocks' outperformance on average over the past half-century or so has simply been due to increasing price multiples, not an improvement in business fundamentals. That is, U.S. companies did not generate more profit than international companies; their stocks just got more expensive. And remember what we know about expensiveness: cheap stocks have greater expected returns and expensive stocks have lower expected returns.

Dalio and Bridgewater maintain that global diversification in equities is going to become increasingly important given the geopolitical climate, trade and capital dynamics, and differences in monetary policy. They suggest that it is now even less prudent to assume a preconceived bet that any single country will be the clear winner in terms of stock market returns.

In short, geographic diversification in equities has huge potential upside and little downside for investors.

I went into the merits of international diversification in even more detail in a separate post here if you're interested.

Vanguard offers a low-cost fund called the Vanguard FTSE Developed Markets ETF. Its ticker is VEA.

Developed Markets (ex-US) Small Cap Value – 10%

We can also specifically target small cap value in ex-US Developed Markets stocks. It costs a bit more to do so, and some who tilt small cap value in the U.S. don't feel the need to do so in foreign stocks, but I think it's a prudent move considering the factor premia – in this case Size and Value – have shown up at different time periods across different geographies throughout history.

Remember we also get a diversification benefit here in doing so; it's not just for the greater expected returns. The earnings of large international corporations are more closely tied to global market forces, whereas smaller companies are more affected by local, idiosyncratic economic conditions. This means they are perfectly correlated with neither their large-cap counterparts nor with U.S. stocks.

Until just about a year ago, an expensive dividend fund from WisdomTree (DLS) was arguably the best way to access this segment of the global market. Now, Avantis has launched a fund available to retail investors that specifically targets international small cap value – AVDV. It is the only fund available to the public that specifically targets Size and Value (and conveniently, Profitability) in ex-US stocks. AVDV is also roughly half the cost of the former option DLS.

Emerging Markets – 10%

Emerging Markets refer to developing countries – China, Taiwan, India, Brazil, Thailand, etc.

Investors sometimes shy away from these countries due to their unfamiliarity and greater risk. I would argue that makes them more attractive. Stocks in these countries have paid a significant risk premium historically, compensating investors for taking on their greater risk.

Arguably more importantly, Emerging Markets tend to have a reliably lower correlation to U.S. stocks compared to Developed Markets, and thus are a superior diversifier. Of course, we would expect this, as these developing countries have unique risks – regulatory, liquidity, political, financial transparency, currency, etc. – that do not affect developed countries, or at least not the same extent. I delved into this in a little more detail here. For the previously mentioned “lost decade” of 2000-2009 when the S&P 500 delivered a negative 10% return, Emerging Markets stocks were up 155%.

Emerging Markets only comprise about 11% of the global stock market. This is why I don't use the popular VXUS (total international stock market) – because its ratio of Developed Markets to Emerging Markets is about 3:1. Here we're using a 1:1 ratio of Developed to Emerging Markets.

Vanguard's Emerging Markets ETF is VWO.

Emerging Markets Small Cap Value – 10%

Just like we just did with Developed Markets above, we can focus in on small cap value stocks within Emerging Markets as well.

Here we’re using a small cap dividend fund from WisdomTree as a proxy for Value within small caps in Emerging Markets. Don’t let this sound discouraging. The fund also screens for liquidity and strong financials and has appreciable loadings across Size, Value, and Profitability. Factor investors are wise to this fact, as this fund boasts nearly $3 billion in assets.

The fund is DGS, the WisdomTree Emerging Markets SmallCap Dividend Fund.

Factor investors like myself thought AVES, Avantis’s newest offering for more aggressive factor tilts in Emerging Markets, might dethrone DGS when it launched in late 2021. While it’s certainly no slouch and would still be a fine choice, I still prefer the looks of DGS, even with its higher fee. I compared these specifically here.

U.S. Treasury STRIPS – 10%

No well-diversified portfolio is complete without bonds, even at low, zero, or negative interest rates.

By diversifying across uncorrelated assets, we mean holding different assets that will perform well at different times. For example, when stocks zig, bonds tend to zag. Those 2 assets are uncorrelated. Holding both provides a smoother ride, reducing portfolio volatility (variability of return) and risk. We used the same concept above in relation to risk factor exposure. Now we're talking about entirely separate asset classes, but we're also taking advantage of a risk premium in fixed income: term. I delved into the concept of asset diversification in detail in a separate post here.

STRIPS (Separate Trading of Registered Interest and Principal of Securities) are basically just bonds where the coupon payment is rolled into the price, so they are zero-coupon bonds. Here we're using a fund that is essentially just very long duration treasury bonds (25 years).

I can see the waves of comments coming in, which I see all the time on forums and Reddit threads:

- “Bonds are useless at low yields!”

- “Bonds are for old people!”

- “Long bonds are too volatile and too susceptible to interest rate risk!”

- “Corporate bonds pay more!”

- “Interest rates can only go up from here! Bonds will be toast!”

- “Bonds return less than stocks!”

So why long term treasuries? Here are my brief rebuttals to the above.

- Bond duration should be roughly matched to one's investing horizon, over which time a bond should return its par value plus interest. Betting on “safer,” shorter-term bonds with a duration shorter than your investing horizon could be described as market timing, which we know can't be done profitably on a consistent basis. This is also a potentially costlier bet, as yields tend to increase as we extend bond duration, and long bonds better counteract stock crashes. More on that in a second.

- Moreover, in regards to bond duration, we know market timing doesn't work with stocks, so why would we think it works with bonds and interest rates? Bonds have returns and interest payments. A bond's duration is the point at which price risk and reinvestment risk – the components of what we refer to as a bond's interest rate risk – are balanced. In this sense, though it may seem counterintuitive, matching bond duration to the investing horizon reduces interest rate risk and inflation risk for the investor. An increase in interest rates and subsequent drop in a bond's price is price risk. A decrease in interest rates means future coupons are reinvested at the lower rate; this is reinvestment risk. A bond's duration is an estimate of the precise point at which these two risks balance each other out to zero. If you have a long investing horizon and a short bond duration, you have more reinvestment risk and less price risk. If you have a short investing horizon and a long bond duration, you have less reinvestment risk and more price risk. Purposefully using one of these mismatches in expectation of specific interest rate behavior is intrinsically betting that your prediction of the future is better than the market's, which should strike you as unlikely.

- It is fundamentally incorrect to say that bonds must necessarily lose money in a rising rate environment. Bonds only suffer from rising interest rates when those rates are rising faster than expected. Bonds handle low and slow rate increases just fine; look at the period of rising interest rates between 1940 and about 1975, where bonds kept rolling at their par and paid that sweet, steady coupon.

- Bond pricing does not happen in a vacuum. Here are some more examples of periods of rising interest rates where long bonds delivered a positive return:

- From 1992-2000, interest rates rose by about 3% and long treasury bonds returned about 9% annualized for the period.

- From 2003-2007, interest rates rose by about 4% and long treasury bonds returned about 5% annualized for the period.

- From 2015-2019, interest rates rose by about 2% and long treasury bonds returned about 5% annualized for the period.

- New bonds bought by a bond index fund in a rising rate environment will be bought at the higher rate, while old ones at the previous lower rate are sold off. You're not stuck with the same yield for your entire investing horizon. The reinvested higher yield makes up for any initial drop in price over the duration of the bond.

- We know that treasury bonds are an objectively superior diversifier alongside stocks compared to corporate bonds. This is also why I don't use the popular total bond market fund BND.

- At such a low allocation of 10%, we need and want the greater volatility of long-term bonds so that they can more effectively counteract the downward movement of stocks, which are riskier and more volatile than bonds. We're using them to reduce the portfolio's volatility and risk. More volatile assets make better diversifiers. The vast majority of the portfolio's risk is still being contributed by stocks. Using long bonds also provides some exposure to the term fixed income risk factor.

- We're not talking about bonds held in isolation, which would probably be a bad investment right now. We're talking about them in the context of a diversified portfolio alongside stocks, for which they are still the usual flight-to-safety asset during stock downturns. It has been noted that this uncorrelation of treasury bonds and stocks is even amplified during times of market turmoil, which researchers referred to as crisis alpha.

- Similarly, short-term decreases in bond prices do not mean the bonds are not still doing their job of buffering stock downturns.

- Bonds still offer the lowest correlation to stocks of any asset, meaning they're still the best diversifier to hold alongside stocks. Even if rising rates mean bonds are a comparatively worse diversifier (for stocks) in terms of expected returns during that period does not mean they are not still the best diversifier to use.

- Historically, when treasury bonds moved in the same direction as stocks, it was usually up.

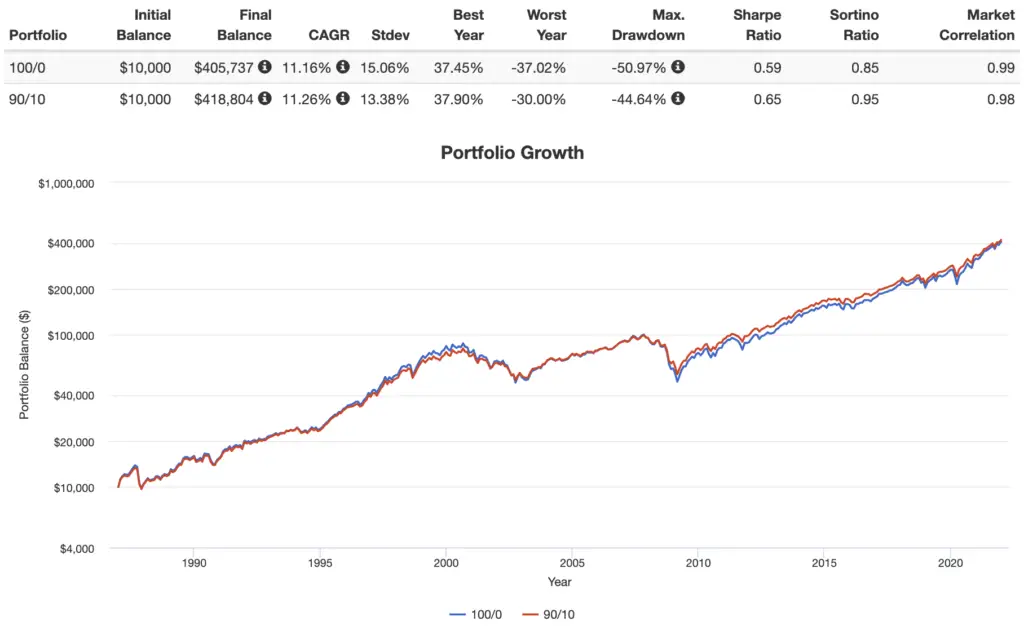

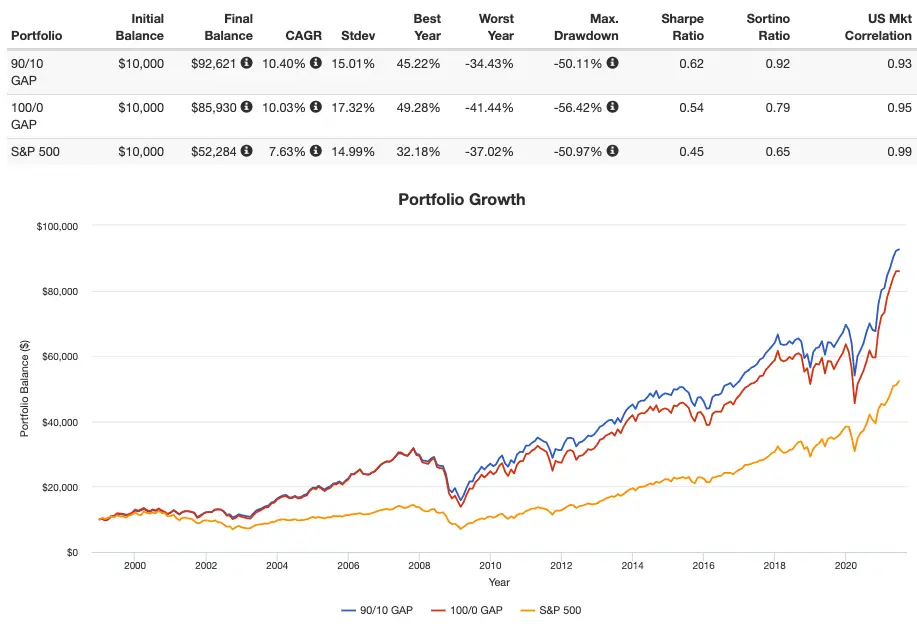

- Long bonds have beaten stocks over the last 20 years. We also know there have been plenty of periods where the market risk factor premium was negative, i.e. 1-month T Bills beat the stock market – the 15 years from 1929 to 1943, the 17 years from 1966-82, and the 13 years from 2000-12. Largely irrelevant, but just some fun stats for people who for some reason think stocks always outperform bonds. Also note how I've shown below that a 90/10 portfolio using STRIPS outperformed a 100% stocks portfolio on both a general and risk-adjusted basis for the period 1987-2021.

- Interest rates are likely to stay low for a while. Also, there’s no reason to expect interest rates to rise just because they are low. People have been claiming “rates can only go up” for the past 20 years or so and they haven't. They have gradually declined for the last 700 years without reversion to the mean. Negative rates aren't out of the question, and we're seeing them used in some foreign countries.

- Bond convexity means their asymmetric risk/return profile favors the upside.

- I acknowledge that post-Volcker monetary policy, resulting in falling interest rates, has driven the particularly stellar returns of the raging bond bull market since 1982, but I also think the Fed and U.S. monetary policy are fundamentally different since the Volcker era, likely allowing us to altogether avoid runaway inflation like the late 1970’s going forward. Stocks are also probably the best inflation “hedge” over the long term.

Here's that backtest mentioned above showing a 90/10 portfolio using STRIPS beating a 100% stocks portfolio for 1987-2021:

David Swensen summed it up nicely in his book Unconventional Success:

“The purity of noncallable, long-term, default-free treasury bonds provides the most powerful diversification to investor portfolios.”

Ok, bonds rant over.

For this piece, I'm using Vanguard's EDV, the Vanguard Extended Duration Treasury ETF.

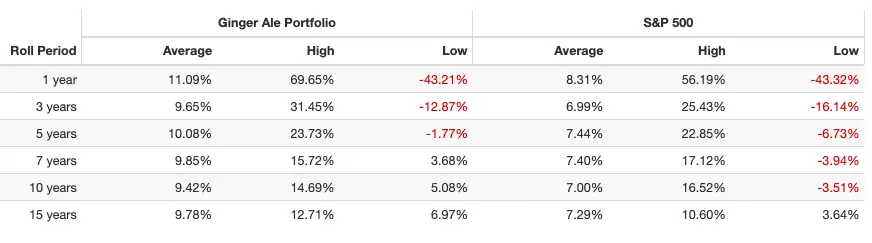

Ginger Ale Portfolio – Historical Performance

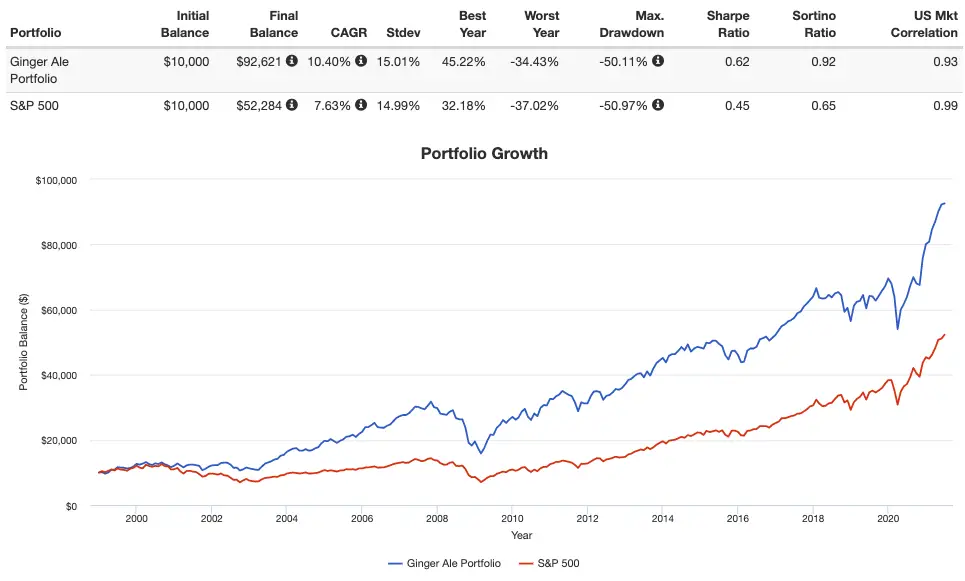

Some of these funds are pretty new, so I had to use comparable mutual funds from Dimensional in some cases to extend this backtest and give us a rough idea of how this thing would have performed historically. The furthest I could get was 1998, going through June 2021:

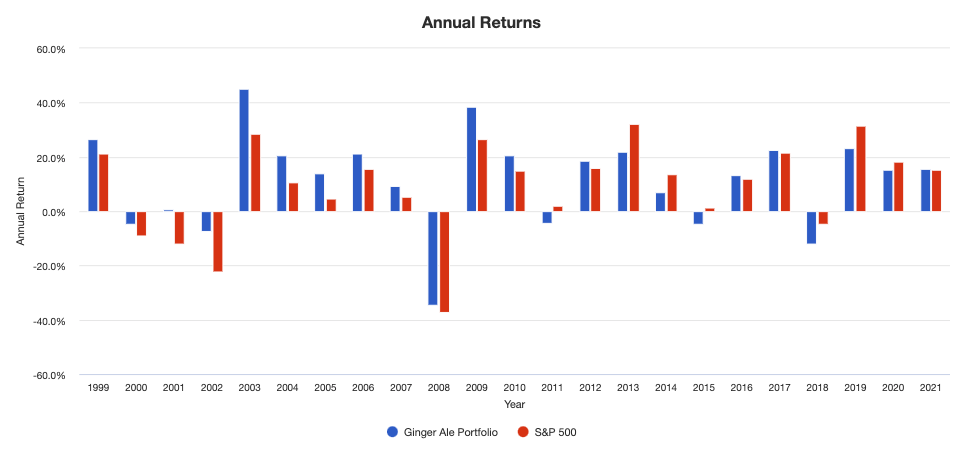

Here are the annual returns:

Here are the rolling returns:

Keep in mind the Size and Value premia and international stocks suffered for the decade 2010-2020, otherwise I think the differences in performance metrics would have been even greater.

Ginger Ale Portfolio Pie for M1 Finance

So putting the funds together, the resulting Ginger Ale Portfolio looks like this:

- VOO – 25%

- AVUV – 25%

- VEA – 10%

- AVDV – 10%

- VWO – 10%

- DGS – 10%

- EDV – 10%

You can add this pie to your portfolio on M1 Finance by clicking this link and then clicking “Save to my account.”

Canadians can find the above ETFs on Questrade or Interactive Brokers. Investors outside North America can use Interactive Brokers.

Being More Aggressive with 100% Stocks

I'd like to think I made a pretty good case for why you shouldn't fear bonds, but if you're young and/or you have a very high risk tolerance, you might still be itching to ditch the bonds and go 100% stocks. Here's a more aggressive version, basically giving an extra 5% each to VOO and AVUV for more of a U.S. tilt:

- VOO – 30%

- AVUV – 30%

- VEA – 10%

- AVDV – 10%

- VWO – 10%

- DGS – 10%

Here's the pie link for that one.

Just note that historically this would have resulted in worse performance than the original 90/10:

Incorporating NTSX, NTSI, NTSE

A lot of people know I'm a huge fan of WisdomTrees line of “Efficient Core” funds like NTSX and have explicitly asked about replacing the stocks index funds from the aggressive version with these new 90/60 funds from WisdomTree, so I've added this section to briefly address that. If this idea sounds foreign to you, maybe go read this post that explains how NTSX works first and then come back here.

Making those substitutions of the WisdomTree Efficient Core Funds (NTSX, NTSI, and NTSE) for the broad index funds for the S&P 500 (VOO), ex-US Developed Markets (VEA), and Emerging Markets (VWO) is absolutely fine, but I've tried to explain to a few people in the comments that this doesn't materially change the exposure too much from the original Ginger Ale Portfolio simply because EDV packs quite a volatile punch since it's extended duration treasury bonds. That was the whole point of its inclusion.

In other words, going 6x on intermediate treasury bonds (what the WisdomTree funds do) is nearly the same exposure as what EDV provides.

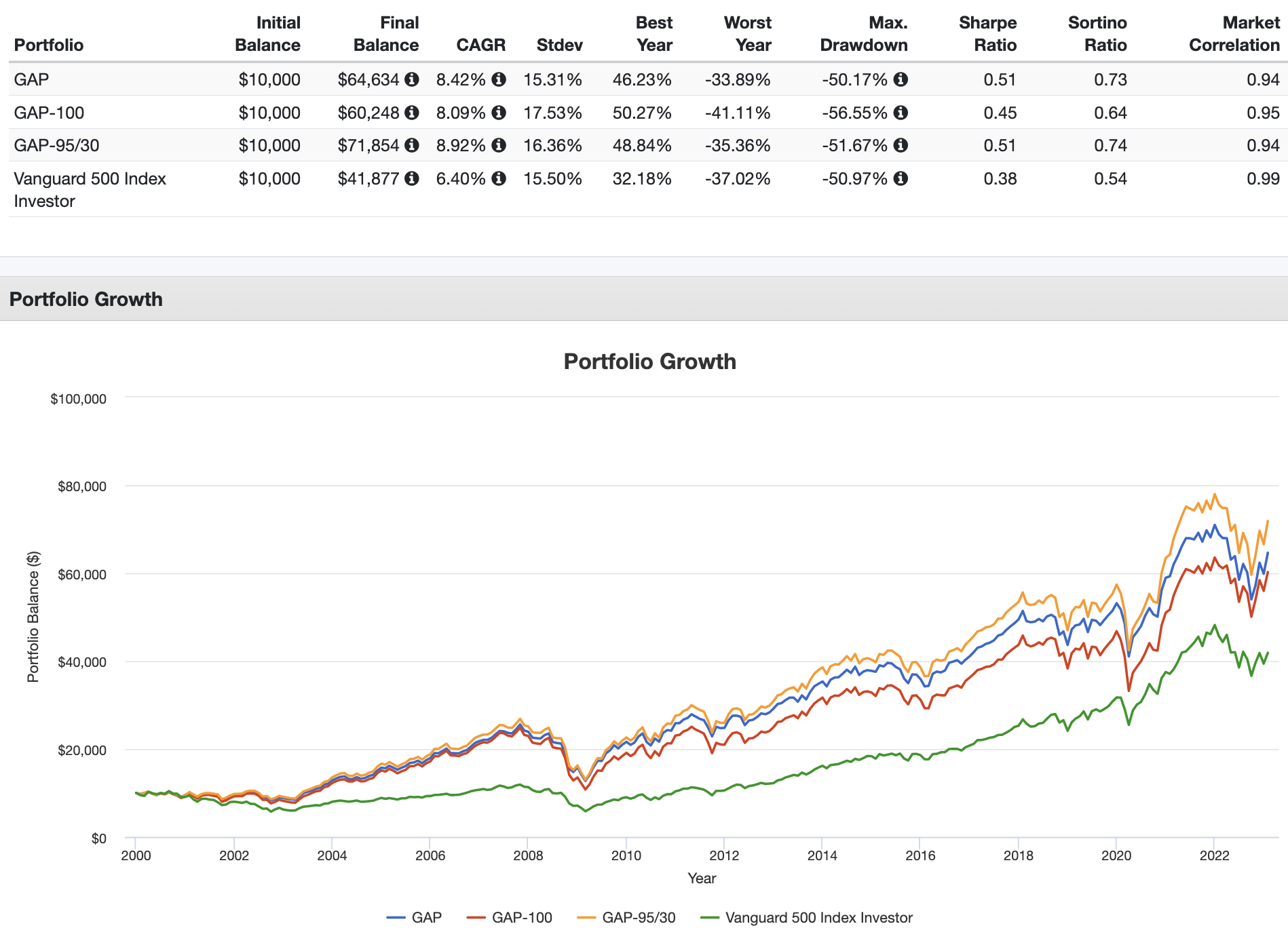

This is illustrated in the backtest below that shows the original Ginger Ale Portfolio, the aggressive 100% stocks version, and a version substituting in NTSX/NTSI/NTSE that delivers effective exposure of 95/35:

Making those substitutions, that 95/30 portfolio looks like this:

NTSX – 30%

AVUV – 30%

NTSI – 10%

AVDV – 10%

NTSE – 10%

DGS – 10%

Also keep in mind this one has a much greater expense ratio. You can get this pie here.

Adjusting This Portfolio For Retirement

I've also had a lot of people ask me how I plan to adjust this portfolio as I near and enter retirement. The answer is pretty simple and straightforward. I don't care about dividends or using them as income, so I plan to simply decrease stocks, increase bonds, decrease bond duration, add some TIPS, and sell shares as needed. Factor tilts and geographical diversification would remain intact.

For example, a 40/60 version using intermediate nominal and real bonds might look something like this:

- 10% VOO – U.S. Large Caps

- 10% AVUV – U.S. Small Cap Value

- 5% VEA – Developed Markets (ex-US)

- 5% AVDV – Developed Markets (ex-US) Small Cap Value

- 5% VWO – Emerging Markets

- 5% DGS – Emerging Markets Small Cap Value

- 30% VGIT – Intermediate U.S. Treasury Bonds

- 30% SCHP – Intermediate TIPS

That pie is here if you want it for some reason.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Questions, comments, concerns, criticisms? Let me know in the comments.

Disclosure: I am long VOO, AVUV, VEA, VWO, AVDV, DGS, and EDV.

Interested in more Lazy Portfolios? See the full list here.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Hey, I just discovered this website so I’m not the most advanced in the subject and am probably missing something obvious but I was comparing your ginger ale portfolio to Ben Felixes portfolio and noticed that the s&p 500 index results were different in the two models presented even though they were over the same time horizon.

One probably includes a few months that throws it off, i.e. not lined up perfectly with calendar year Jan. 1.

I put together a version of this utilizing Avantis funds and I was wondering if I could get your opinion. The holdings are as follows:

AVLV: 25% (0.15%)

AVUV: 25% (0.25%)

AVDE: 10% (0.23%)

AVDV: 10% (0.36%)

AVEM: 10% (0.36%)

AVES: 10% (0.36)

EDV: 10% (0.06%)

From what I can gather this would give it a much heavier factor tilt than the vanilla ginger ale portfolio which may or may not pay off, but it will have a significantly higher expense ratio which will eat into returns. Taking a look at the funds themselves, they appear to less diversified in terms of total holdings and they exclude real estate entirely (which is why it’s held in AVGE). With this in mind would it be prudent to add some AVRE?

Also, would there be any major tax drag with this or the vanilla ginger ale portfolio in taxable? It doesn’t seem that there would be anything outrageous but perhaps I’m missing something…

Thanks, this is a great read. I’m currently planning to adopt a size/value tilt in my own portfolio.

If someone was wanting to turn down the exposure to the US a little…. Do you have an opinion on international treasuries being included within the bond portion of portfolio? Eg IGOV + EDV

Thanks, Sean! Based on the evidence, international bonds don’t appear to hurt or help the portfolio, so I opt for simplicity on that one.

Thank you for your articles! Really great job! Could you answer please, why did you choose equal proportion of large and small stocks in every type of markets. Why not 60:40 or 70:30 and etc. ?

For the US domestic exposure you’ve opted to Go S&P 500 Large Cap and S&P 600 Value specifically for the factor tilt from what I understand – to make a clear delineation and gain the size/value premia.

What about the Developed Markets though? VEA looks to be mostly Large Cap but holds medium and small cap also. (FTSE all Cap ex-US) Why not go with a Large Cap Developed markets fund of some kind that is more targeted — like VOO vs VTI?

Thanks for the great blog site. Very very helpful information. I’m redesigning my portfolio .. something like this:

18% S&P 500 USA large cap

18% Small Cap Value ( S&P 600 SC Value Index VIOV )

13% International Large Cap Blend (Developed Markets) VTMGX

13% International Small Cap Value Avantis – AVDV

8% Emerging Markets (VEMAX)

BONDS 30%:

20% Intermediate Term Treasuries ( VISGX )

10% TIPS ( VIPSX )

An int’l equivalent of something more targeted like VOO doesn’t really exist to my knowledge, at least not at the same low fee of something like VEA. And again, VTI would be perfectly fine for the broad U.S. piece.

Hi,

Do you split your holdings across multiple investment accounts to have a unified portfolio? If so, which holdings do you put in taxable, IRA and 401K?

Or, do you have different strategies in different accounts? This question is more about the dividend pie that I also found on the website.

Regards!

Yep, one single unified strategy split up based on tax efficiency whenever possible but I don’t obsess over it.

Howdy,! Hope your Turkey day was enjoyable! I surf your sight and enjoy the content and opinions. You have me interested in Advantis funds. Any options yet on AVGE.? It holds much of the fund styles and investments that you and others suggest Jen on fund. Sort of a VT on steroids…. If you will…..

Thanks! I did just recently cover AVGE here actually.

Hi. Is there a variation of this but using Vanguard only? I’m not able no find all of these ETF at etoro. Regards.

Along with VOO, VEA, and VWO, you should find VIOV (replacement for AVUV) and VSS (replacement for AVDV and DGS). Good luck!

Hi John – would you consider replacing AVDV with DDLS, as they both seem to target similar segments with DDLS having a better longer term return? Thanks!

Do you hold this portfolio in a non-taxable account? How often do you rebalance it?

Thank you for this wonderful site, which I’ve discovered just today. A novice question:

Does Ginger Ale assume yearly re-balancing, which would make it less suitable than NTSX for a taxable account?

(i.e. what might we expect from a simulation of rolling 15-year average returns for NTSX vs. the same for Ginger-Ale with annual rebalancing in an account taxable at 15% long term capital gains?)

Thanks, Scott! Correct, annual rebalancing.

Thanks for replying; didn’t notice your reply and I foolishly reposted this question. Ignore the reposting–and thanks again!

Does EDV still make sense at the end of 2022, with interest rates only expected to go higher?

They way I understand EDV is this: increase in interestate rates = drop in EDV value. So inverse correlation.

Depends on allocation and time horizon. The relationship you describe is the same for all bonds, not just EDV.

The new ETF by Avantis, AVGE, seems to be a lazy portfolio somewhat similar to your Ginger Ale portfolio. I noticed it is actively managed and has a REIT ETF included so I think it best for a tax-deferred account. Overall, very nice package for only 23 basis points in my opinion and takes all the annual rebalancing out of it if I understand it correctly. A review on this ETF would be much appreciated in the future.

Indeed, David. Will definitely cover AVGE sometime soon.

David, circling back. I just published a post on AVGE here.

John,

Thank you for the great work. Any reason not to ditch EDV, ratchet up the equities a bit and replace VOO with NTSX and VEA with NTSI?

Not a bad idea. Should result in roughly the same exposure.

Hello,

im using trade republic in europe and its hard to find etf equivalents.

For the Vanguard Extended Duration Treasury ETF would the iShares USD Treasury Bond 20+yr UCITS ETF USD (Ticker DTLA) be a valid alternative?

Thank you

Thank you for all of your time and effort on these posts.

What do you think of replacing VOO, VEA and VWO with NTSX, NTSI and NTSE ?

Thanks, Dennis! Sounds like a fine idea if you want a bit more leverage.

Why not use AVES?

Wanted to get a good sample size (history) of data first before evaluating it. I’ll probably make that switch after writing it up. Stay tuned.

Why not use AVES instead of VWO?

Not the same thing.

A couple of questions, you’ve mentioned elsewhere that you hold leveraged ETFs, but I don’t see them here in this portfolio. How do they fit in here? In the same vein, how do you model your other holdings, like real estate, cash into this? To be specific, I think of “my portfolio” as being the sum total of my investments, across all accounts, which is why I ask this questions.

The second question has to do with your take on small cap growth. I just compared VBR and VBK, and it really looks like their perfomance is somewhat similar. What am I missing?

Answered this in other comments already. Not sure what you mean with your VBR/VBK question. I laid out the case for small cap value stocks in detail.

So if I’m trying to switch to your method of investing, would I just sell everything I currently have in one fell swoop and then buy using your asset allocation? Or should I do it gradually? I have thought about making the switch to some version of your ginger ale portfolio many times but I really get stuck on how to unwind what I currently have, which right now is a bunch of cash, some individual stocks, some mutual funds, and some ETFs. I’m approaching retirement, but have very few bonds–because I just don’t understand them. I have a taxable account, but much more in various IRAs and 401ks. Sad to say some if it is in ARKK funds which were actually doing great and I neglected to get out when I should have. (Fortunately not that much though.)

Sarah, this would probably depend on any tax implications to consider, as well as what your overall strategy and target asset allocation are. Best to consult a financial professional for your personal situation.

Hi, great article. I’m based in the uk. Any guidance on how to construct the portfolio given my location?

Thanks

Sorry, Paul, I’m not well versed on what specific products are available to you there.

Hi. Can I use VT instead VOO+VEA+VWO? And complement with AVDV + AVUV + DGS?

Regards

Sure, it would just be a different allocation to US, Developed Markets, and Emerging Markets.

What you mean? The Weights? For what I calculate would be just a few points…but not sure if I have it right. In case you have a quick guess, would love to hear….

Yes, different weights. The whole point of me breaking up VEA and VWO, for example, is to purposely weight them differently than their global market cap, e.g. the ratio of ex-US Developed to Emerging in VT is roughly 3:1 and I want 1:1, as I explained in the post. Using VT to replace VOO, VEA, and VWO would put it at about 50%, but then VT also includes US small caps.

John,

I am back re-reading the GA portfolio notes on the bond allocation and the approaching retirement section. Obviously, my entry into the GA portfolio early this year could not have been timed worse. I’ve already dialed back my EDV by 2 % which goes against everything you teach about market timing. But it has been unbearable to see my “hedge” perform worse than a tanking stock market.

Anyways, you speak of EDV having a duration of 25 years and matching duration of treasury to time to retirement. Your retirement adjustment goes all the way to 60% bond with no EDV. Is there a way I should think about tinkering on the way there? What does the middle look like? I’m about 20 years from retirement currently. Easy for me to adjust my portfolio with M1. Or do I say F*** it and just buy target date? Thanks again for your work on this topic.

Barry, the most agnostic approach would be to aim to match the duration to the investing horizon, adjusting each year. A target date fund basically does the same thing; nothing special about them but obviously more hands off. The TDF is also probably not duration matching.

Can you comment on the difference between EDV and TLT or another non STRIPS lol germ bind as far as performance and diversification?

I’m thinking of using the fidelity or vanguard long term treasuries fund due to the very low expense ratio for my bond allocation

Essentially EDV is just longer duration.

What’s the benefit of that in a diversified portfolio?

More volatility and/or suitable for a longer time horizon.

Any particular reason (other than % aesthetics) you do 55/45 US/intl in your Ginger Ale portolio but go to 50/50 us/intl for retirement version? (and 60/40 for your aggressive version)

Are you still holding to a 55/44 US/INTL overall presently?

Just worked out that way trying to get round numbers. Won’t make much of a difference.